Last Updated on February 14, 2024

Stock market declines don’t have to be full of bad news.

There are stock market decline silver linings and potential opportunities you can take advantage of during a market decline.

I know it’s not enjoyable to watch your investment portfolio decline in value, feel like the economy is on shaky ground, and wonder when prices will recover; however, there are a few reasons to see the glass as half full as opposed to half empty.

Let’s look at the silver linings of stock market declines and what you can do about them.

Valuations are Cheaper

The major silver lining is the valuation on stocks often becomes cheaper, which generally means future expected returns are higher.

I’ll explain more later, but let’s set the groundwork to understand it first.

Have you ever been to an auction where bidding gets out of hand?

A few people start bidding on a sought after item and before you know it, they are bidding far more than it’s worth. Everybody watches it and thinks, “It can’t be worth that amount of money!” Whether it is worth it or not, that’s what people are willing to pay for it at that given moment, which technically, makes it worth it.

The same phenomenon can happen with stocks.

I’m going to get technical for a moment to help explain valuations, but I’ll incorporate charts and analogies to make it easier to understand.

Price-to-Earnings Ratio and Valuations

When you buy a stock, you are buying future cash flows. There is a common ratio known as the price-to-earnings ratio, or P/E ratio, for short.

It’s calculated by dividing the market value of a stock by the company’s earnings per share. It could be the last quarter of earnings or a forward projection, but it tends to be a small snapshot in time.

For example, if the market value of a stock is $100, and the stock has earnings per share of $5, it has a P/E ratio of 20 ($100/$5). The way to interpret that P/E ratio is that investors are willing to pay $20 for $1 of earnings.

If the numbers seem too intangible, let’s think about it using magical chickens. Instead of a hen laying up to one egg per day, you had a magical chicken that could lay 5 eggs per day. If you paid $100 for that chicken, you would be paying $100 for 5 eggs per day. The price-to-eggs ratio, a term I made up, is 20.

The P/E ratio is a way to compare how expensive (overvalued) or inexpensive (undervalued) a stock is relative to another company. The higher the P/E ratio, the more expensive a stock is and the lower the P/E ratio, the less expensive a stock is.

For instance, if you had a stock with a P/E ratio of 5, you are paying $5 for $1 of earnings. If you had a stock with a P/E ratio of 95, you are paying $95 for $1 of earnings.

Stocks often have higher P/E ratios when investors expect higher growth from a company. It could be new technology, processes, products, users, or anything else that would drive earnings in the company.

P/E ratios also vary by industry. For example, banks often have lower P/E ratios than other industries because growth is limited, they are cyclical, meaning they often go up and down with the economy, and are heavily affected by changes of interest rates.

There are many criticisms of the P/E ratio, which could be an entire series of blog posts, but let’s leave it at this baseline of knowledge to get back to my original point – that when stocks decline, valuations on stocks often become cheaper, which generally means future expected returns are higher.

Magical Chickens to Explain Valuations

Let’s go back to the magical chickens again.

You bought a magical chicken for $100 that could produce 5 eggs in a day, but then a storm is forecasted that threatens the chicken. It could die. It could become stressed and lay less eggs. It might be blown away, and it could be days before you find it again and can collect eggs.

You aren’t sure if you want to keep the chicken, so you decide to see what magical chickens are selling for. You learn that instead of $100 that you paid for it, people are offering $90 because of the uncertainty around the storm. The price-to-eggs ratio is now 18 instead of 20 when you bought it. Valuations have come down.

You wait longer, and the storm forecast becomes worse. Now, the magical chickens are selling for $70 because people are worried about less eggs being collected during a prolonged storm. Your chicken is still laying 5 eggs per day, which makes the price-to-eggs ratio 14.

Your neighbor decides to sell their chicken to you for $70 because they can’t take the uncertainty. You now have two magical chickens laying 10 eggs per day.

The storm passes, does some damage, but your magical chickens survive.

You are curious what chickens are selling for now on the open market. They are back to $100.

