One of the most common questions I receive as a financial planner is, “Should I invest or pay off my mortgage?”

The “right answer” depends on the person.

For some people, paying off the mortgage instead of investing makes more sense. For others, investing is a better option.

There are many factors to consider. Plus, this is one of the questions where sometimes the emotional side of the decision (being debt-free) outweighs the economic benefits.

Let’s talk about how a mortgage works, look at an example of paying of a mortgage early, and the pros and cons of paying off your mortgage early instead of investing.

How a Mortgage Works – Principal vs. Interest

First, let’s get a better understanding of how a mortgage works, so you can understand what is happening if you make extra payments towards your mortgage to pay it off early.

Let’s assume the following facts:

- Home Purchase Price: $800,000

- Down Payment (25%): $200,000

- Loan Amount: $600,000

- Term: 30 years fixed

- Interest Rate: 6.5%

In this scenario, your principal and interest payment is $3,792.41.

However, that doesn’t mean you are paying $3,792.41 towards your principal each month. Instead, a portion of each payment is applied to principal and interest.

In the early years, more of the payment is going towards interest, which means you are not paying much towards principal.

For example, with your first payment, here is the split:

- Principal: $542.41

- Interest: $3,250

In other words, after your first mortgage payment, your $600,000 loan was reduced to $599,457.59.

After five years of payments, here is the split with the next payment:

- Principal: $746.01

- Interest: $3,046.40

After five years, your mortgage principal went from $600,000 to $561,665.86. You reduced your loan balance by $38,334.14 despite making $227,544.49 in payments. The other $189,210.35 went towards interest.

This is in contrast to the later years of the loan when you start to pay more principal. For example at the end of 25 years, here is the split:

- Principal: $2,727.75

- Interest: $1,064.66

At that time, the $600,000 loan would be at $193,824.97. You paid down your principal by $406,175.03 despite making $1,137,722.44 in payments. The other $731,547.41 went towards interest.

When you pay down your mortgage early, you are making your normal payment plus extra payments that you can apply towards principal.

Let’s look at an example of paying off a mortgage early.

Example of Paying Off Mortgage Early

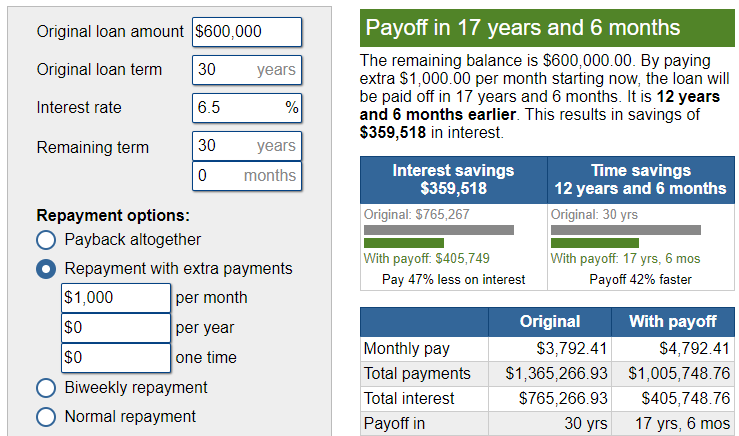

Using the same scenario as before, but making $1,000 extra payments toward principal each month, the loan would be paid off in less than 18 years and you would save about $359,518.17 in interest.

To compare it to year five with no additional payments, your principal loan balance would be $490,991.90 instead of $561,665.86.

Paying off your mortgage early through additional payments can save interest, end the loan early, and free up cash flow.

If you want to calculate how much in interest you can save by paying off your mortgage early, there are many calculators available.

Pros of Paying Off Your Mortgage Early

There are many pros to paying off your mortgage early.

Interest Savings – Guaranteed Returns

When you make additional principal payments towards your mortgage to pay it off early, you are guaranteeing yourself a rate of return. The rate of return is the interest rate on your mortgage.

For example, if you make an extra $1,000 payment and your interest rate is 6.5%, you are saving at that interest rate. It’s interest you don’t have to pay.

