You have your homeowners insurance in place, but what about earthquake insurance?

Is earthquake insurance worth it?

Your typical homeowners insurance policy won’t cover damage due to an earthquake, which means if you suffer damage due to an earthquake, you may be required to pay everything out of pocket.

That could potentially mean footing the bill to rebuild your house if it falls off the foundation and collapses.

Earthquake insurance is a coverage many people go without. Is that a good decision?

Let’s talk about what earthquake insurance covers, how much it costs, earthquake hazards in different states, where you can buy it, and how to think about whether you want to buy earthquake insurance.

What is Earthquake Insurance and What Does it Cover?

Earthquake insurance may provide coverage for damage caused by earthquakes. It could provide funds for damage to your home, other structures on your property, a place to live temporarily while your home is being repaired, or to replace personal property.

Generally, homeowners insurance policies do not cover earthquake damage, which is why earthquake insurance can often be added to your homeowners policy or bought through a separate policy.

Earthquake insurance may cover:

- Dwelling

- Other Structures

- Personal Property

- Loss of Use/Additional Living Expenses

Dwelling

Similar to homeowners insurance, earthquake insurance may cover the cost of repairing or rebuilding your home. This could help repair the foundation, garage, or anything else attached to the home.

Often, brick or stone masonry are excluded from earthquake insurance policies because they are more likely to be damaged in an earthquake.

Other Structures

This may cover other structures that are detached from your home. Typically, if it’s connected to your house’s roof line, it falls under dwelling coverage. If it is not attached to your house’s roof line, it falls under other structures.

For example, other structures coverage may pay to repair or replace detached garages, gazebos, or fences.

Personal Property

If your personal possessions are damaged in an earthquake, earthquake insurance may help replace them. It could include items like your bed, kitchen table, clothes, jewelry, musical instruments, and more.

Loss of Use/Additional Living Expenses

If your home is uninhabitable after an earthquake, loss of use or additional living expenses coverage may help cover the cost of living elsewhere while your home is repaired. It could also pay for increased transportation or food costs.

What Does Earthquake Insurance Cost?

Earthquake insurance is expensive.

In a lower risk state, it might only be $100 to $300 a year, but in states that are more likely to experience an earthquake, you might pay $800 to $3,000 annually.

In my experience, I see most people in higher risk areas pay $1,000 to $2,000 annually.

The cost is going to be based on many different factors, such as:

- Where you live

- Your home’s building materials

- Age of your home

- Home value

For example, if you live in California or Washington state, those areas experience more earthquakes, which means you would normally pay more than someone living in Wisconsin.

If your home uses more expensive building materials, those are more expensive to repair, which means your premiums may be higher for earthquake insurance.

Older homes may not be built up to the same standards today. Some people choose to retrofit their homes, such as bolting their home to the foundation, to make them safer in an earthquake.

Some insurance companies won’t offer earthquake insurance if your home is not bolted to the foundation, which means you may have limited coverage options if you have an older home that is not retrofitted. If you have an older home and are able to get coverage, the home may be built in such a way that it is less likely to survive an earthquake, which could drive up your earthquake insurance costs.

Your home’s value also influences the earthquake insurance premium. If you have a $300,000 home, that is much cheaper to replace than a $1,000,000 home.

The only way to know your exact cost is to contact an insurance agent or broker who has access to earthquake insurance and can provide a quote, but you may see premiums between $1,000 and $2,000 in higher risk areas.

The other frustrating part about earthquake insurance is that the deductibles tend to be high, often 10% to 20%.

This means that if you had dwelling coverage of $500,000 and a deductible of 10%, you would be on the hook for $50,000 before your earthquake insurance would pay.

In many cases, an earthquake may only do $20,000 to $50,000 in damage, which means you would not want to file a claim because it’s below the deductible amount.

In these situations, earthquake insurance is protecting the very worst possible scenarios where your home slides off the foundations and is crushed beyond repair.

For many people, it’s tough paying over $1,000 annually knowing you still might need to pay $50,000 to $100,000 (or more, depending on the insured home value) as a deductible before your insurance company pays.

However, $50,000 is still a better price to pay than $500,000 if you have to rebuild your home.

Earthquake insurance is expensive and with high deductibles, you will still usually be responsible for paying a significant amount before your earthquake insurance provides benefits.

Which States Have the Highest Earthquake Hazards?

It’s impossible to know when and where an earthquake will hit.

Growing up in the Pacific Northwest, we were always told to expect an earthquake in our lifetime because scientists estimate a major quake happens once every few hundred years and the last one happened more than 300 years ago.

California is also very familiar with earthquakes.

But, where are the largest hazards?

