Dividend investing is one of the most misunderstood parts of investing.

As a financial planner, I’ve been in many meetings with prospective families who have different levels of investment education. I often find people think dividend investing is magic and must be the end-all, be-all of investing.

Unfortunately, many of the closely held beliefs people have about dividend investing are wrong. The internet is buzzing with articles about how to find dividend paying stocks, which can create a desire to live off dividends instead of selling parts of your portfolio.

Before I get into the issues with dividend investing, what do I mean when I say dividend investing?

Dividend investing is investing in companies that pay cash distributions. It’s a return of profits to people who hold the stock.

Now, let me dispel some of the myths of dividend investing and seven problems with dividend investing.

Problem 1: Dividends Increase Your Taxes

The first problem with dividend investing is that it increases your taxes in a brokerage account.

The taxes are usually not an issue in a tax-advantaged account, such as an IRA, Roth IRA, or 401(k), but in a brokerage account, dividends can increase your taxes.

When a dividend is paid, you are taxed on it, whether you reinvest the dividend or take it as cash. It doesn’t matter whether you leave it in the brokerage account or take it out. It will be taxed.

How it is taxed depends on whether it is qualified or nonqualified.

Qualified dividends are taxed at preferential capital gains tax rates. Nonqualified dividends are taxed at ordinary income tax rates.

Capital gains tax rates are 0%, 15%, or 20%, depending on your other income and which bracket you fall into. Ordinary income tax rates range between 0% and 37%.

In order for a dividend to be qualified, it must:

- Be issued by publicly traded US companies

- An investor must own the stock for more than 60 days out of a 121-day period beginning 60 days before the ex-dividend date

The last bullet is complicated, but a general way to think about it is if you have held the stock for a few months, the dividend will likely be qualified.

Certain funds usually do not pay qualified dividends, such as REITs, MLPs, and bond funds. They normally pay nonqualified dividends that are taxed at ordinary income rates.

Now that you know more about how dividends are taxed, let’s look at an example.

Let’s say you are in the 15% capital gains bracket and earn $10,000 worth of qualified dividends in a brokerage account.

Whether you reinvest the $10,000 worth of dividends back into the stock, take the $10,000 as cash and leave it in the account, or distribute the $10,000 to your bank account, you will be taxed on the dividends.

Your tax bill for those dividends will be approximately $1,500.

Now, you may be thinking, “Who cares? I don’t mind paying taxes. At least I am getting dividends.”

I’ll address that in the next two sections.

Problem 2: Dividends Are Forced Taxation

Would you rather pay 15% in taxes on the growth in your portfolio in the year that you earn it or when you choose to pay it?

I know my answer.

I want to choose when to pay it!

Dividends are forced taxation.

If you have a higher income year and want to reduce your tax liability, you can’t. You can’t control when you receive the dividends, which means you can’t control when you are taxed on the dividends.

Who wants to be forced to pay taxes? One of the biggest pain points for people in retirement is taxes. Most people want to know how to reduce their taxes and make sure they are doing everything possible to pay what they are legally obligated, but not tip the IRS.

Dividend investors are better tippers to the IRS.

With careful planning, you can better control your tax situation. If you can reduce your income, that may allow opportunities for Roth conversions to reduce taxes over your lifetime. I’m not a fan of dividend investing because it’s forced taxation that doesn’t allow you as much flexibility with how you control your income.

I’d much rather control when I am taxed. What do you prefer?

Now, you may still be thinking, “Okay, I’m taxed on what I am earning. That’s okay. It’s free money. As long as I keep earning it, I can support my lifestyle.”

Let’s talk about that myth.

Problem 3: Dividends Are Not Free Money – Yield vs. Return

Dividends are not free money. They don’t magically come out of thin air. As the old adage goes, “There is no such thing as a free lunch.”

Let’s look at a simple example.

If Company A is worth $100, has no debt, and pays a $5 dividend, how much will it be worth after it pays the dividend?