You saw in the early example how making extra payments could reduce the total interest paid by shortening the loan.

If your interest rate is high, you’ll save more in interest by paying off your mortgage early compared to someone who has a lower mortgage interest rate.

Debt-Free Sooner

Having worked with hundreds of retirees over the years, this is one of the biggest benefits of paying off a mortgage.

The peace of mind that comes with having no mortgage and being debt free can’t adequately be expressed over the internet.

People love being debt free!

For some people, it gives them peace of mind to retire sooner, move closer to family, or make other life changes that they may have not made with a mortgage.

Create Cash Flow for Other Purposes

Another advantage to paying off your mortgage early is that it can create more cash flow for other purposes.

I’ve talked with many widows who express how thankful they are that their home is paid off, which gives them more spending for other things.

Not having a mortgage may mean “extra” thousands of dollars that can be used for gifting to family members, spent on travel, or healthcare expenses.

It could also mean that much more of a buffer that can be used when the right opportunity presents itself.

When I meet people with terminal illnesses, having a mortgage paid off is often a priority because it means one less thing for the surviving spouse to worry about and one less obligation.

Can Use Equity Later

Paying off your mortgage later could also mean having more equity in your home that you could use later.

If interest rates go down, you potentially could refinance, take cash out of your home, and use it for other purposes.

Another option if you have enough equity later is that you could open a home equity line of credit (HELOC). The HELOC could be used to remodel your home or other opportunities.

Another strategy is to use a HELOC to get the cash needed for a down payment on another home before selling your current one.

For example, if you had a HELOC of $200,000 and needed $150,000 for a down payment on another home, you may be able to use your HELOC to put the down payment, carry two mortgages for a couple months while you sell your home and move into the new home.

Cons of Paying Off Your Mortgage Early

Although there are pros of paying off your mortgage early, there are many disadvantages, too.

Wealth Tied Up – Liquid Funds Become Illiquid Funds

When you pay off your mortgage early, you are taking liquid funds that could easily be used for anything else and turning them into illiquid funds by tying them up into the house.

Although you can access equity in your home, it’s not always the easiest or cheapest to access.

For example, in 2008 and 2020, many lenders stopped offering HELOCs, froze credit lines, and even canceled HELOCs that had not been used.

People often have HELOCs as a back up in case they need to access a large sum of money at once, but they have been some of the first lending products to stop being offered in times of distress (usually when people need them the most!).

HELOCs also typically come with a variable interest rate, which means uncertainty around the payments you may need to make. If you pay off your fixed rate mortgage early and then need to take out equity, you may need to do it at a higher rate, which could end up costing you more in interest.

Be careful about tying up wealth in your home.

The equity in your home is not always easy to access or cheap.

Fewer Tax Deductions

Another disadvantage of paying off your mortgage early is that you may have fewer tax deductions.

Mortgage interest is a tax benefit, but only if you are itemizing your deductions.

Since the standard deduction was raised in 2017, this is less of a benefit since fewer people are itemizing their deductions, but it may become more important again in 2026 if these temporary tax changes revert back to the rules in place in 2017.

Opportunity Cost of Other Financial Goals

If you are paying off your mortgage more quickly, then you have less funds available for other goals.

Many people try to pay off their mortgage quickly, but don’t recognize the opportunity cost of making additional payments.

The opportunity cost may be fewer vacations with your family, less retirement savings, or gifting to your family.

While having your mortgage paid off can be a good feeling, don’t discount what else the money could do for you.

Not Giving Inflation Time to Work

Another con of paying off your mortgage more quickly is that you are not giving inflation time to work.

While your property taxes and insurance costs may increase over time, your principal and interest payment will remain fixed, assuming you got a fixed rate mortgage.

While the principal and interest may feel like a large sum today, it may not feel as big in 20 years because inflation ate away at the value.

For example, if you talk to someone who bought their house 10 or more years ago, their principal and interest payment may be $1,000 while most people getting a mortgage today might be over $2,000. Although the $1,000 may have felt large to them 10 years ago, it likely feels like a small amount and easier to pay today.

