What is it like working with a virtual financial planner?

For many people, it can be a new experience. They may be used to going into their financial planner’s downtown office, in a crowded city, with cramped parking, and rush hour traffic.

The office may be a little too sterile or fancy, devoid of any personality.

At least, that’s been my experience and what people have told me in the past.

Working with a virtual financial planner can be a nice change — less driving, easy access to your files, and more convenient — all from the comfort of your own space.

For people who are used to going into an office to work with a financial planner, I’m going to talk about what it’s like working with me virtually. Every virtual financial planner engages with clients differently.

This is my way of working with clients virtually.

What is a Virtual Financial Planner?

Before we get into how I work with clients virtually, let me explain what a virtual financial planner is.

A virtual financial planner is simply a financial planner who works virtually.

They meet with families remotely over a video call, such as Google Meet or Zoom, instead of in an office setting or at your home.

Virtual financial planners may help you in the following ways:

- Discover what an ideal life looks like for you and how the money you have saved can support your ideal life

- Do long-term tax planning to help reduce the amount you pay in taxes

- Develop a financial independence plan to help give you confidence about retiring or making work optional

- Create a personalized investment plan to support your income needs

- Discuss estate planning ideas to help make sure settling your estate is not a burden on loved ones and you don’t pay more in estate taxes than necessary

- Review insurance policies to identify potential risks to your financial life

- Proactively let you know of legislation that may affect you and financial planning strategies

- Help give to charity as tax-efficiently as possible

- Meet with you on a regular basis and be available for any questions or concerns you have through the stock market ups and downs

I like to think of a virtual financial planner as a “thinking” or “accountability partner” in your life.

I can provide education, be a sounding board, and help people come to the decision they think will fit their life best.

Why Should I Hire a Virtual Financial Planner?

There are a few reasons you may want to consider a virtual financial planner over someone locally.

Although it can be nice to see someone face-to-face in your local area, there are disadvantages to limiting your geographic search for a financial planner.

Expertise & Finding a Better Fit

By considering hiring a virtual financial planner, you open up the number of financial planners you can work with.

Some cities only have a limited number of financial planners, particularly fee-only, fiduciary advisors.

Also, by expanding your search, you may be able to find a virtual financial planner with more expertise and experience working with people in your similar situation.

For example, I focus on working with widows and caregivers. Other financial advisors in your city may be uncomfortable working with widows, or they may be terrible listeners and give advice without getting to know you (there is a reason an estimated 80% of widows fire their existing financial advisor after a spouse’s death). They may also be unaware of some of the tax planning opportunities, Social Security claiming strategies, and the emotions around losing a spouse.

By considering a virtual financial planner, you get the opportunity to work with financial planners across the United States.

You may find someone who you connect with better and who can provide better advice given your situation.

If you are thinking about hiring a virtual financial planner, you should have a conversation with them and ask these 10 questions before hiring a new financial planner.

Saving Time & Easier Scheduling

Another benefit of hiring a virtual financial advisor is that it may save you time.

I used to work in a downtown Seattle high-rise office building.

While some people made a day out of coming downtown and had lunch or saw a show in the evening, I found many people disliked driving downtown, trying to find the parking garage on one way streets, navigating the tiny spots, and getting stuck in rush hour traffic that seemed to happen more than half the day.

Instead of driving to an office, clients may schedule a strategy meeting with me during their lunch break or take an hour at the end of the day for a meeting.

It’s much easier to hop on a quick call or video meeting from home.

If you had to go into an office, it might be 15 to 45 minutes each way, which meant with an hour or longer meeting, that meeting might take three hours from your day — the better part of your morning or afternoon away from work, family, or friends to make a meeting.

Clients can easily call me or do a screen sharing meeting if they need to show me an online account or we need to go through something together online. It’s much easier to fit in a 30 minute call and have it actually be 30 minutes.

I’ve found being a virtual financial planner means that my clients save time, and it’s easier to find a time to meet.

Save Money

You may also be able to save money by working with a virtual financial planner.

There are the small savings, such as potentially paying less in gas, parking fees, and other expenses when you are out and about.

More importantly, working with a virtual financial planner may mean less in investment or financial planning fees. In my experience, many of the large brokerage firms that have offices with “financial consultants” or “wealth advisors” often have more expensive funds. They may use proprietary funds and the “wealth advisor” may be compensated based on how your investments are allocated.

Or, worse, you end up with a “financial advisor” who is really an insurance salesperson, and every solution or strategy proposed has an insurance component where you don’t see the fees directly, but you pay an opportunity cost being in a product that may not support your ideal life, your money is not as easily as accessible without penalties, or the product doesn’t work as you thought it would.

