Does it ever feel like your money is disconnected from your ideal life and what you value?

In my experience, our money is often put on autopilot, which can be a good thing to a certain extent, but if you never come back to what your money can do for you, you may be missing out on opportunities to live a more fulfilling life.

Life planning connects the emotional, human side of money to the technical, economic side. It goes beyond the “technically correct financial planning decision” and looks at who you are as an individual, what you value, and helps you come to the right financial planning decisions for you.

Life planning is about discovering what’s important to you, how you want to live your ideal life, identifying the obstacles that could possibly get in the way, creating the energy to live it, and aligning your money with it.

If your money isn’t helping you live your ideal life, what is it doing?

What is Financial Life Planning?

Financial life planning, often referred to as simply “life planning” focuses on the human side of financial planning.

Instead of starting with the numbers, it leads with you as an individual.

It explores what is important to you from a 50,000 foot view, narrows it down to the most essential elements, and identifies obstacles that could possibly get in the way of you living your ideal life.

It’s about creating the energy to live a truly fulfilled life while connecting your money to help you live it.

What are the Benefits of Financial Life Planning?

The benefits of financial life planning can be far-reaching.

You are reading this blog post because of life planning. When I went through my own life planning with a friend as we were learning the process, life planning gave me the permission I needed to take a leap of faith, leave my stable job, and start my own business. My business exists thanks, in part, to life planning.

The benefits of life planning don’t have to be huge, life-altering changes. They can be small, meaningful changes.

It’s about aligning your money with your ideal life. It’s giving your money a purpose and feeling good about how you are spending your time. It’s removing the autopilot of life and seriously looking at your life, reflecting, and dreaming about what you want it to be.

Here are a few possible examples of benefits from life planning:

- Feeling like your money is aligned with how you want to spend

- Taking regular vacations to decompress from life

- Making dinner with family a priority

- Hiring a babysitter regularly to make time for date nights or naps

- Hiring a house cleaner to free up time and have a clean space

- Building a workshop to learn woodworking

- Quitting a toxic job that is getting the best of you

As you can see, the benefits of life planning are different for everyone. Sometimes, it leads to small changes. Other times, it leads to uprooting a life and doing drastically different things.

Examples of Life Planning Outcomes

Life planning can feel intangible and may come off as a little too “touchy feely” for some people, but it’s not. It’s about making the space to get what you want from life.

It can help to hear what other people experienced to know what is possible with life planning

Personally, life planning helped me discover the courage to quit a stable, high-paying job I had been at for over a decade, take more than a 100% pay cut (start up expenses and no revenue coming in at first), and launch my own financial planning practice. I was burned out, and after years of asking for more administrative support, I was not provided it. So, I created a career that would be more sustainable for me.

I’ve known others who had been thinking of hiring a house cleaner for over a decade, but weren’t sure which step to take first and felt uncomfortable spending the money. After we looked at the financial aspects of hiring a house cleaner, they started identifying the next smallest step to finding a house cleaner. Now, they have a house cleaner who comes regularly. It’s been a positive addition to their life.

Another person found that with two young children at home, they had less time for themselves and each other. They identified that a babysitter once a week to go out to eat would be a welcome change. They weren’t sure where to start with finding a babysitter, so I asked them questions to help guide them to their own answers. They hired a babysitter and made “dinner without kids” a regular part of their week.

Life planning can be big or small changes. The size of the change does not matter. It’s the impact and meaningfulness of the change that matters.

Note: The above case studies are hypothetical and do not involve an actual Kindness Financial Planning client. No portion of the content should be construed by a client or prospective client as a guarantee that they will experience the same or certain level of results or satisfaction if Kindness Financial Planning is engaged to provide investment and financial planning services.