Pros of Investing Instead of Paying off Your Mortgage

While paying off a mortgage early has its pros, so does investing.

Higher Risk and Potentially Higher Returns

Any time you invest, there is uncertainty and risk. You don’t know what your rate of return will be or the sequence of your returns.

Investing comes with more risk and uncertainty whereas if you pay off the mortgage, you know the rate of return you are receiving.

For example, if your mortgage interest rate is 4%, you are earning 4% by paying down your mortgage because it’s interest you won’t have to pay.

When you invest, the rate of return remains a question mark. Although there is data showing ranges of returns for stocks and bonds over different time periods, it’s not guaranteed.

It merely gives you an idea of what has happened historically.

Historically, the S&P 500 has returned around 8% to 10%, depending on the time period measured. I quote the S&P 500 because we have longer periods of data for it than a globally diversified portfolio.

You are taking more risk when you invest, but you also have the opportunity for greater wealth.

Assuming the sequence of returns is not bad, if your mortgage interest rate is 4%, and you can earn 8%, you may come out ahead.

Please keep in mind you may be investing in a diversified portfolio of stocks and bonds, so your returns may be lower than 100% in the S&P 500.

More Liquid Assets

Another advantage of investing extra money instead of paying off that mortgage is that you have more liquid assets.

As discussed earlier, your home is an illiquid asset, which means it’s challenging to turn it into spendable money.

If you invest in publicly traded assets that are liquid, you can use that cash as opportunities come up.

For example, if you want to pay for a vacation for your entire family, you can. There is no struggle about where you will come up with the funds or feel like you can’t do it.

In my experience, people feel much more comfortable paying for once in a lifetime experience (or even everyday experiences) if they have more readily available assets to pay for it.

If it’s tied up in the home, you may miss out on those life experiences.

Cons of Investing Instead of Paying off Your Mortgage

There are also cons of investing instead of paying off your mortgage.

Market Risk

If you invest, you are taking on market risk.

You could invest extra money, and you could go through a time period like the Tech Bubble or the Global Financial Crisis. You may see your investment drop more than 30%.

At least for that short time period, you may have been better off making extra payments towards the mortgage; however, please keep in mind investing is for the long term.

It can feel uncomfortable investing extra, watching the market go down, and thinking about the alternative choice of paying off the mortgage that you did not do.

If you are going to invest, you need to have a long-term mindset. Otherwise, you may be even more tempted to pay off the mortgage more quickly at some of the worst times (when markets are down).

Unknown Rate of Return

When you are investing, you are trading in a known rate of return (your mortgage interest rate) for an unknown one.

Depending on how you are investing the funds and what’s happening in the world, you may come out ahead investing, but you may not.

Personally, I’d have a hard time aggressively paying down a fixed-rate mortgage taken out around 2020 when mortgage rates were at historic lows.

That’s a low hurdle rate to overcome when investing. As of this writing, there are savings accounts paying more than those mortgage rates. You could even lock in a 20 or 30 year treasury bond that pays more than those mortgage rates.

Although you can lock in a rate of return with a bond (to the extent it does not default), many people are likely going to pick a mix of stocks and bonds that may fall in line with historical returns, but you never know what the rate may be.

Less Equity in Your Home

Another con of investing is that you may end up with less equity in your home.

I don’t necessarily see this as a bad thing because if you are saving the money elsewhere instead of spending it, you should have other liquid assets that can be used for big life purchases.

However, some people like having equity in their home knowing that it’s there if they ever want to sell and downsize or take out a HELOC to remodel a portion of their house.

Final Thoughts – My Question for You

Deciding whether to invest or pay off your mortgage is a personal, often emotional decision.

You can quantify the choices to a certain extent, but ultimately, some people feel better having a paid off mortgage, which is the most important priority.

Before you pay it off, consider what you are giving up.

- Do you have other liquid funds for a down payment if you need to move?

- Are you considering the opportunity cost of having more money tied up in your home?

- What’s the mortgage interest rate compared to the possible rate of return you might get investing?

I’ll leave you with one question to act on.

How will you decide whether to pay off your mortgage?