When a spouse passes away, taxes are usually the last thing on someone’s mind.

There is grief, family conversations, a funeral or celebration of life, temporarily being locked out of financial accounts, administrative hassle of settling accounts, and trying to imagine a changed life while missing their person.

If you have the capacity to think about taxes, there are a few key opportunities that exist only in the year of death, and once the window passes, they are gone. The key opportunities could mean tax savings of tens of thousands of dollars or more, depending on your financial situation.

Let’s go through what tax planning you should do in the year your spouse dies.

Roth Conversions

One key opportunity in the year of death is Roth conversions.

Although you need to complete the Required Minimum Distribution (RMD) first, once it’s complete, you may want to consider a Roth conversion.

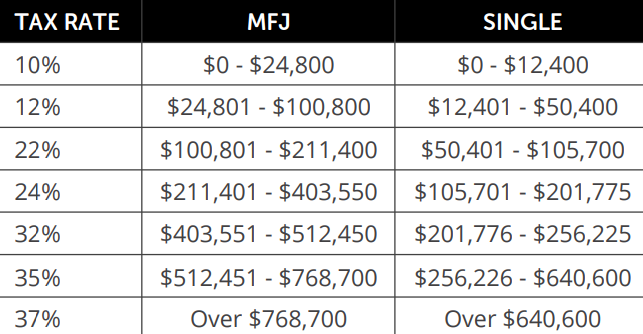

There is a term called “survivor’s penalty” or “widow’s penalty” after a spouse dies because a couple usually files as married filing jointly, and the year of death is the last year they can normally benefit from the wider tax brackets.

The year after death, the surviving spouse normally needs to file as single, where the brackets are not as wide, which often leads to higher taxes.

Planning Tip: There are cases where someone can file as a qualifying surviving spouse for two years after death, but there are special rules, such as having a child that qualifies as a dependent who lives with you and that you don’t remarry before the end of the current tax year.

The reason taxes usually go up for the surviving spouse is because the income is often similar, but the tax brackets are narrower. For example, RMDs, interest, dividends, rental income, and many other sources of income will be the same. The only main change is that the lower Social Security benefit will stop. If you had pensions, the pension amount may be reduced slightly, but my hope is that most couples chose the highest survivorship pension option, and there isn’t a reduction in income.

You can see in the tax brackets below that if your taxable income was $300,000 as married filing jointly, that would put you in the 24% tax bracket. If your spouse died and your income dropped $30,000, and you had to file as single, you’d be in the 35% tax bracket.

To put it in more concrete dollar terms, let’s look at an example.

Let’s assume Suzie and Gabe Sample have the following income:

- Interest: $20,000

- IRA Distributions: $150,000

- Pension: $70,000

- Social Security: $70,000

- Suzie: $40,000

- Gabe: $30,000

- Rental Income: $36,000

Their total income is $335,500. After a standard deduction of $35,500 in 2026, their taxable income is $300,000. Their estimated federal tax liability is $59,324.

If Gabe passes away and his Social Security amount goes away, the total income would be $310,000 (only up to 85% of Social Security benefits are taxable). After a $18,150 standard deduction in 2026 for single filers, taxable income would be $291,850.

At single tax rates, the estimated total federal tax liability is $73,045.

In other words, although Suzie’s income went down after Gabe passed away, she is paying about $13,721 more in taxes. Her ordinary income marginal tax bracket went from 24% to 35%.

If she lives another 10 years past Gabe, she may pay more than $100,000 more than originally thought if married filing jointly.

Since Suzie can only use the married filing jointly bracket in the year of Gabe’s death, she may want to consider a Roth conversion to fill up the 24% tax bracket. That may mean converting about $103,000 from her IRA to her Roth IRA.

If we assume she pays 24% on the $103,000 instead of 35%, that is a tax savings of more than $11,000.

She could even consider converting to the top of the 32% tax bracket because she feels confident she will be in the 35% tax bracket the following year.

Another benefit of a Roth conversion is that when Suzie passes away, the Roth IRA won’t be taxable to her adult kid when they start distributions from an Inherited Roth IRA, whereas the Inherited IRA distributions would be taxed as ordinary income.

If Suzie had $2,000,000 in an IRA, and her adult kid had to deplete the account within 10 years of her death, that’s more than $200,000 of ordinary income each year on top of her adult kid’s other sources of income. Although they don’t have to take distributions evenly over 10 years, trying to get $2,000,000 out of an IRA within 10 years is a lot of income in most years.

If the adult kid is working and earning $250,000 themselves, that’s $450,000 worth of income.

It’s easy to see a scenario where the adult kid could be in the 32% or 35% tax bracket, which means that Roth conversion in the 24% tax bracket is helpful not only to Suzie, but to her adult kid.

A Roth conversion in the year of death is often a good way to reduce the widow’s penalty in future years.

Step Up Cost Basis in Taxable Brokerage Accounts

Most financial institutions don’t automatically step up the cost basis of brokerage accounts when a spouse passes away. It usually falls on you to request it.

If you are in a Community Property state (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin) and the assets are in both spouses’ names, you should receive a 100% step up in cost basis. This means that if you bought Stock ABC for $10 a share decades ago, and it now is worth $300 a share as of the date of death, your new cost basis becomes $300.

If you were to sell the stock shortly after, the gain or loss should be minimal. For example, if you sold it a few weeks later when it was worth $305 a share, the new gain will be $5 a share.