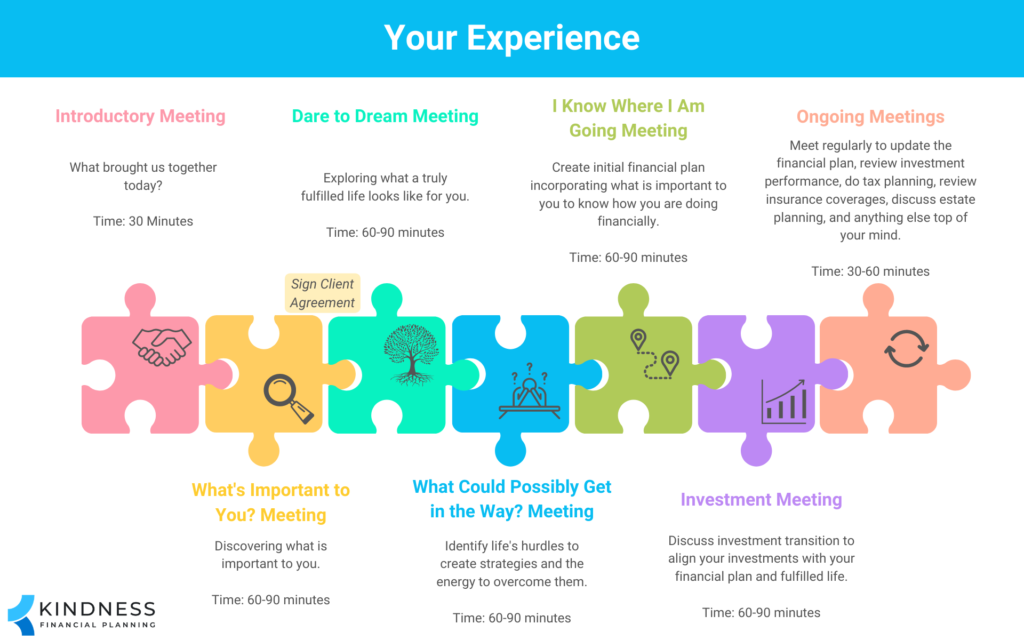

What is the Process of Financial Life Planning?

The process of financial life planning involves five conversations. The first three are probably not like anything you’ve experienced. Conversations four and five are more “traditional” financial planning conversations.

For some, it may feel like these conversations have nothing to do with money, but they have everything to do with money.

If you don’t make the time to discover and think carefully about what an ideal life looks like, how will you know if you are on the right path? How will you know how much money you need for it? How will you know if the money is aligned with your fulfilled life?

It’s much easier to make financial decisions when you know what you want from life.

Are you unsure if you should give money to family or friends? Life planning may help you discover whether that is a priority.

Are you tempted to move to another state to reduce taxes? Yes, life planning could help with that decision.

Do you feel like you are taking too much or too little risk with your investments? Again, once you know what your ideal life looks like, it becomes easy to see the answer.

Life planning is figuring out what is important to you and giving you the energy to go out and create that life — then integrating financial planning and investments into supporting it.

Imagine trying to do a jigsaw puzzle without seeing the picture on the box. Life planning is about creating the picture on the box before we decide how to put the pieces together.

What’s Important to You? – Conversation #1

The first conversation is about learning what brings us together.

It raises the question about what you want to accomplish together. It asks: What is in your most fulfilled life? What else is important? What could be added? Anything else?

It’s about peeling back the onion layers to discover everything — not just surface level answers most of us are accustomed to giving.

I think of the first conversation as the 50,000 foot view. Let’s identify everything that is important to you — without any filter.

It’s 60 to 90 minutes that are dedicated and focused on you and what is important.

When was the last time you took 90 minutes for yourself?

The conversation finishes with inspirational work for you to complete before our second conversation.

Inspirational Work: Kinder’s 3 questions and Heart’s Core Grid

I’ll go into Kinder’s 3 questions later in this article. It’s a process to help narrow down what is most important to you.

Heart’s Core Grid helps people figure out what needs to be in your life to have meaning. It helps separate what must be in your life from the obligations. It identifies the differences between what you have to do or who you have to be from the fun things you get to do or be.

Dare to Dream Meeting – Conversation #2

The second conversation is where it gets deeper.

I may ask what it was like completing the inspirational work from the first conversation.

We read the responses to the inspirational work together and go deeper to give me a better idea that out of all the important things, which are the most essential elements to have in your life.

You have the opportunity to tell me more about the important things and what they mean to you.

Then, once I have an understanding of what is important to you, I may ask for permission to paint a picture of an ideal life given what you have shared.

It’s a summary of what I heard, and then you have the opportunity to tell me if I painted it completely, if something needs to be changed, or if anything is missing.

We wrap up our second conversation with more inspirational work before our third meeting.

Inspirational Work: Ideal Day, Week, and Year

The Ideal Day, Week, and Year inspirational work has you write down what an ideal day, week, and year would look like and then you get to compare it to how you currently spend your days, weeks, and years. It can be quite eye opening to see where there is a disconnect and where you are already living your ideal life.