The answer is $95.

After the company pays $5, it has $5 less on its balance sheet. It can’t pay the $5 dividend and still be worth $100.

If it could, that would be like me giving you $5 out of the $100 in my wallet and still thinking I have $100 in my wallet.

The reason people get confused about dividends not being free money is that stock prices move constantly while the stock market is open. It’s harder to see on the day that a company pays a dividend that it is declining in price by the same value because other forces are at play.

If really positive news comes out on the day the company pays a dividend, it may go up by a similar amount. For example, if Company A announces they have a new partnership in the works that will be positive for the company, they may go up in value by $5 on the same day they pay a $5 dividend.

If you just looked at the stock on that day, you might think that you have the same company worth $100, but you also received $5 as a dividend. It actually looks like the dividend was magically paid.

But, that’s not what happened. If the dividend hadn’t been paid, the stock likely would have been worth $105 ($100 + $5 increase in price).

In either case, you have $105.

If the company pays a dividend, you have the $5 dividend plus the $100 in a share of Company A. If the company doesn’t pay a dividend, you have the $105 in a share of Company A.

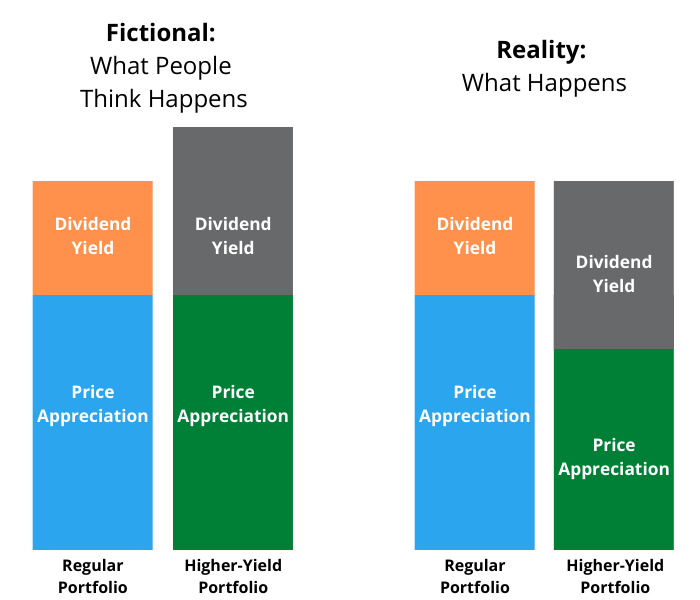

This brings me to my next point – dividend yields do not equal return.

People often confuse dividend yields and return or price appreciation.

Remember how I said you can better control how you are taxed if you don’t focus on dividends?

You can better control how you are taxed by focusing on price appreciation.

Price appreciation is the key here.

When a stock goes up in a brokerage account, you are not taxed on it. If a stock goes up $10,000 in a brokerage account, you are not taxed on the $10,000 until you sell.

I know that seems basic, but let’s break it down further.

People should care most about their total return, which are the dividends plus price appreciation.

Total return = Dividend + Price Appreciation

For example, if Company A pays a 4% dividend and appreciates 6%, they have a 10% total return.

To make the numbers more concrete, let’s say Company A is worth $100 again. Company A paid you $4 in dividends and appreciated $6 in the first year.

How much is taxed?

As you learned earlier, $4 will be taxed at capital gains rates, assuming it is a qualified dividend. If you are in the 15% capital gains bracket, you will pay $0.60 in taxes.

The $6 you earned from price appreciation won’t be taxed.