When a spouse passes away, this is a good opportunity to diversify, simplify, and clean up investment portfolios. For example, you could do the following:

- Reduce concentrated stock holdings

- Sell mutual funds that are tax-inefficient and push out capital gain distributions

- Get out of funds with high expense ratios

- Reduce the number of investments

- Rebalance the portfolio

When investments have been held a long time, it’s hard to adjust the portfolio because any sales will usually result in capital gains and taxes. When a spouse passes away, particularly in a Community Property state, you can usually make any changes with zero to minimal tax consequences.

If you bought an individual stock that’s done really well and it’s now 20% to 30% of your portfolio, you may be able to sell it without significant tax consequences.

If a particular part of your portfolio is not as geographically diversified as you wanted it, such as owning too much in US stocks, you could sell some and buy more developed international or emerging markets.

If you have 30 different investment positions, you could reduce it down to 5 to 10 investments or fewer.

For those not in Community Property states, you are usually only eligible for a step up on 50% of the assets’ value, which means the original basis is unchanged for the surviving spouse. Although it’s not a full step up in cost basis, it still gives more flexibility to make changes.

For those in Common Law states, there are planning strategies to receive a full step up in cost basis, but they also have their disadvantages.

For example, if a married couple lives in a Common Law state with a joint account and one spouse is diagnosed with a terminal illness where they are expected to live more than a year, the healthy spouse could move their assets from the joint account to an account in the terminally ill spouses’ name.

If the terminally ill spouse lives more than a year and then passes away, the assets should receive a step up in cost basis when they go to the healthy spouse. The key is for at least one year to pass between the transfer of the assets and the death of the spouse. If it’s less than a year, the assets don’t receive a step up in cost basis.

The major risk with a strategy like this is that once the assets are gifted, the terminally ill spouse can do anything they want with them. They could give them to another family member, lose them to fraud or a scam, or donate them to charity. Many people think their spouse would never do such a thing, but it’s possible, particularly in the context of a terminal illness.

Adjust the Investments (Concentrated Stock, High Expense Funds, and Tax-Inefficient Funds)

When a spouse passes away and some or all of the cost basis gets a step up, it’s worth spending the time to think about modifying or completely changing the investments.

I touched on it before, but it’s important enough to have its own section.

What I often find is that many widows or widowers don’t want to immediately make changes to the investments, particularly if they were the spouse who was less involved with the investment decisions.

They may recall their spouse talking about how well they did with XYZ stock, why they don’t want to own international stocks, or how they like a particular mutual fund company.

Unfortunately, this can often lead to unbalanced, extremely risky portfolios if XYZ stock did really well. The worst portfolio I ever saw was a portfolio with one individual stock, and on top of it, they had a hefty margin loan on it. Imagine a spouse passing away and keeping it. Their entire financial future is tied to the success or failure of that stock.

If an individual stock makes up more than 5 to 10% of your investment portfolio, that’s a risk to your financial future.

Another issue I see is owning tax-inefficient funds and high expense ratio funds. This usually comes in the form of the statement, “We have owned that fund for forever. We bought it 30 years ago.”

If the tax consequences are minimal to make the change, and sometimes even if it’s not minimal, it can make sense to get out of high fee funds or funds that produce capital gain distributions each year. The cost of the taxes and the cost of the fund each year can sometimes have a break even of only a few years, meaning it can make more sense to sell the fund even with tax consequences, pay the tax today, and be in a better position after a few years.

For many widows and widowers, making investment changes after death is often the last thing on their mind, but it’s also often one of the best times to make changes with minimal tax consequences.

It’s a good time to review the time frame for using the funds and deciding whether the current investments are properly aligned for their different future.

Get An Appraisal on The Home

When your spouse passes away, it’s important to get an official appraisal on your home. You don’t want one done by a real estate agent or another unofficial method. You want to pay an appraiser to write up a report and have that as evidence of what your house is worth.

The reason for getting an official appraisal is that your house may also receive a step up in cost basis, either fully or partially, at death.

Unlike investments that trade regularly where you know the current valuation and can assign a cost basis, no one knows what your house is actually worth on the day of death unless you get an official appraisal.

The official appraisal is what can be used to assign a value in case you sell your home. For example, let’s say you bought a home for $100,000 over 30 years ago and it’s worth $800,000 when your spouse passes away.

If you live in a Community Property state like Washington, your new cost basis is $800,000 instead of $100,000. If you sell it for $900,000 five years later, you only have a $100,000 capital gain. Your $250,000 home sale tax exclusion more than covers your capital gain, meaning you can sell it without any tax consequences.

It’s much easier to get the official home appraisal shortly after your spouse passing away than trying to retroactively get an appraisal five years later (or decades).

Charitable Giving

Earlier I talked about how Roth conversions can be helpful in the year of death. Another strategy to layer in with Roth conversions, particularly if you are charitably combined, is to also do a larger charitable gift.

If you are over 70 ½, Qualified Charitable Distributions tend to be the most tax-efficient form of giving, but if you are younger, you could consider a larger gift of stock and/or a gift of stock to a Donor-Advised Fund. This would be particularly useful for any stock that does not receive a step up in cost basis at death.

If the donation is large enough (i.e. bunching many years worth of gifting into one year into a Donor-Advised Fund), it may allow you to itemize your deductions, which can allow you to convert more to a Roth IRA within the same tax bracket.

Final Thoughts – My Question for You

For many widows and widowers, tax planning in the year of death is hard to think about. There is enough going on as you face a changed reality.

If you can set aside the time, thinking about a Roth conversion, adjusting your investment portfolio, getting an appraisal on your home, and revisiting your charitable giving can be helpful.

I’ll leave you with one question to act on.

What tax planning will you do this year?