Last Updated on December 18, 2024

Are you afraid that you may be paying too much in taxes?

Although it’s close to the end of the year and tax planning should be year-round, don’t be the person who finds out in 2024 that they paid the IRS too much for 2023!

If you haven’t done any tax planning for 2023 yet, now is the time.

While many reactively plan for taxes, proper tax planning is not based on year-to-year numbers. Good tax planning looks at your lifetime tax liability and develops strategies to minimize the amount you pay throughout life.

Here are 7 ideas to consider before the end of the year to strategically reduce the taxes you pay over your lifetime.

Tax Planning Checklist Step 1: Complete Required Minimum Distributions (RMDs)

The SECURE Act 2.0 changed RMD ages.

Instead of the RMD age starting at age 72, which was changed with the SECURE Act of 2019, it pushed RMDs back to ages 73 and 75, depending on your year of birth.

For those with a birth year of 1951 to 1959, RMDs will begin at age 73. For those born in 1960 or later, RMDs will begin at age 75.

For those who were already subject to RMDs, you should continue taking your RMDs. The new law did not change it for people who had already begun taking RMDs.

If you have an RMD you need to complete before December 31, don’t wait until the last minute to do it!

Custodians get very busy near the end of the year, and the penalty for not completing an RMD is 25% of the amount that should have been distributed. For example, if your RMD is $50,000, the penalty for not distributing your RMD by December 31 would be $12,500. This makes it a very important step on the checklist because the penalty can be significant! The penalty can be reduced down to 10% if you take it within a “correction window” (typically within the end of the second calendar year following the year the RMD should have been distributed), but even that would mean a $5,000 penalty based on an RMD of $50,000.

Since the SECURE Act 2.0 changed the RMD beginning dates, nobody is starting RMDs for the first time in 2023.

However, pay special attention to those starting RMDs for the first time in 2024. For people who begin RMDs for the first time in 2024, your first RMD would be due by April 1 of 2025; however, if you wait until 2025, you’ll have two RMDs to complete in 2025. Depending on your tax situation, you may want to complete it in 2024.

If you do not need your RMD for spending, you could reinvest the proceeds into a taxable brokerage account. Most custodians allow you to electronically move cash between your IRA and your brokerage account where you can invest it.

If you do this in the future, you may want to consider moving it to your brokerage earlier in the year, where the tax treatment is generally better. If you take the RMD amount and invest it into your brokerage account and the market goes down, you can tax-loss harvest. If the market goes up, you will get capital gains treatment on the future sale instead of ordinary income treatment. Capital gains tax rates are generally lower.

Qualified Charitable Distributions (QCDs)

If you want to give to charity, you could also do a Qualified Charitable Distribution (QCD). QCDs are one of the best ways to give because for each dollar you give up to $100,000 per year, the distribution is not taxable and can satisfy your RMD.

For example, if your RMD is $20,000 and you distribute $5,000 as a QCD, only $15,000 is taxable to you. If you distribute $20,000 as a QCD, none of it is taxable. You can distribute more than your RMD as a QCD (up to $100k), but it does not carry forward to satisfy your RMD for the following year. If you distribute more, you reduce the balance in your retirement account, which could make future RMDs smaller.

Inherited IRAs

For those who are not age 73 or older, but have an Inherited IRA or Inherited Roth IRA, you may need to complete a RMD. The distribution rules are complicated and vary depending on many factors.

Generally, for account owners who died in 2020 or later, the account needs to be distributed by December 31 of the 10th year after the year in which the account holder died. For example, if someone died in 2020, the account would need to be fully distributed by December 31, 2030. Distributions can be taken earlier, but the account needs to be completely distributed by then.

It’s still unclear whether beneficiaries need to distribute RMDs for years 1 through 9, but the IRS said no penalties will apply if beneficiaries did not distribute RMDs in 2021, 2022, or 2023. Beneficiaries may still want to consider distributing an Inherited IRA RMD this year if they find themselves in a lower bracket than they may be in the future. The rules around Inherited RMDs are not final, which means you’ll want to continue watching for notices from the IRS to decide what to do in 2024 and beyond.

If the account owner died prior to 2020, distributions can generally be stretched over your lifetime using the Single Life Expectancy table.

Please keep in mind that distribution rules are complicated, and your situation may vary from the normal process. You should consult your tax advisor or financial planner about your individual situation.