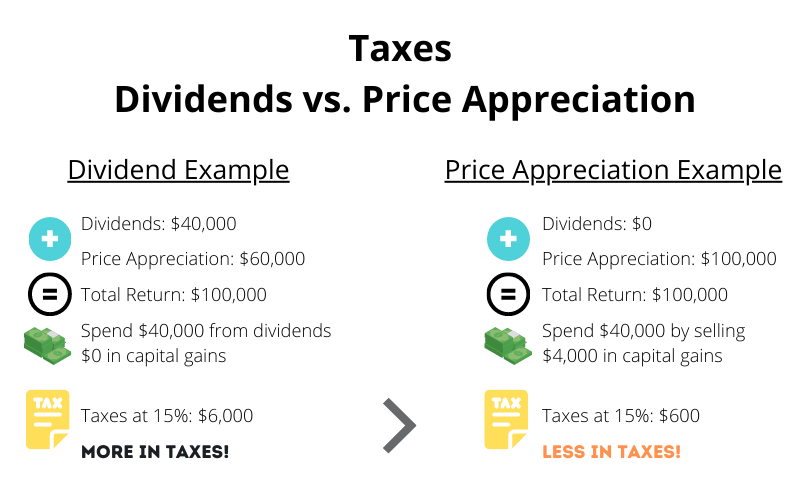

It doesn’t sound bad with smaller numbers, but let’s do this on a portfolio level now. Let’s assume you have $1,000,000 in a brokerage account and earn 4% in dividends and 6% in price appreciation.

Now, you have $40,000 in dividends, leading to a tax bill of $6,000. The other $60,000 earned through price appreciation is not taxed.

It feels worse now, right?

What if, instead of earning dividends, you earned 10% through price appreciation?

Then, you don’t receive any dividends and get to choose when you recognize the $100,000 gain.

If you are trying to create lower levels of income, perhaps you only sell $40,000 and recognize $4,000 in capital gains.

In that situation, $4,000 in capital gains will be taxed at 15%, meaning you owe $600 in taxes.

Instead of paying $6,000 in forced taxes through dividends, you cut your portfolio tax bill to $600 in taxes through focusing on price appreciation.

I’d much rather receive the majority of my return in the form of price appreciation – not dividends.

Dividends don’t magically increase your return or make your income safer. They aren’t free money, but they are forced taxation.

A better way to invest is to focus on total return. Price appreciation allows more flexibility in how you recognize income and can be used to plan your income year-to-year for tax planning purposes.

Problem 4: Dividend Stocks Are Not a Bond Substitute

No matter how many times you read it online, it doesn’t make it any more true. Dividend stocks are not a bond substitute.

Bonds are typically used for income and to reduce the ups and downs of the portfolio. They are not meant to be drivers of growth.