Although virtual planners have a variety ways of working with clients, I am 100% fee only and a fiduciary. The only way that I’m compensated is by what clients pay me.

I don’t receive compensation based on what I recommend, earn commissions from the investments I suggest, or sell insurance products.

If an insurance solution is needed, I make referrals to insurance specialists I trust to get coverage in place.

You may be able to save money by working with a virtual financial planner.

More Fulfilled Planner

Another intangible benefit may be that you get to work with a more rested, fulfilled financial planner.

I’ve worked with 115 clients while doing most of the administrative paperwork, tax planning, financial planning, investment strategies, insurance reviews, and more, with the expectation that I would one day work with 150 clients.

I was exhausted, stressed, and didn’t have much of a life outside of work, which made it harder to be a good financial planner.

According to Dunbar’s number, we can only maintain about 150 relationships.

Within that number are different layers:

- Loved ones: 5 people

- Good friends: 15 people

- Friends: 50 people

- Meaningful contacts: 150

- Acquaintances: 500 people

- People you can recognize: 1,500

I only want to have clients who I have relationships with — not acquaintances.

That means I am limited to far less than 150 people. Let’s do the math.

I’m married. My parents are both alive, and I have a relationship with both. My wife’s parents are still alive. I have a small family with a couple of aunts and uncles.

Within my family circle, there are already about 15 people. If I add good friends and friends, that’s another 20 people.

Already, I’m around 35 people before I include professional relationships and families I work with.

I’d like many, if not all, of my clients to fall into the category of friends, but realistically, that leaves about 15 relationships for the category and the rest in “meaningful contacts”, which is still a good relationship.

If I add professional relationships and other relationships I have to the original 35 people before clients, I’m likely over 50 people and more realistically, probably close to 75 people.

That means at most, I have room for 75 more “meaningful contacts” in my life.

It’s easy to see why I felt stressed trying to develop and grow 115 client relationships and shuddered at the thought of trying to make it to 150 clients.

I’m purposefully limiting Kindness Financial Planning, LLC to about 50 clients with whom I’ll work.

It feels like the best mix between my personal life and providing a very high level of service and availability for clients.

Since I’m not trying to serve 100 to 150 clients like some other financial planners, and I’m not trying to build a model like a big brokerage firm, where they can have hundreds or thousands of clients, I can show up ready to listen, empathize, and help guide clients to a more ideal life.

I’ve noticed many other virtual financial planners are being intentional about the number of people they serve.

There’s value in working with a virtual financial planner who limits the number of clients with whom they will work.

I’ve found I am showing up better for clients — asking more questions, listening better, and having the time to go deeper on what really matters most to them.

What are the Disadvantages of Hiring a Virtual Planner?

Having worked for a decade as a financial planner who primarily worked in person, along with a few virtual relationships, I know firsthand there are disadvantages of working with a virtual planner.

Some Things are Easier in Person

First, some things are easier to do in person.

If you have a box of documents you want scanned, I could grab the box and scan them for you while in person.

Virtually, you’ll need to do it at home with a scanner or app on your phone or go to a store to scan them. That’s more work for you. Thankfully, more documents are delivered electronically now, but there is still the occasional document you may need to scan.

Virtual Isn’t for Everybody

Second, being on the computer screen is not the same as being in person. I wish I had a better way to frame it, but it’s just different.

For some people, they want that in person connection and are opposed to building a relationship virtually.

Having done life planning virtually and having never met some clients in person, I know virtual can work for some people, but probably not all people.

I’ve built meaningful relationships, provided advice, and been an integral part of someone’s life — while only working virtually.

Technology

Some people are not as great with technology as others. They see it as a barrier.

I hear this from many people, but if I can help someone in their late 80s who claims to be bad with technology get on a video call and work virtually, I don’t see this as too big of a hurdle.

I’m extremely patient and dedicated to having the financial planning experience be a good one. There are very few times I haven’t been able to come up with workarounds when we hit a snag with technology.

And if we do, there is always the option to mail documents or enlist the help of family members or friends to help with the technology.

For those who don’t want to deal with technology at all, hiring a virtual planner is not just a disadvantage, but probably not an option.

What Is It Like Working with a Virtual Financial Planner?

Now that you know the advantages and disadvantages of working with a virtual financial planner, let’s look at what it is like working with me.