Some time passes and a few innovations are made that allow the magical chickens to produce 6 eggs per day instead of 5, which causes the price of the magical chickens to go up.

Each of your magical chickens is now worth $120.

When the magical chicken market went down in value, valuations came down, which didn’t feel good, but expected future returns went up at that point.

When your neighbor sold you a chicken for $70, you knew you were still buying a solid chicken that could produce eggs, but there were some risks to how many eggs it could produce and whether it would survive. You knew historically that chickens traded at around $100, and there was no reason to expect them not to reach that level at some point in the future. You simply didn’t know when that would be.

That’s what I mean when I say when stock markets decline, valuations often decline with them, which makes future expected returns higher.

If you bought a chicken for $120 when they historically traded at $100, there is less room for prices to go up, unless people value magical chickens differently in the future, eggs become more expensive, or innovations happen that allow the magical chickens to produce more eggs per day.

Let’s get back to stocks and a better measure of valuation than the P/E ratio.

CAPE and Future Expected Returns

Although the P/E ratio is helpful, many argue a better measure of valuation is the CAPE ratio, also known as the Shiller P/E or PE 10 Ratio.

It’s calculated by dividing the market value of a stock by the average of a company’s inflation-adjusted earnings for the last ten years.

It helps smooth out fluctuations in earnings over a market cycle instead of a point in time. The P/E ratio looks at a small snapshot in time, so it may only incorporate what happened last quarter, which may not accurately reflect the company’s success or failures.

It would be like taking all the eggs produced by a chicken over the past 10 years, adjusted for inflation, instead of what the chicken produced last quarter.

So, what do I mean when I say that when stock markets decline, valuations become cheaper, which generally means future expected returns are higher? Let’s dig into the details.

The CAPE has been tracked for more than 100 years and has a long-term historical average of about 17.

Generally, when you have a higher valuation (higher CAPE), future returns are generally lower. The opposite is also true. When valuations are lower, future returns are generally higher.

I say generally because it’s not a perfect relationship, and there are periods of time where it doesn’t hold true.