Tax Planning Checklist Step 2: Analyze Opportunities for Roth Conversions

You may want to consider a Roth conversion before the end of the year. Unlike contributions, which can be contributed until your tax filing deadline (not including extensions), Roth conversions have to be done in the calendar year for them to count in that year’s income.

There are only a few years left to take advantage of the lower tax rates created by the Tax Cuts and Jobs Act.

The current rates, which are lower and wider, are due to sunset at the end of 2025, which means starting in 2026, we’ll be back to the 2017 tax rates adjusted for inflation. Those tax rates are higher and have a narrower income range within each bracket.

Below are the 2023 and 2017 tax brackets for you to see how much lower the tax rates are today.

| Married Filing Jointly 2023 Tax Brackets | Married Filing Jointly 2017 Tax Brackets | ||

| Taxable Income | Tax Bracket: | Taxable Income | Tax Bracket: |

| $0 – $22,000 | 10% | $0 – $18,650 | 10% |

| $22,001 – $89,450 | 12% | $18,651 – $75,900 | 15% |

| $89,451 – $190,750 | 22% | $75,901 – $153,100 | 25% |

| $190,751 – $364,200 | 24% | $153,101 – $233,350 | 28% |

| $364,201 – $462,500 | 32% | $233,351 – $416,700 | 33% |

| $462,501 – $693,750 | 35% | $416,701 – $470,700 | 35% |

| $693,751+ | 37% | $470,701+ | 39.6% |

| Single 2023 Tax Brackets | Single 2017 Tax Brackets | ||

| Taxable Income | Tax Bracket: | Taxable Income | Tax Bracket: |

| $0 – $11,000 | 10% | $0 – $9,325 | 10% |

| $11,001 – $44,725 | 12% | $9,326 – $37,950 | 15% |

| $44,726 – $95,375 | 22% | $37,951 – $91,900 | 25% |

| $95,376 – $182,100 | 24% | $91,901 – $191,650 | 28% |

| $182,101 – $231,250 | 32% | $191,651 – $416,700 | 33% |

| $231,251 – $578,125 | 35% | $416,701 – $418,400 | 35% |

| $578,125+ | 37% | $418,401+ | 39.6% |

If you are in the 22% or 24% marginal tax bracket, it’s a particularly good time to analyze whether a Roth Conversion makes sense because those in the 22% tax bracket today may find themselves in the 25% tax bracket and those in the 24% tax bracket may find themselves in the 28% tax bracket in 2026.

Roth conversions don’t make sense for everybody. You’ll need to consider your IRA balance, future income, how your investments are structured, and how much you want to hedge against higher tax rates in the future.

Generally, if you have more than $750,000 in a retirement account and are 73 or younger, you may want to explore Roth conversions with a financial planner or accountant by comparing your current year tax bracket to a future estimated tax bracket. If you can pay a lower tax rate now than you anticipate paying in the future, it may make sense to do a Roth conversion.

Tax Planning Checklist Step 3: Proactively Tax-Gain and Tax-Loss Harvest

Although many people think paying no taxes is a good thing, it could be a missed planning opportunity that costs you thousands of dollars or more.

It’s like going on an all-inclusive vacation, but only staying on one part of the beach and eating the same meal at the same restaurant every day. You should have done more, but you missed out.

Many people don’t understand how ordinary income affects capital gains and vice versa.

Most people are familiar with ordinary income tax rates because it’s how most of us are taxed while working. If you earn $100 while working, you have $100 of ordinary income. When someone retires or is no longer earning as much ordinary income, they generally fall into a lower income tax bracket, but they also fall into a lower capital gains bracket — sometimes even 0%.

Capital gains are recognized when you sell an investment for more than what you bought it for in a non-retirement account. For example, if you bought a stock for $10 and sold it for $30 in a brokerage account, you would have $20 worth of capital gains.