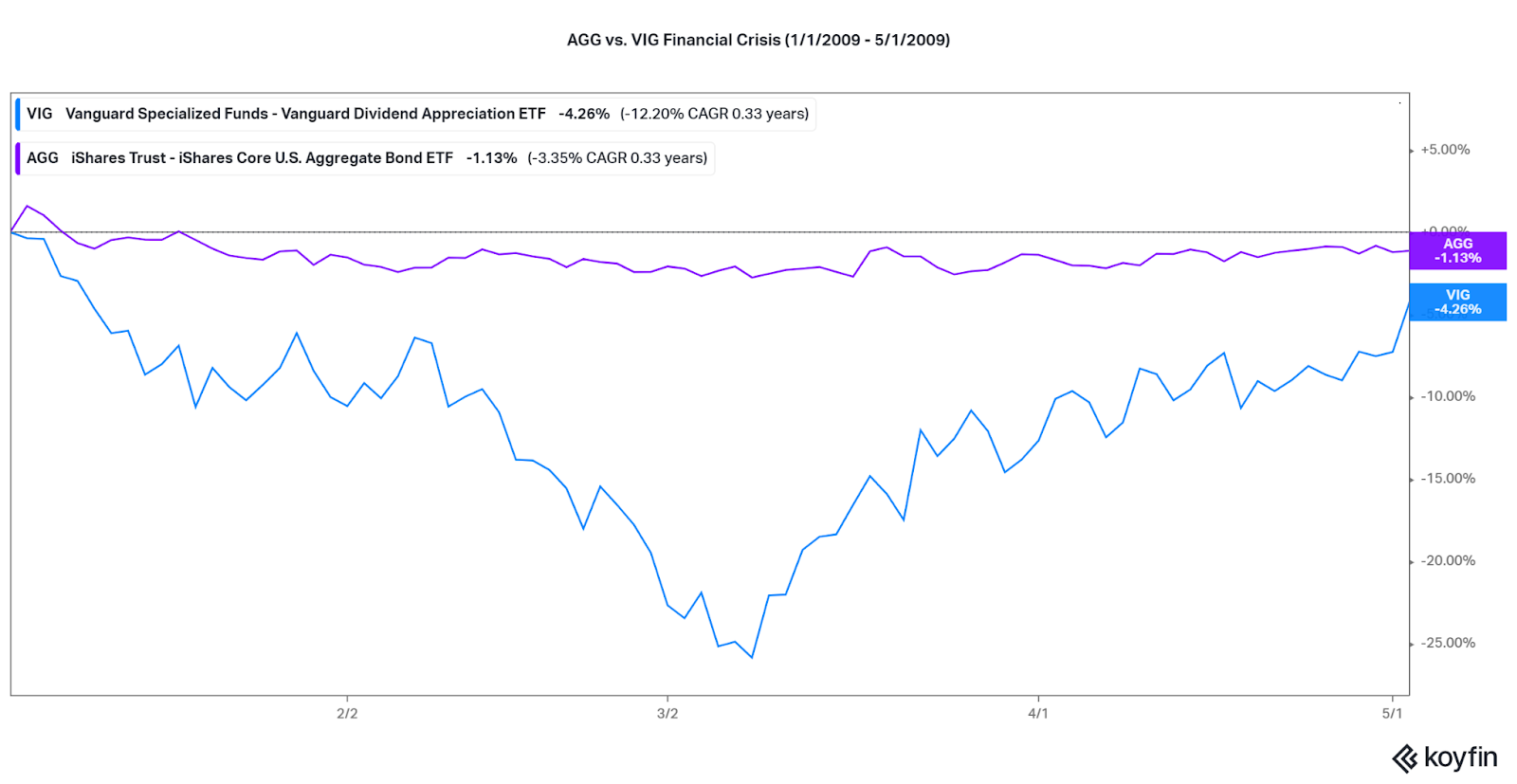

To put it in perspective, let’s look at how one dividend ETF, the Vanguard Dividend Appreciation ETF (ticker: VIG), performed compared to an aggregate bond ETF, iShares Core U.S. Aggregate Bond ETF (ticker: AGG), during market turmoil. This isn’t a recommendation for either ETF. I am using them to show that bonds normally don’t decline in value as much as stocks during stock market declines.

The first graph shows the decline of each during the start of the COVID pandemic. You can see in March of 2020 that bonds declined in value, but nowhere near as much as the dividend ETF.

The bonds declined a little more than 5%. The dividend stocks declined about 25%+. Those are two very different experiences for investors.

If you had $1,000,000 invested in each, you would have about $950,000 invested in bonds and about $750,000 invested in the dividends stocks near the lows.

The second graph shows the performance of the same ETFs during the Financial Crisis in 2009. Bonds primarily held their value during that time while the dividend stocks declined considerably.

If an investor wants to take more stock risk and is comfortable with the ups and downs, that is okay, but dividend stocks are not a substitute for bonds. I’d go back to my earlier point that if an investor wants to take more stock risk, why not invest it in a way that focuses on price appreciation?

That way you get to control how you are taxed.

Problem 5: Dividends Reduce What The Company Can Reinvest for Growth

Another reason I don’t like focusing on dividend investing is that companies that pay dividends have less money to reinvest for growth.

They are admitting that they don’t have ideas to increase the value of the company, which usually means they are done growing as fast.

Another way to look at it is that they are saying, “We don’t have a responsible way to use this money and it would be better in your hands.” Then, you become responsible for deciding what to do with that income – whether it’s investing it or spending it.