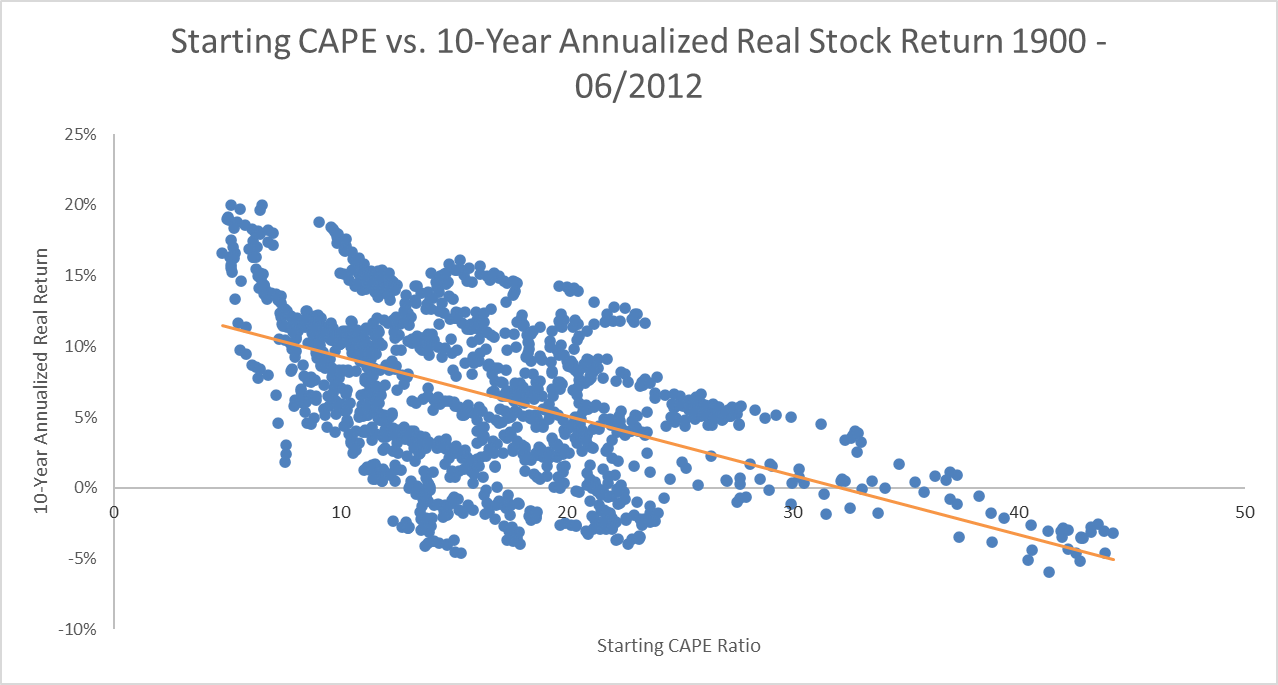

Let’s look at the starting CAPE for U.S. stocks and the return over the next 10 years between 1900 and June 2012.

As you can see, generally, the higher the starting CAPE ratio, the lower the return is in U.S. stocks over the next 10 years.

It’s not perfect.

There are time periods with high valuations that have decent returns, and there are time periods with low valuations that have poor returns.

“Okay, but the early 1900s don’t count”, you may be thinking.

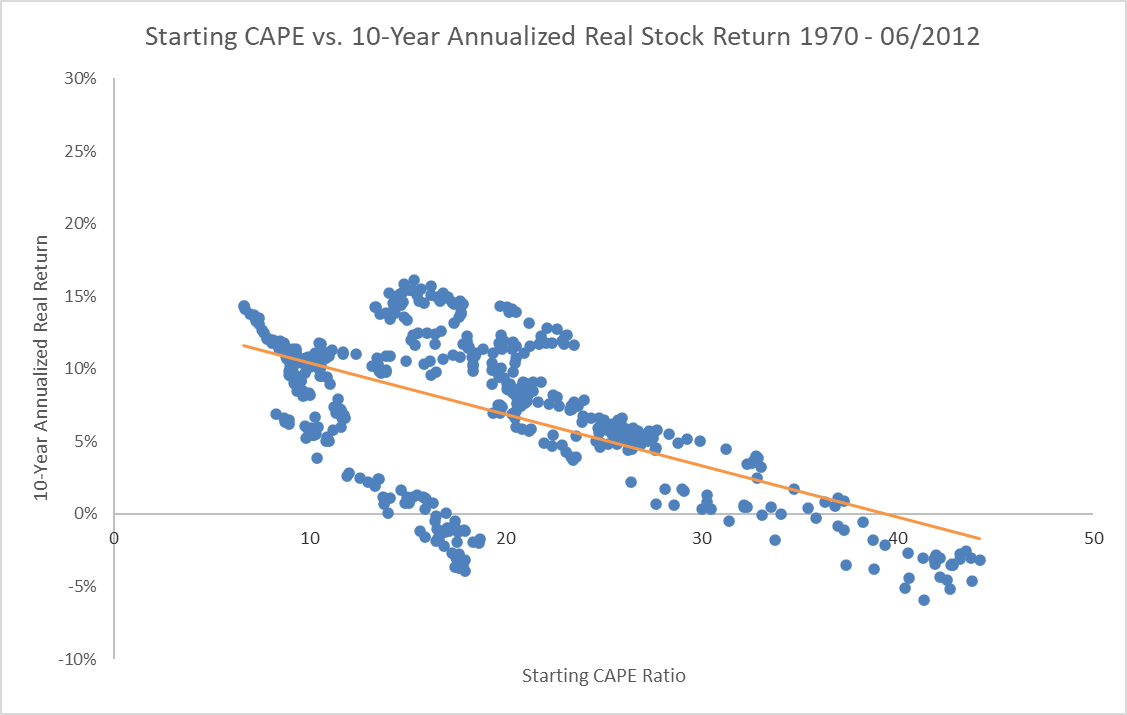

Let’s look at 1970 until June 2012.

