Look, I’m not a fan of budgeting.

This isn’t an article about why you should budget, how to deprive yourself of everyday comforts, or the need to scrutinize your spending line-by-line.

However, I do think it’s important to review your spending every once in a while. It’s easy to start spending on something, leave it on autopilot, and never revisit whether it’s actually worth it.

Plus, knowing when and how your money is being spent can give peace of mind. If you know where it is going, it’s easy to see where adjustments can be made if you ever felt the need to alter your spending.

Let’s look at the best app to track spending. I’ll also talk about a few other ways you can track your spending because different methods work better for different people.

Why You Should Track Your Spending

Before I tell you the best app to track spending or how to track your spending, I want to tell you why you should track your spending. It’s hard to start something if you don’t know why it is important.

You should track your spending for the same reason you track what ingredients go into a recipe. You don’t have to measure each teaspoon, but you should at least know vaguely what is going into the dish and how much of it.

If you don’t know what’s going into the dish, you don’t know how to create it again in the future, how to adjust it to make it better, or what to cut back on if one flavor overwhelms the dish.

If you don’t know how your money is being spent, you have no idea if that’s actually how you want to be spending. Or, if your financial situation changes, either positively or negatively, you won’t have a baseline to know what you want to change.

For example, if you are unsure how much you spend per month and where it is going, what happens if there is a prolonged decline in the stock market? You may feel the need to reduce your spending, but by how much? In which areas of your life will you reduce spending?

If you know approximately how much you spend per month and what you are buying, it’s much easier to make adjustments.

It’s also easy to make adjustments the other way. I’ve met people who wanted to spend a certain amount giving to charity each year and after reviewing their budget, they could see they were falling very short.

Having a clear picture of how they were spending, it was easy for them to increase their charitable giving each year.

Tracking your spending doesn’t need to be an arduous task. In fact, once you set it up, it could require less than 10 minutes per month.

Isn’t 10 minutes per month worth knowing how much you are spending and where it is going?

Let’s look at the different apps and ways to track your spending.

Old Fashioned: Pen and Paper

I’ll be honest – I’m not a fan of this method, but I’m including it because I know some people need the tangibility of pen and paper.

You can write down every expense and how much you spend on a piece of paper to track your spending.

It’s easy to see why I’m not a fan of the pen and paper method. It’s painstakingly slow and cumbersome; however, for some, the act of writing it down makes it more real.

There have been studies that it is easier to spot errors when reading a hard copy than editing online. I imagine the same process is at play when budgeting.

With a computer screen, you might skim over certain sections, whereas on paper, you are forced to look at it more closely.

This is a decent method if you want to track your spending every few years, but I wouldn’t make this a regular habit, unless the other methods really don’t work for you.

Excel or Google Sheets

There are great free budgeting spreadsheets in Excel and Google Sheets.

This is the pen and paper method on the computer. It’s still time consuming, but it’s a good exercise to go through every five years or during big life changes.

Like the pen and paper method, there is something different about manually inputting expenses into categories compared to letting a software program do it for you. And, this is coming from someone who loves simplicity and automating finances as much as possible.

The times I’ve done my budget inside of Excel or Google Sheets, I’ve always looked at it more critically. The painful act of sitting down for an hour, reviewing bills and credit card statements, and typing it up makes me feel the budget more.

I also like this one because if you save the spreadsheet, you have snapshots in time to review in the future. It’s easy to see how your spending has changed over time.

For someone who hasn’t looked at how they have been spending for years, I usually recommend doing it in Excel or a Google Sheet because it’s more hands on.

I’ve found they get a better feel for how they are spending, and it forces them to look carefully at every expense. Looking at every expense, they automatically feel whether their spending is alignment with their values and where they may want to make changes.

YNAB

Like the pen and paper method, I don’t personally like YNAB and found it hard to use, but I know people swear by it, which is why I am including it.

YNAB uses a “zero-based budgeting system”, which is a fancy way of saying every dollar is assigned a “job.” In other words, there is no catch all or “other” category, and it’s not looking in the past.

Instead, you have to assign each dollar its job in advance. As soon as money comes into your bank account, you tell YNAB how much money should go to each category. For example, if $7,000 came into your bank account, you might tell it that $2,500 goes towards housing, $500 goes to charity, $1,000 to food, and $1,000 to a 529 plan, and $2,000 towards a future vacation.

Most apps that track your spending are backwards looking, meaning once the expense occurs, it is categorized, and you can see how you have been spending.

YNAB takes a more active approach and wants you to get hands on with allocating your money into different categories.

This method works really well for people who may be new to budgeting, have a tendency to overspend, or need a more hands on approach at first.

You can try it free for 34 days to decide if this method works for you. That should be enough time to decide whether you want to subscribe to the annual plan ($98.99 a year).

