Car insurance is important coverage because not only can it protect your car, it can also help pay for another person’s injuries or property damage if you cause an accident.

Although your auto policy likely needs to be reviewed less frequently than your homeowners insurance policy because fewer changes occur with your car, it is still important to review it every few years, as your financial situation changes, or when you get a new car.

Let’s look at the different coverages available, how to select a deductible, and why you may want to think twice before filing a claim.

Understanding Car Insurance Coverage

Let’s look at each of the categories you’ll see on your car insurance. I’ll walk you through what it usually insures and how to think about how to select an amount in each category.

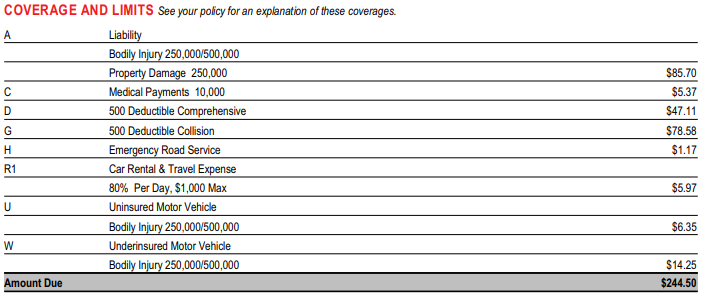

Before we begin, below is a sample policy.

Bodily Injury Liability Coverage

Bodily injury liability coverage may help cover another person’s expenses related to an injury due to an accident you cause.

Below are common areas it could cover:

- Medical expenses

- Legal fees

- Loss of income

- Funeral costs

For example, if you hit another person while driving, and they break their arm, your bodily injury liability coverage may help pay for their medical expenses.

It could also pay legal fees to defend yourself, lost income for the other person if they are unable to work, and funeral costs if you kill someone in an accident,

It’s commonly expressed as two numbers like in the policy above.

In the policy above, it’s listed as “250,000/500,000.” The first number, 250,000, represents the maximum amount of coverage for one person in an accident. The second number, 500,000, represents the maximum coverage for a single accident.

Let’s look at a scenario to bring it to life.

For example, if you are in an accident and hit another car with four passengers, a married couple and two children, and do the following damage:

- Adult 1: $300,000 in lost wages and medical bills

- Adult 2: $100,000 in lost wages and medical bills

- Child 1: No damages

- Child 2: No damages

Somehow, the children are okay, but the adults are severely hurt. They have extensive medical bills and are unable to work for an extended period of time.

In this case, you don’t exhaust the total coverage for the single accident, but you do exhaust the coverage for Adult 1. Because you only had $250,000 per person, Adult 1 will only receive $250,000 – not $300,000.

They may decide to sue you for the remaining $50,000, or, if you have umbrella insurance, that could have possibly help bridge the gap.

In general, I prefer purchasing the maximum amount of bodily injury liability coverage possible. The maximum is often around $500,000.

If you hit one high-income earning person who is unable to work for an extended period and had significant medical bills, it would be easy to exhaust a policy with lower limits. And that’s just one person.

What if you hit multiple cars and injured multiple people?

Nobody likes to think they will ever cause an accident, but it only takes one split second to cause an accident – changing the song, turning around to check on a child, or trying to calm a dog.

Bodily injury coverage can help be the first line of defense to protect your assets.

Property Damage Liability Coverage

Property damage liability coverage may help pay for damage you cause to another person’s property.

Although it’s usually someone’s car, it could be a building, garage doors, or fence, too.

Property damage liability coverage is another area where I would not skimp on coverage.

Although $100,000 can feel like plenty of property damage coverage, you could hit and total one car and exhaust your limits.

In major metropolitan areas, it’s common to drive around cars that are worth far more than $100,000.

That’s not even counting if you caused an accident where multiple cars were involved and you hit other property, such as a building.

Like bodily injury liability coverage, if your policy doesn’t cover the damage you cause, someone may sue you for the balance to make you pay out of pocket.

It often isn’t that much more expensive to raise your property damage liability coverage.

I generally suggest $250,000 or $500,000 of property damage coverage to help protect in low probability event situations that could be very expensive.

Medical Payments Coverage

Medical payments coverage may help pay for your or your passengers’ medical or funeral expenses in an accident.

It can also pay for your medical expenses if you or your family members are hit by a car while riding a bike, walking, or riding in someone else’s car.