There is a very similar relationship. Generally, when the starting CAPE ratio is higher, it means lower future returns.

“Okay, but the last two decades have seen growth in technology, and the world is different”, you may be thinking.

Still, a very similar relationship exists. A lower starting CAPE ratio generally has meant higher returns over the next 10 years.

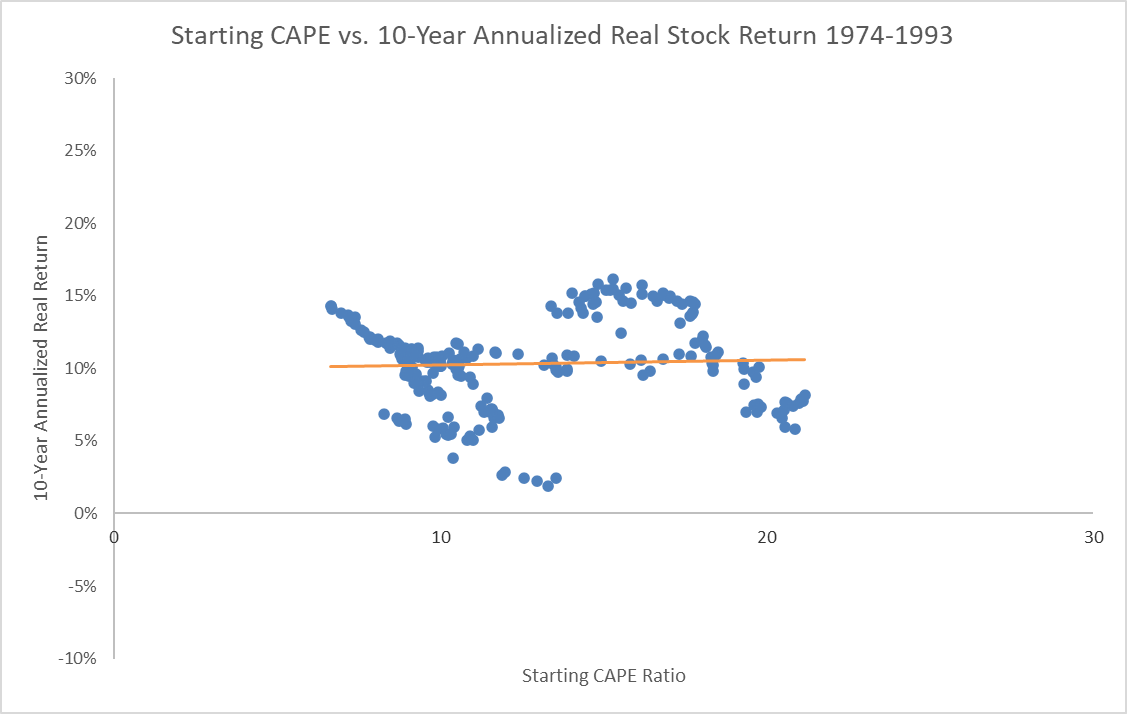

There have been time periods where this relationship hasn’t held. In the mid-70s, 80s, and early 90s, the starting CAPE ratio didn’t mean higher or lower returns over the next 10 years.

As you can see, the line is slightly slanting upward, but for the most part is flat. A high starting CAPE ratio didn’t mean lower future returns.

This is why I say generally a higher starting CAPE ratio means lower future returns.