What Could Possibly Get in the Way? – Conversation #3

The third conversation is one of my favorite conversations because it identifies everything that could possibly get in the way of you reaching your ideal life and solutions are created to solve each one.

Through questions, such as “How will you approach it?”, you come up with your own solutions. From there, I may ask, “When do you see that happening?” to help put a time frame on it. Finally, I may ask, “Who would be a good person to help keep you accountable?” to help put public accountability to overcoming any obstacles.

Each hurdle is approached one-by-one, so it doesn’t feel overwhelming and you have a clear path of what needs to be done going forward.

The third conversation is where small actions start to take place that can lead to meaningful changes.

We finish our third conversation with more inspirational work to bring everything together.

Inspirational Work: Goals for Life

The Goals for Life allows you to zoom out and think about what you want to accomplish in different time frames, such as one week, three months, one year, ten years, and during your lifetime. Then, you put a number in each box for which is your most important priority, then next most important, and all the way down to the last priority. The best way to complete it is to write down what comes up first — without thinking too much — and then ranking the priorities. It’s not about what makes the most sense. It’s about writing down the goals from your gut.

I Know Where I Am Going Meeting – Conversation #4

The fourth conversation is where we enter the realm of “traditional financial planning.”

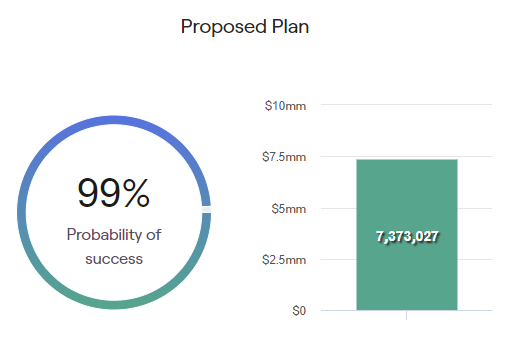

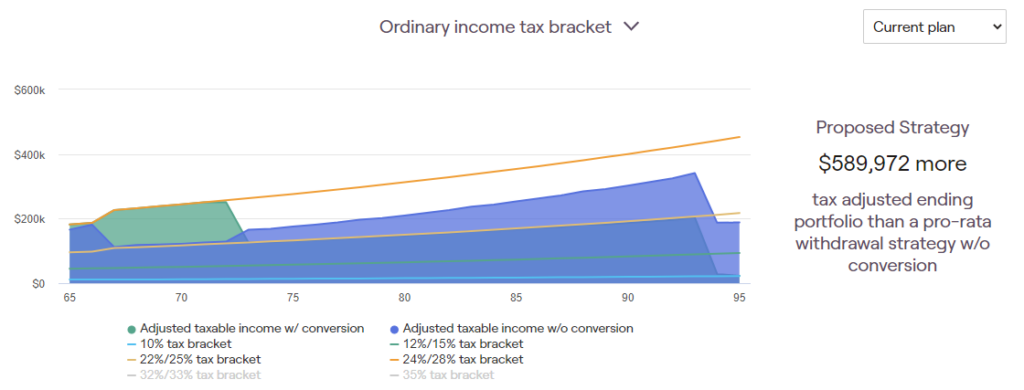

We bring your ideal plan to life by putting everything you want to do into a financial planning software that can stress-test market returns, downturns, higher inflation, wars, economic innovation, and changing economic conditions to see the likelihood of it working out.

This is also where we can start to see tax planning opportunities, gaps in insurance, how gifting would impact your plan, and estate planning issues.

The financial planning software is meant to help provide peace of mind that you are on track, see the impact of changing investment allocations and how much risk you may need to take with your investments, and provide a framework for saving prior to retirement and spending throughout retirement.

The financial plan is not a one-time event. It’s a living, breathing plan that changes. It’s something I come back to with clients regularly — through market ups and downs — and as your life changes. It’s the tool I use to answer the question, “What if I did XYZ? How would that affect things?”

Investment Meeting – Conversation #5

The last step before we start to prioritize other planning conversations, such as insurance, estate planning, college planning, tax planning, and more is to discuss the investment transition.

This is where we can align your money with your ideal life.

Now that I know more about you, what you are hoping to accomplish, and what an ideal retirement looks like, I can show you how I would invest your assets to align everything together.

You get to see how I would invest your accounts, your overall mix of stocks to bonds, and how strategies like asset location may be integrated into the portfolio.

We also talk about stock market history, expenses of the investments, and how I manage portfolios.