This is usually an optional coverage you can add to your auto insurance. The most common limits are $1,000, $2,000, $5,000, $10,000, and $25,000.

Below are some of the medical costs it may help cover:

- Health insurance deductibles

- X-rays

- Ambulance fees

- Hospital stays

- Dental procedures

- Funeral costs

Since medical payments coverage is limited, whether you decide to add it to your auto insurance depends on how much you want to self-insure for this type of scenario.

Personally, I like the peace of mind $5,000-$10,000 of coverage provides because it would usually pay a good chunk of someone’s health insurance deductible. It’s also relatively inexpensive.

Comprehensive Coverage

Comprehensive coverage may pay for damage to your car caused by the following:

- Theft

- Fire

- Hail

- Floods

- Accidents with animals

- Falling objects (rocks flying up, off cars, trees, etc.)

Comprehensive coverage does not pay for damage to your car from a collision or pay for damage to someone else’s car from a collision.

Comprehensive coverage is typically not required by states, but your lender usually requires it if you finance or lease a vehicle.

If your car isn’t worth very much or you could easily replace it with your savings or investments, you may not need comprehensive coverage.

I usually suggest comprehensive coverage for people with more expensive cars or if you can’t pay out of pocket for a new car.

For example, if your car is worth $7,000 and you have plenty of money to replace it, you may not need comprehensive coverage.

However, if you have a car worth $30,000 and you have plenty of money to replace it, you may still want comprehensive coverage if the thought of paying $30,000 for another car hurts your stomach.

You’ll need to weigh whether you could stomach replacing or repairing your car in the event it is damaged in something other than a collision.

Important Note: This is an area of coverage you’ll want to review if you replace your car. You don’t want to be the person who has a $5,000 vehicle, replaces it with a new vehicle worth $40,000, and forgets to add comprehensive coverage.

Collision Coverage

Collision coverage may help pay to replace or repair your car if it’s damaged in an accident with a vehicle or object, regardless of who is at fault.

For example, collision coverage may cover you if you hit a vehicle, house, or fence. It could also provide coverage if you flip in your own vehicle.

Like comprehensive coverage, collision coverage is usually not required by states, but your lender may require you to purchase it if you are financing or leasing a car.

Also like comprehensive coverage, you may want collision coverage if you have a more expensive vehicle or wouldn’t feel comfortable replacing or repairing your vehicle if it was damaged in an accident with another object.

Important Note: This is another area of coverage you’ll want to review if you replace your car. You may have felt comfortable not having collision coverage with an old car worth $5,000, but you may not feel the same with a new $40,000 car.

Personal Injury Protection (PIP) Coverage

Personal injury protection coverage can also be referred to as no-fault insurance.

It may help pay for medical and non-medical costs, regardless of who is at fault in an accident.

It’s required in some states, optional in others, and can’t be purchased in some. Some states only offer medical payments coverage.

You may be wondering about the difference between PIP and medical payments coverage. PIP can cover medical bills and other expenses, such as loss of income or childcare expenses, whereas medical payments coverage only covers medical bills or funeral expenses.

Similar to medical payments, you’ll need to decide whether PIP coverage is worthwhile to help cover medical expenses, loss of income, or other non-medical expenses.

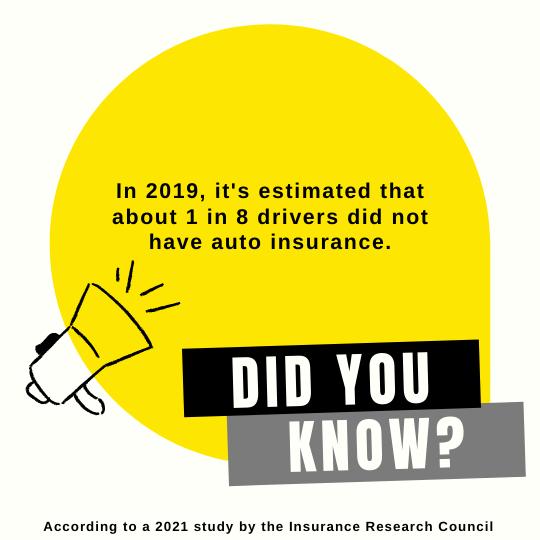

Uninsured/Underinsured Motor Vehicle Coverage

Uninsured and underinsured motor vehicle coverage may help pay for your medical bills and lost wages if you are injured in a car crash caused by a driver who doesn’t have liability insurance or doesn’t have enough.