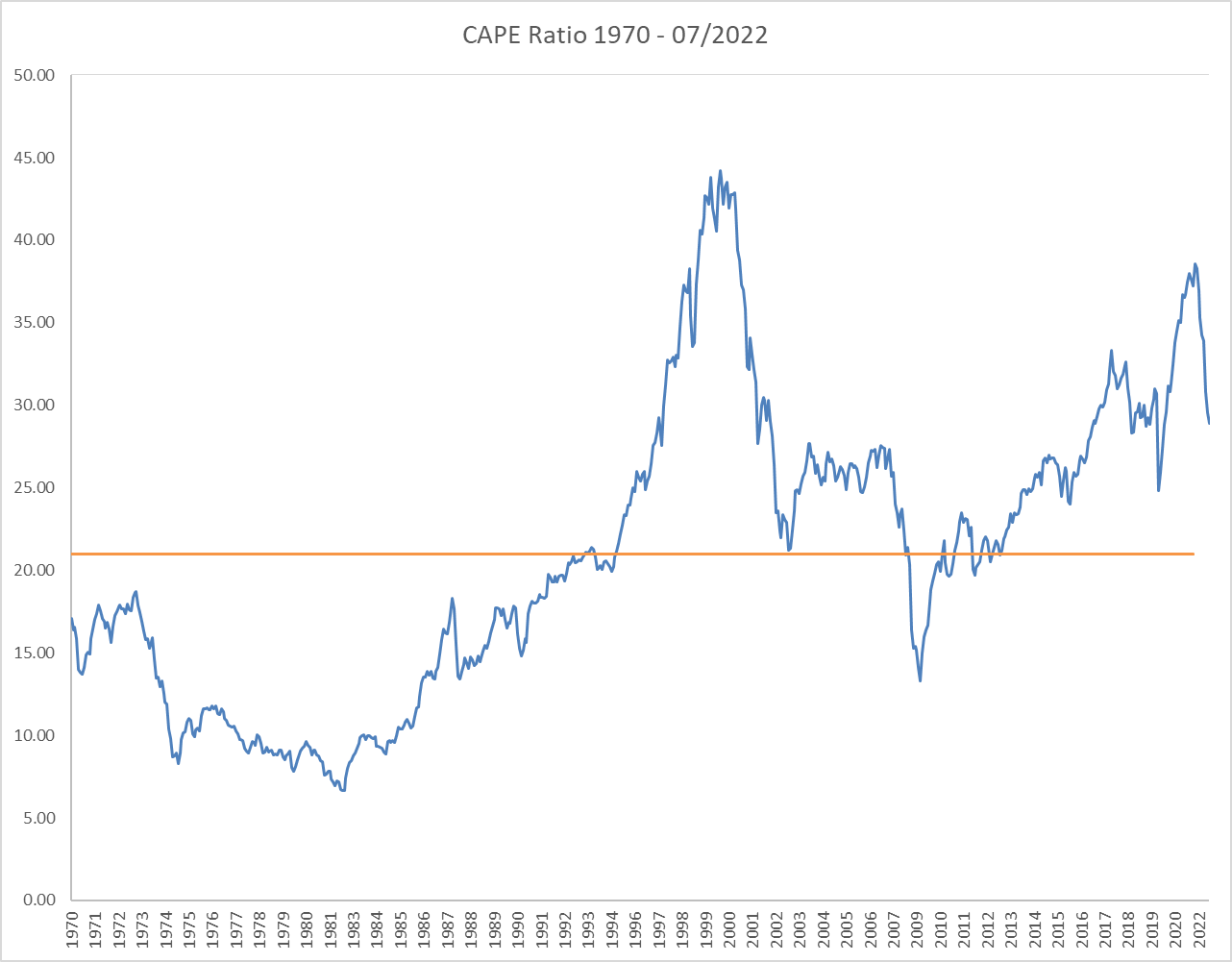

When stock markets decline, CAPE ratios tend to decline with it. You can see in the chart below how the CAPE ratio has changed since 1970.

The average CAPE ratio over this time period was approximately 21, though if you take it back to the late 1800s, it’s closer to 17. I decided to track it from 1970 mostly as an arbitrary point, but also to discount some of the early data for anybody who says what happened in the late 1800’s and early 1900’s are not relevant today.

As you can see, the CAPE ratio has been higher than the historical average for most of the past decade.