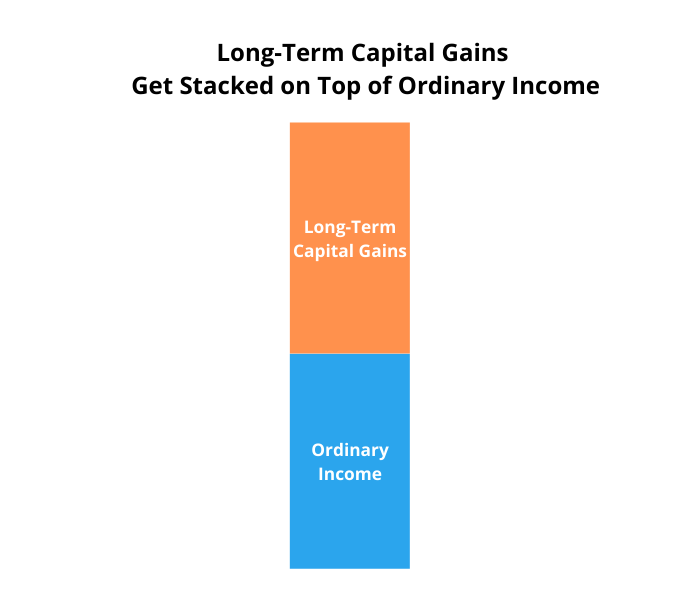

The way ordinary income tax rates and capital gains tax rates are connected is that capital gains are stacked on top of ordinary income.

Example of how capital gains are stacked on top of ordinary income

What this means is that your capital gains tax rate can go up or down depending on your ordinary income, but your capital gains are always taxed at their own capital gains tax rate – not ordinary income tax rates.

Long-term capital gains tax brackets are the following:

| Capital Gains Tax Rate | Married Filing Jointly Taxable Income | Single Taxable Income |

| 0% | $0 – $89,250 | $0 – $44,625 |

| 15% | $89,251 – $553,850 | $44,626 – $492,300 |

| 20% | $553,851 or more | $492,301 or more |

Example 1 of 0% Capital Gains Bracket – No Income

Let’s look at an example to clarify.

Let’s say you retired, and for simplicity, you earn no income and take the standard deduction ($27,700) as a married couple.

If you do nothing, you’ll pay $0 in taxes, but you missed out on using your standard deduction. It was wasted. You could have had $27,700 in income and still paid $0 in taxes because it would have been fully offset by your standard deduction.

In the case of capital gains, you could have realized $116,950 in long-term capital gains and paid $0 in taxes. Yes, you heard me right.

You could have realized $116,950 in long-term capital gains and paid nothing in taxes.

How does that work?

Remember, ordinary income has its own tax bracket. Capital gains get stacked on top of ordinary income and are taxed at their own rate.

Example 2 of 0% Capital Gains Bracket – $40,000 Income

Let’s take it a step further and say you have $3,000 of taxable interest and $37,000 of ordinary income from part-time work.

In this case, your gross income is $40,000. Your taxable income is $40,000 minus the $27,700 standard deduction, bringing it to $12,300.

Your total income tax is $1,230.

If you do nothing, you are still missing out on the opportunity to recognize long-term capital gains and pay zero tax on those capital gains.

Example 3 of 0% Capital Gains Bracket – $40,000 Income and $69,250 of Long-Term Capital Gains

You could recognize $76,950 in long-term capital gains and still be in the 0% capital gains tax bracket. Let’s go over the math.

$3,000 of taxable interest

+ $37,000 of ordinary income

+ $76,950 of long-term capital gains

= $116,950 of gross income

– $27,700 standard deduction

= $89,250 taxable income

The $89,250 figure is the top of the 0% capital gains bracket. You can do your own calculations using this calculator.

If you already had taxable income of $89,250 from ordinary income, your capital gains will get stacked on top and be taxed at 15%.

But, as long as you have lower income and can fill up the 0% capital gains tax bracket, you should consider taking advantage of recognizing income if it results in not paying additional taxes.

Importance of Mock Tax Projections

You should be aware that capital gains can affect the taxation of other sources of income, such as Social Security. To ensure you are not raising your taxes while still being in the 0% capital gains bracket, you should do a mock tax projection to see how your tax liabilities change if you recognize capital gains.

Mechanics of Tax-Gain Harvesting

The mechanics of tax-gain harvesting are easy. You simply need to sell an investment or part of an investment with a long-term capital gain and then buy it back immediately. You don’t need to wait like with tax-loss harvesting.

You could sell “Investment A” today and buy “Investment A” back a second later.

Tax-Loss Harvesting

The other thing to double check before year-end is if you have tax-loss harvesting opportunities. If an investment went down in value, you could sell it at a loss to recognize the loss, and use that loss to offset other gains. If you don’t have gains, you can offset up to $3,000 of ordinary income per year. Ideally, you should proactively be doing this throughout the year and not just at the end of the year.