Education is an important part because the more you know what I am doing and why I am doing it, the more likely you will be to stick with the investments through good and bad times.

This ultimately leads to more success in living your ideal life.

After our fifth conversation, you either sign off on the investment transition, or we make adjustments as needed before you sign off, and I begin the process of transitioning your investments.

This is the last step in the initial life planning process. Then, we meet on a regular basis and as needed in order to integrate other financial planning decisions, discuss investments, and help as an accountability or thinking partner during life decisions.

What are Kinder’s 3 Questions?

George Kinder, often referred to as “The Father of Life Planning”, came up with these three questions before financial planning even became popular.

He was a little before his time.

When most of the financial industry was still focused on only the investment side of the industry (with product and trading commissions), Kinder was asking these more important questions.

It’s only over the past decade or so as more firms integrated financial planning into their practices that these questions have become more popular and familiar.

You are starting to see more people integrate some version of life planning into their client experiences.

Question #1

I want you to imagine that you are financially secure, that you have enough money to take care of your needs, now and in the future. The question is…how would you live your life? Would you change anything? Let yourself go. Don’t hold back on your dreams.

Describe a life that is complete, that is richly yours.

This is the “fun” question. It’s usually the easiest of the bunch because you have all the money you need — you are financially secure. It’s no longer a worry.

But, it can also be a very challenging question. How often do you dream about what you could do and how you would change your life?

People sometimes struggle with this question. They come up with 3 to 5 things they want in their life, often what society or others tell them they need.

It’s only after some uncomfortable silence and inquisitive feelings that the onion layers start to get peeled back to see what a completely rich and true life would look like.

Question #2

This time you visit your doctor who tells you that you have only 5 to 10 years left to live. The good part is that you won’t ever feel sick. The bad news is that you will have no notice of the moment of your death. What will you do in the time you have remaining to live?

Will you change your life and how will you do it?

Yikes, this one feels closer to home. You may have thought you had 20 years left to — now, it’s 5 to 10 years.

Sitting in those feelings can be uncomfortable.

You may start to realize the things you thought were most important are less important.

It’s inspiring to see not only what comes up for people, but how they will change their life.

Question #3

This time your doctor shocks you with the news that you have only one day left to live. Notice what feelings arise as you confront your very real mortality. Ask yourself:

What did I miss? Who did I not get to be?

What did I not get to do?

This question can result in tears.

It’s not about how you would spend your last day.

It’s about who you did not get to be in this one authentic life of yours. It’s about what you didn’t do. It’s about all of the things you missed out on.

Then, a clearer painting starts to develop of what an ideal life looks like for you, and only you.

Here is the disclosure and attribution to Kinder’s 3 questions and other material in this article: “This material was developed by George Kinder and Kinder Institute of Life Planning. It is part of a training program that leads to the Registered Life Planner® designation. Used by permission of George Kinder © 1999-2023.”

How Do I Find a Life Planner?

Every financial planner does life planning a bit differently. For those who trained through the Kinder Institute of Life Planning, you may find that they use a similar process, but tailored to their style and way of working.

You can find a Registered Life Planner® using the Kinder Institute Find a Life Planner tool.

Other financial planners may incorporate pieces of training from other programs, learning, and books.

The key is finding a financial planner who focuses on more than the money. If a financial planner is not exploring what is important to you and merely helps you make investment decisions, you may be in the wrong place.

What If I Want to Do Life Planning on My Own?

You may be wondering if you can do life planning on your own.

You can — sort of.

You can do it, but I don’t think it’s as effective. As someone who went through the training, tried to do life planning for myself, and then went through it with a partner, I discovered it’s far more effective to have someone else help guide you through the process.

They ask better questions, dig deeper, and hold you accountable.

If you want to try it on your own, there are resources and steps to walk you through the life planning process.

It can give you a taste of what it is, but to experience the real thing, I’d consider a financial life planner.

Final Thoughts – My Question for You

Financial life planning is more than money.

It’s about you. It’s about your values. It’s about discovering and living your ideal life.

Although it may seem obvious that a financial planner should first understand what you want to accomplish and your values before talking about anything else, most people have dreams for their lives that are closely guarded and beliefs or fears around money that go unnoticed.

It’s more challenging to explore what is important to you, but it’s vital to explore the human side of money first.

It leads to a better financial planning process and peace of mind that everything is working in coordination for you.

I’ll leave you with one question to act on.

When will you start the life planning process?