In December 2021, it was over 38. As of July 2022, it was almost 29. It’s still high relative to historical averages, but it is lower than it was in late 2021.

In December of 2021, it was tough to say future expected returns would be high given the CAPE ratio. It’s always possible, but unlikely given the historical relationship.

Remember, higher CAPE ratios are generally associated with lower returns over the next 10 years.

As with any point in time, it’s difficult to say what returns over the next 10 years will be, but it looks more promising in July of 2022 than it was in December of 2021.

That’s the silver lining of market declines. Valuations are closer to historical averages, which means future expected returns are higher than they were before. Some of the froth, mania, and “this time is different”, is taken out of the market.

To be clear, I’m not advocating for using the CAPE ratio as a market timing tool. I don’t change my investment strategy based on it, but it is a good expectation setting tool. If the CAPE ratio is higher, it’s reasonable to expect lower returns in the future than the recent past.

A CAPE ratio is not useful for market timing decisions. Sometimes, high valuations still lead to high returns. Sometimes, high valuations lead to positive, but low returns. Sometimes, high valuations lead to negative returns.

There is always the possibility valuations will be higher going forward than in the past. Perhaps people are simply willing to pay more for earnings.

Lastly, keep in mind we’ve been looking at 10 year returns. If you extend it out and look at 20 or 30 year returns (many people’s timeframe for spending money), the data is more clumped together and less sloped. This means the relationship between your starting CAPE ratio and future returns is less strong because you have a reversion to a mean. You get multiple market cycles in a 20 or 30 year period, which smooths out the return closer to historical average. You can get more variability within a 10 year period depending on where you start with valuations.

Key takeaways:

- Low CAPE ratios generally mean higher future returns, but not always.

- CAPE is not a market timing tool, but it can be used as an expectation setting tool.

- The starting CAPE ratio is less relevant for those with 20+ year timeframes, which is the case for many people.

If you are looking for more reading about CAPE predicting future returns, I recommend this article, and if you are looking at different models to estimate future returns, I recommend this one.

Opportunities When Stock Markets Decline

Now that you understand valuations and future expected returns, let’s talk about what opportunities exist when stock markets decline.

Roth Conversions

Another silver lining of a stock market decline is the opportunity to do Roth conversions when stock prices are depressed.

If you’ve already decided a Roth conversion strategy makes sense for you, a stock market decline can be an excellent time to do a Roth conversion.

The benefit of doing it during a stock market decline is that you get to convert at a low point, which means any market recovery occurs in the tax-free account instead of the tax-deferred account, and you get to convert a larger portion of your pre-tax account.

For example, let’s say you wanted to convert $100,000 of your $200,000 IRA to your Roth IRA, and that translated to 2,000 shares of ABC ETF at $50 per share. If you converted at those prices, you would move 50% of the account and have 2,000 shares of ABC ETF remaining in your IRA. You would have $100,000 in each type of account.

Instead, if ABC ETF goes down 20% to $40 a share, your IRA balance would decline to $160,000. Then, if you do the Roth conversion, that allows you to convert 2,500 shares instead of the 2,000 shares you were originally planning to equal $100,000. Then, you have 1,500 shares left in the IRA worth $60,000.

Now, you have 37.5% of your IRA left versus 50% compared to if you had done the Roth conversion before the stock market decline

This is a key point of doing Roth conversions during stock market declines. It allows you to convert more shares for the same dollar value. In other words, you can convert a larger percentage of your pre-tax account to a Roth IRA during a stock market decline.

Then, let’s say ABC ETF goes up 40% over the next year because the stock market recovers, bringing it to $56 per share. Now, your $100,000 Roth conversion is worth $140,000, and your IRA balance is $84,000. That’s a split of 62.5% tax-free and 37.5% tax-deferred.

If you had instead done the Roth conversion earlier in the year before the stock market decline, you would have $112,000 in your IRA and Roth IRA (2,000 shares x $56 per share) or 50% tax-free and 50% tax-deferred.