As losses occur, you usually want to take them.

I do this by monitoring losses throughout the year and if a loss is meaningful, I sell the position and replace it with a similar investment. After 31 days, I may swap back to the original investment if there is not a huge gain. If there is a huge gain or the substitute investment is good enough, I keep the similar investment.

Tax Planning Checklist Step 4: Complete Charitable Giving

Like the other tax strategies, don’t wait until the last week of December to decide to give to charity.

Review it earlier and ask yourself:

- Have you supported the charities you intended?

- Did you give the amounts you wanted?

- Do you want to set up recurring donations?

- Have you considered giving more unrestricted funds?

- Did you give cash or pay by credit card when another method would be more tax efficient?

Although QCDs are a great way to give, another option to consider is a Donor-Advised Fund (DAF).

DAFs are a great way to bunch a few years worth of gifts into one year. While you can contribute cash to a DAF, a better method might be to donate highly appreciated investments that have been held longer than a year.

For example, you could contribute $20,000 worth of an individual investment you bought for $5,000. By donating it, you avoid the $15,000 capital gain and still receive a charitable deduction of $20,000. Plus, the funds can be invested in the Donor-Advised Fund and you can request grants to charities you would normally support. A grant is simply a request to the sponsoring organization to write a check from your Donor-Advised Fund to the charity of your choice.

Whether you use a Donor-Advised Fund or another method of giving, don’t forget to review your charitable giving for the year.

Tax Planning Checklist Step 5: Review Contributions to Tax-Advantaged Retirement Accounts

If you are still working and want to max out your retirement contributions, check that your last paycheck or two will contribute enough to your retirement account to equal $22,500. If you are over age 50, you can make a $7,500 catch up contribution for a total of $30,000.

If you have access to an HSA, consider making contributions of $3,850 for self-only or $7,750 for families. HSAs are triple tax advantaged, meaning you get a tax deduction, earnings grow tax deferred, and withdrawals for medical expenses are tax-free.

One popular strategy is to make regular contributions to an HSA, invest it, and spend out of pocket. It’s a way to build up a larger account that can be used tax-free for medical expenses later.

Tax Planning Checklist Step 6: Review Tax Withholdings and Estimated Tax Payments

After you know your income for the year, such as wages, RMDs, Roth conversions, and long-term capital gain amounts, you can review your tax withholdings.

To avoid underpayment penalties, you need to pay 90% of your current year tax liabilities or 100% of your prior year tax liabilities if your adjusted gross income is $150,000 or less (110% of your prior year tax liabilities if your adjusted gross income is $150,000 or more).

If you have not withheld enough in taxes and have income that can be withheld, consider having more withheld instead of making an estimated tax payment because tax withholdings are treated as being withheld throughout the year. This means if you are underpaid, you can bridge the shortfall late in the year and avoid underpayment penalties.

The same cannot be said for estimated tax payments. If you wait until the last estimated tax payment deadline and make a large estimated tax payment, you may still have an underpayment penalty if more should have been withheld throughout the year.

This is why it’s important to proactively plan for taxes starting when you file your tax return and throughout the year.

Tax Planning Checklist Step 7: Decide Whether to Gift to Family

Lastly, this is an excellent time of year to consider gifting money to family.

In 2023, every person can give $17,000 to as many individuals as they want and not need to file a gift tax return. In 2024, this amount may increase.

What this means is if you want to give $17,000 to each child or grandchild, you can do it without any gift tax consequences.

If you give more than $17,000 to any single person, then you would need to file a gift tax return. No gift tax is due, but it does reduce your federal lifetime exemption amount, currently at $12.92 million per person.

If you are looking to superfund a 529 plan, give family extra spending cash, or gift money to a child who is working in order for them to fund a Roth IRA, now is a great time of year to do it.

Final Thoughts – My Question for You

With the stock market down this year, there are many tax planning opportunities.

Instead of waiting until December, consider taking 15 minutes to go through this checklist to see if you are missing opportunities to reduce the amount of taxes you pay over your lifetime.

Not taking action could mean paying more taxes than you are legally obligated. Do you want to pay more in taxes?

As I once heard, “Pay all the taxes you owe, but don’t leave the IRS a tip.”

Which steps will you take to reduce the likelihood that you are leaving the IRS a tip?