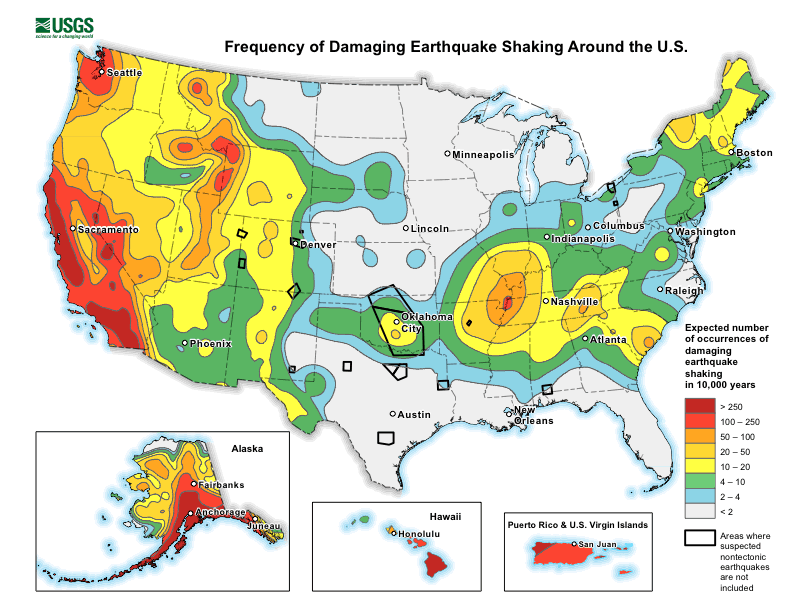

Thankfully, the USGS created a hazard map showing the frequency of damaging earthquake shaking around the U.S.

As you can see, the largest hazards are in and around Seattle and large parts of California, though there are hazards in most of the West, as well as some of the southern states and parts of the northeast.

USGA estimates that nearly half of Americans are exposed to potentially damaging earthquakes.

The states with the highest populations exposed are:

- California

- Washington

- Utah

- Tennessee

- Oregon

- South Carolina

- Nevada

- Arkansas

- Missouri

- Illinois

What’s interesting about this map is that the black outlines show where the number of occurrences of damaging shaking could go up because of induced earthquakes, which are caused by human activity. Human activity may include activities such as fracking.

As you can see, particularly in areas of Texas, there is not a high hazard of natural earthquakes, but there are more induced earthquakes.

This map can help you understand the earthquake hazard in your area, but it won’t tell you the particular risk you face or whether earthquake insurance is worth it.

Do I Need Earthquake Insurance?

Now that you know what earthquake insurance may cover, the cost, and which states have the highest earthquake hazard, let’s answer whether you need earthquake insurance.

As with most personal finance decisions, it depends!

According to the USGS, you should consider the following factors:

- How close you are to active earthquake faults

- Frequency of earthquakes in your region

- Time since the last earthquake

- Building construction

- Architectural layout

- Materials used in your home

- Qualify of the build

- Type and condition of your soil

- Slope of your land

- FIll material

- Geologic structure of the earth beneath your land

- Annual rainfall

- Value of your home and personal possessions

- Cost of the insurance and deductible

Those are great aspects to consider, and I’ll add to it with a few questions to consider.

- Am I using the equity in my house during my retirement?

- If I needed to rebuild my house using my own assets, would that radically alter my financial independence plan?

If you plan to sell your home, downsize, and invest some of the proceeds or use equity from your home in other ways during retirement, I think it’s reasonable to consider earthquake insurance.

For example, if your financial independence plan relies on $500,000 in proceeds from selling your home to fund your living expenses at some point in retirement, what if that money is not available because an earthquake destroys your home?

Wouldn’t it make sense to protect that future retirement income through earthquake insurance?

I can’t say for certain it makes sense, but it’s something to consider.

Another way to approach it is if you could easily rebuild your home without changing your retirement, then maybe earthquake insurance isn’t needed.

However, if you had to spend a good chunk of your retirement portfolio to get back into a home after an earthquake and that affected how much you could spend later, it may make sense to pay earthquake insurance premiums for the extra protection.

In short, if your home is a big asset in your financial plan and you couldn’t easily afford replacing it, earthquake insurance is worth considering.

Where Can I Buy Earthquake Insurance?

I recommend contacting your current insurance agent or broker to ask if your current company can provide a quote for earthquake insurance.

If you are considering earthquake insurance, it’s also a reasonable time to shop around and compare rates for your homeowners, auto, and umbrella insurance coverage.

If you can’t find an insurance company that will provide earthquake insurance, you may be able to find a standalone policy.

For example, GeoVera and Arrowhead may offer a standalone earthquake insurance policies in California, Oregon, and Washington.

California residents also have the option of buying a California Earthquake Authority (CEA) policy through their existing homeowners policy. They can even estimate the costs of an earthquake insurance policy online.

Not every insurance company sells earthquake insurance, which means if you want it, you may need to do more research.

Final Thoughts – My Question for You

Deciding to buy earthquake insurance is a personal decision.

For some people, it is a worthwhile expense. For others, they see it as a waste of money.

There is no “right” decision when it comes down to whether earthquake insurance is worth it.

If you are wondering whether I have earthquake insurance, I do. I own a home in Seattle on a steep hill. Although coverage isn’t cheap, I get peace of mind knowing that if I need to completely rebuild my house or live somewhere else, I have coverage, even if it requires a huge deductible.

I also think about how if I am living in Seattle, it will likely be challenging to find accommodations after an earthquake and if I can find them, the cost will likely be drastically inflated. That’s when the loss of use could be worth a considerable amount, in addition to the funds provided for rebuilding the house.

As with every personal finance decision, you need to weigh the risks and decide whether earthquake insurance is worth it in your situation.

I’ll leave you with one question to act on.

Will you get a quote for earthquake insurance?