Since dividend companies tend to be more mature, their better days are usually behind them, and this shows up in performance.

For example, below is a chart of the same dividend ETF compared to an S&P 500 ETF (ticker: SPY). As you can see, performance has been lower for the dividend paying stocks than the ETF that tracks the S&P 500.

I’d much rather invest in companies that are reinvesting profits, being innovative, and have more potential for price appreciation.

Problem 6: Focusing Only On Dividend Stocks Reduces Diversification

Another often forgotten aspect of focusing on dividend stocks is that you are excluding a whole universe of stocks!

In fact, FINRA reported that in 2015 that about 84% of the companies in the S&P 500 index pay dividends. In the Standard & Poor’s mid-cap index, it was about 70.5%. For the Standard & Poor’s small-cap index, only about 54% were paying dividends.

Let’s look at an example as of April 2022.

If I screen for domestic companies trading on the NYSE or NASDAQ using Charles Schwab’s stock screener, there are 4,548 companies available.

If I screen for companies that don’t pay a dividend, there are 2,826 companies available.

That means there are about 62% of companies that don’t pay dividends.

Can you imagine only focusing on about 38% of the investable stocks?

If you are only focusing on dividend investing, you are leaving out many companies. Plus, you are likely leaving out stocks from certain segments of the market.

For example, you likely would have less of an exposure to small cap stocks. As noted earlier, only 54% of small cap stocks were paying dividends in 2015. When I do the screening today, it’s about 52% – not much has changed. Historically, small cap stocks have performed better than large cap stocks over longer periods of time.

Focusing exclusively on dividend stocks means you are not as diversified as you could be.

Problem 7: Dividends Are Not Guaranteed

Lastly, and perhaps most importantly, dividends are not guaranteed.

People talk about dividend stocks as if they are guaranteed to go on for forever, but there are many examples of stocks cutting their dividends and even going bankrupt.

Oftentimes, dividends are cut or reduced with no notice. Worse, the stock price can drop, sometimes significantly, at the same time dividends are cut or reduced.

There are many stocks people thought were “safe bets” because they had been paying a dividend for a long time or consistently made money. With hindsight, it’s easy to say, “Of course, I wouldn’t invest in that type of stock. I’d sell it before things got bad.”

That’s what many people think, but yet, that’s not what happens.

You can ask investors in General Motors. They paid a dividend for several decades up until 2006 when they reduced their dividend and then in 2009 declared bankruptcy.

What about Washington Mutual? It was a huge financial institution with a growing dividend until they declared bankruptcy in 2008. People lost a lifetime of savings.

You also have BP. It looked solid as a dividend paying company until the Deepwater Horizon oil spill. The stock dropped considerably, and the company suspended their dividend for over half a year.

People normally will say this won’t happen to them – that they have a solid company. Yet, who can control what happens in the world?

Who can control how consumer habits change, whether someone commits fraud, or how the world will respond to a crisis?

Dividends are not guaranteed. It’s not a regular income stream you can count on.

Final Thoughts – My Question for You

Dividend investing has been popular for a long time, but it seems to come in and out of favor depending on what is happening in the world.

I’m not a fan of dividend investing.

Not only do dividends increase your taxes, but they are a forced taxation. As a financial planner, I prefer investing in a way that allows for more tax planning.

Dividends are certainly not free money. Your total return is what you should care most about, and I prefer most of my return to come from price appreciation – not dividends.

Although people may claim you can hold dividend stocks as a bond substitute, you now know the risk is not the same.

When a company pays a dividend, they are admitting they don’t have good ideas to grow your money. Over time, we’ve seen that dividend stocks as a whole have worse performance.

Lastly, dividends are not guaranteed. Don’t let anyone tell you otherwise.

I’ll leave you with one question to act on.

Which problem with dividend investing will you remember the next time you read an article about the benefits of dividend investing?