I’m not advocating waiting for a stock market decline to do a Roth conversion. Generally, converting earlier in the year is better because stock markets go up more often than they go down; however, if you had already decided you want to do a Roth conversion and haven’t done one yet, doing a Roth conversion during a stock market decline can be powerful because you are converting while prices are on sale.

Rebalancing

Another silver lining of a stock market decline is the opportunity to rebalance and buy assets on sale.

Watching your portfolio go down in value is never an enjoyable experience, but it does put assets on sale, at least relative to where they were prior.

For example, if you have a diversified portfolio of 60% stocks and 40% bonds and stocks went down, bringing them to 55% of your portfolio and bonds to 45%, you could sell part of your bonds to bring the portfolio back into alignment to 60% stocks and 40% bonds.

It’s a way of buying low and selling high. You are selling the assets that have done well (bonds) to buy the assets that are low (stocks).

People love the concept of buy low and sell high, but many don’t recognize that rebalancing is a way to execute that concept. It can be even harder to carry out when stocks are down because it may feel strange buying an asset that just went down when there is something going on in the world that caused stocks to fall.

Over time, rebalancing based on thresholds can be helpful because you are bringing your risk exposure back into alignment, which may help your returns as the market recovers.

For example, if you don’t rebalance in the situation when your stocks make up 55% of the portfolio instead of 60%, you only have 55% of your portfolio in riskier assets that may benefit from a market recovery. On the other hand, if you rebalanced to 60% stocks, you have more assets that may participate in the recovery.

For example, if bonds stay flat during the recovery (for simplicity sake) and stocks go up 10%, your return would be 5.5% if you had 55% stocks and 6% if you had 60% stocks.

While that may seem small, over time, that can add up to a significant amount of money.

Rebalancing is a silver lining you may be able to take advantage of during a stock market decline.

Tax-Loss Harvesting

Lastly, tax-loss harvesting is a silver lining of a stock market decline.

Tax-loss harvesting is where you sell investments at a loss, replace them with a similar (but not identical) investment, and use the losses to offset capital gains, ordinary income, or possibly carryforward to offset future capital gains.

I like to think of tax-loss harvesting as creating a bank account of losses you can use in the current year, but also carry forward for as long as you are alive.

They can be very helpful in reducing the taxes you pay when you need to take withdrawals or rebalance inside a brokerage account.

For example, let’s say you create $100,000 worth of losses during a stock market decline. Remember, you bought a similar investment, so you still participated in any stock market recovery, but by recognizing the losses, you now have $100,000 worth of losses that can offset future capital gains.

Let’s say you don’t recognize any capital gains in the current year. You can offset up to $3,000 of ordinary income per year with the losses and carryforward $97,000 of losses. Let’s say the next year you need to rebalance because stocks have done really well and that will create $50,000 worth of capital gains.

Then, you can fully offset the $50,000 of capital gains and pay no additional capital gains taxes, offset $3,000 of ordinary income again, and carry forward $47,000 of losses to offset future capital gains or ordinary income (up to $3,000 per year).

Losses are particularly valuable for people who have concentrated stock positions they want to sell, but want to minimize the taxes they pay.

While nobody likes to see their portfolio go down, if you do nothing and wait for the stock market to recover, you miss out on the opportunity to recognize losses to offset future capital gains and defer taxes.

Final Thoughts – My Question for You

While stock market declines feel lousy, there are silver linings to them.

Normally, valuations on stocks become cheaper, which usually means future expected returns are higher. Remember, this shouldn’t be used for market timing, and it’s not a perfect relationship, but it can be good for setting expectations.

Also, a stock market decline usually doesn’t mean do nothing. You can do Roth conversions, rebalance, or tax-loss harvesting to potentially help reduce the taxes you pay over your lifetime and bring your portfolio back into alignment, which may help future returns.

I’ll leave you with one question to act on.

Which silver lining will you think of during the next stock market decline?