If it doesn’t work, you can try a different method.

Mint

Mint is my favorite app to track spending. I’ve been using it since 2014, and it’s free (i.e. you will see ads). Mint is owned by Intuit, the same company that owns QuickBooks and TurboTax.

I really like Mint because once you sync your bank accounts and credit cards, the transactions automatically flow into the system. If you don’t need to break down your spending by categories and simply want to see how much you are spending per month and how it changes over time, you have it.

It might only take 15-30 minutes to set up your accounts in Mint’s system.

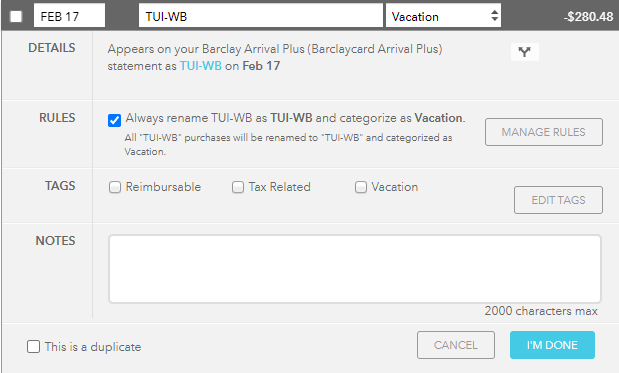

If you want better detail on how you’re spending by category, you may need to spend more time initially to fix it. At first, you may find that certain spending transactions are not categorized properly, but you can set up rules to automatically classify the spending to the right category. Once you set up a rule to classify it correctly, the system will see it in the future and categorize it how you set it. Below is an example.

This is why it may be more work in the first few months. You might need to spend 15-30 minutes at the end of each month looking through your transactions and categorizing any that are miscategorized. After a few months, most of your spending should be categorized correctly. You may only need to check it every few months from that point forward.

For example, when I recently logged in, I saw that an excursion we did while on vacation recently was categorized as “restaurants” because the company operator had a name that didn’t tell the system how to categorize it and not many other people have had a similar expense.

For common expenses with well-known businesses, the system usually classifies it correctly. It’s the smaller independent businesses or spending abroad that are usually not classified correctly.

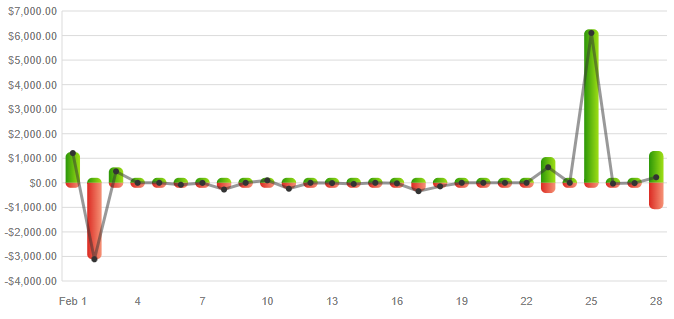

I also like Mint because you can easily see how your spending changes over time. You can view the last seven days, last year, all time, or many other time periods.

On top of seeing your spending, you can see your expenses, as well as your net income. It gives you a good sense for how much money is coming in, how much is going out, and how much is being saved. Below is a sample chart showing income in green and expenses in red.

Another benefit is that it can track your net worth over time. Tracking your net worth is a useful exercise because it gives you an idea of how much your money is growing or declining, particularly during market declines to help put things in perspective.

While you can track your net worth on a spreadsheet, I like that it’s automated on Mint. Like everything else, once you sync your accounts, type in other assets, and input your debts, the system automatically updates.

You then have access to your spending, income, assets, debts, and net worth for any historical point in time. It makes it really easy to see how things have changed, see where money is going, and make adjustments if your financial situation changes.

Those are my favorite features, but it also has a goals section. If you want to pay for your child’s education through saving in a 529 plan, you can set it as a goal and track your progress. It’s a way to visually see your progress.

Another feature other users like is the budgets section. If you want to input your goals and budget for certain categories, you can track how much you have leftover.

Mint is a very robust tool. Once you sync your accounts, most of it works on autopilot with a little maintenance each month.

Final Thoughts – My Question for You

There are many different apps to track your spending.

Personally, I’ve used Mint for a very long time and really like it. It is not the best fit for everybody.

You may need to try a few different methods before you find the one that works best for you. Some people love YNAB while others prefer Mint. Perhaps you need to try a spreadsheet or pen and paper.

Whichever method you decide, I recommend tracking your expenses at least every few years. With the automated systems, you can review it any time.

As life changes, you will know where your money is going. If adjustments need to be made, it’s much easier to do it if you have already been tracking your spending.

I’ll leave you with one question to act on.

Which method of tracking your spending works best for you?