Although liability coverage is required for other drivers, there are plenty of drivers who do not carry it.

It’s estimated that about 1 in 8 drivers did not have auto insurance in 2019. In some states, it’s estimated that more than 1 in 5 do not have auto insurance.

That doesn’t even take into account people who have auto insurance, but carry the minimum amount, which may not be enough to cover you in an auto accident.

Uninsured or underinsured motor vehicle coverage may help you cover your medical bills and lost wages if the other driver doesn’t have coverage or doesn’t have enough.

Some states require this type of coverage while others do not.

If you have good disability insurance or the funds to cover your medical bills and lost wages, this coverage may be less important.

It’s usually relatively inexpensive to add. Even if you had the funds to cover your medical bills and lost wages, it might be worthwhile for the extra peace of mind.

Emergency Roadside Assistance Coverage

Emergency roadside assistance coverage may help pay for a tow, battery jump, gas delivery, tire change, or to pay a locksmith if you are locked out.

This is a cheap coverage you can add if you want.

Will you ever need it?

Maybe not, but usually for a few bucks per month you can have the coverage.

I could take or leave this coverage.

Rental Reimbursement Coverage

Rental reimbursement coverage may help pay for a rental car or transportation expenses while your car is being repaired after a covered claim.

I used to not be in favor of this coverage because car rentals weren’t very expensive. If you could rent a car for $30 a day, you’d only be out of pocket $420 for two weeks.

However, I’m a big fan of rental reimbursement coverage now. With car rentals going for $75+ a day in many areas, the cost to rent a car is much higher.

If your car takes two weeks to be repaired, that might be over $1,000. Plus, car parts are in short supply and taking longer to get. If they can’t get a part, you might be waiting even longer.

In the past, someone hit my car while it was parked outside my garage, and I am very thankful I had the coverage available. Although I didn’t use it because I could get by without a car for the week or so it took to repair, I looked at car rental rates to see what it would have cost.

I noticed that the rental rates offered through my insurance company were much cheaper than if I went to the car rental company directly. Having the coverage and whatever negotiated rates they have would have saved me a good amount of money.

Pay attention to the maximum per day your insurance company will pay, as well as the limit per occurrence to get an idea of how many days you could rent a car.

If rental car prices go down in the future, I could see dropping this coverage, but with rental car prices where they are, I think it’s a worthwhile tradeoff to add this coverage.

How to Choose a Deductible

Now that you have a better understanding of what coverages are available, you need to decide your deductible.

The deductible is the amount you will pay in a covered claim before your insurance company pays.

For example, if you have a covered claim worth $10,000 and your deductible is $1,000, you’ll be required to pay $1,000 before your insurance company will pay $9,000.

Generally, the lower the deductible, the higher your premium and vice versa.

In most situations, I favor a higher deductible in return for a lower premium.

I usually aim for a $500 or $1,000 deductible. You can have a higher deductible, such as $2,000, but from what I’ve seen in the past, your premium usually doesn’t go down very much.

You can ask your insurance agent to provide the cost for each level of deductible to see how much the premium adjusts.

Then, you can decide which deductible makes the most sense for you.

Think Twice About Filing Claims

Like any type of insurance, think carefully about whether you want to file a claim after an auto accident.

Your insurance company may raise your rates or decide not to renew your policy if you have a certain number of claims.

This is one reason why I generally suggest a higher deductible, too. If your deductible is higher, you are less likely to file a claim for smaller damages.

If you are in an accident, have a $1,000 deductible, and your car has $1,500 worth of damage, you may decide that paying out of pocket for that expense is better because the insurance company is only going to pay $500.

For those who have the funds to cover the deductible, a higher deductible usually makes more sense.

Final Thoughts – My Question for You

I suggest reviewing your car insurance every few years, when you buy a new vehicle, or add a driver to your policy.

Understanding your coverage and how it applies in certain circumstances is important.

Call your agent and ask them to go through your policy with you. Ask questions. Keep asking until you fully understand.

You don’t want to be in an accident only to find out you don’t have coverage for something you thought you had or wish you had.

I’ll leave you with one question to act on.

When will you review your car insurance policy?