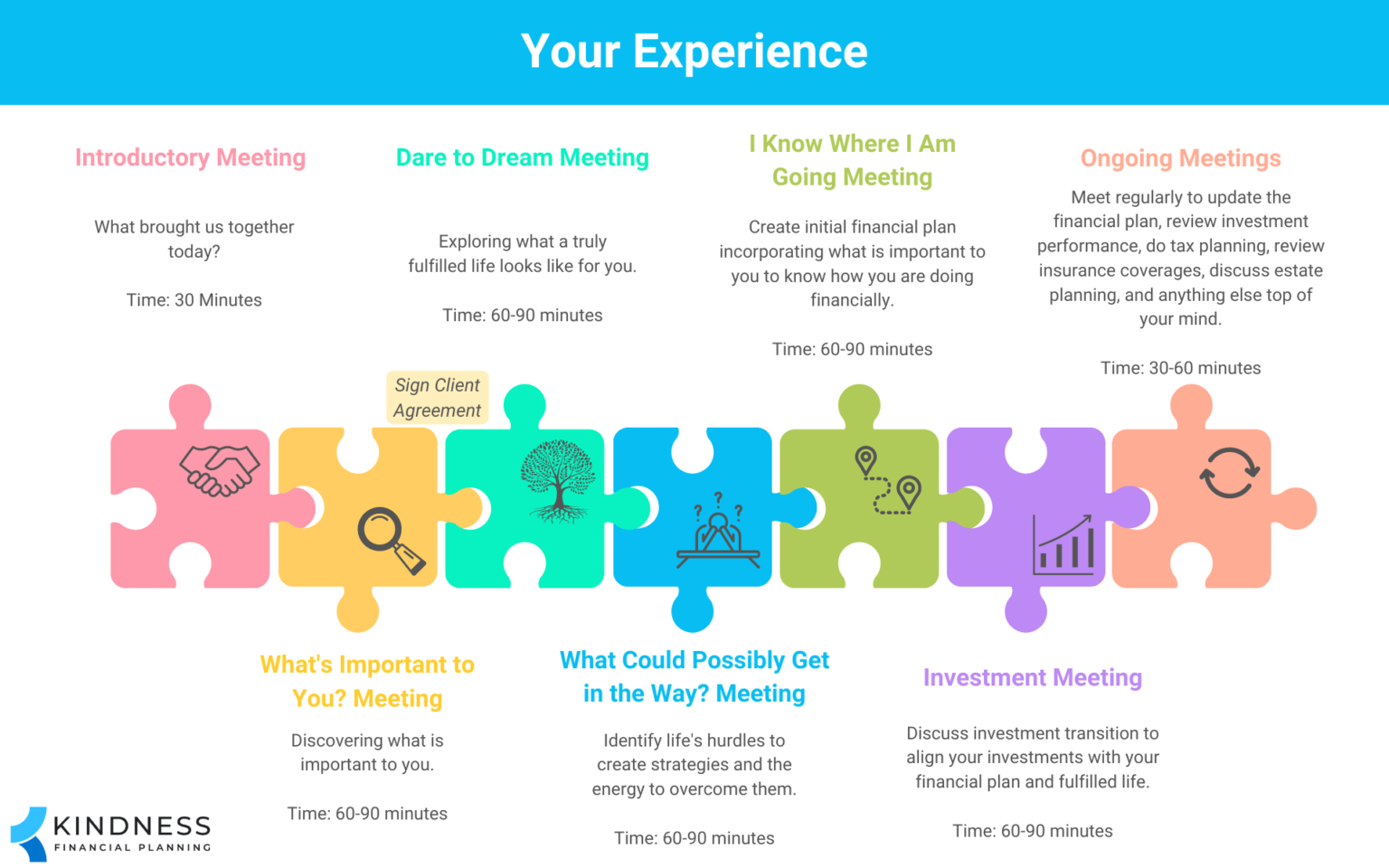

Onboarding Process

I begin with a 30 minute introductory call to explain my background, how I work with clients, but more importantly, to learn what brought you to me today.

It’s an opportunity for you to share what you are looking for, what’s on your mind, and figure out if we would be a good fit for each other.

If not, I can provide resources or methods of finding another financial planner who would be a better fit.

If you decide it may be a good fit, we schedule a “What’s Important To You?” meeting. This meeting is dedicated to discovering what is important to you.

When’s the last time you experienced 60 to 90 minutes where a financial planner asks you questions to discover what’s important in your life?

If after that point we feel we should work together, we sign the client agreement.

I send my client agreement via a secure electronic signature platform, set you up with Right Capital (my financial planning software, which includes a secure vault to send files to each other), and we start to collect important financial documents.

Below is an example of the financial documents I may initially ask for:

- Most recent pay stub

- Last two years of tax returns

- Statements for current investment and bank accounts

- Social Security benefit statement

Over time, I’ll ask for auto, home, and umbrella insurance coverages, as well as your estate plan, and other important documents.

We’ll continue working through my initial consultation process, which includes a “Dare to Dream” meeting, “What Could Possibly Get in the Way? meeting, a financial independence plan meeting, and then an investment transition meeting.

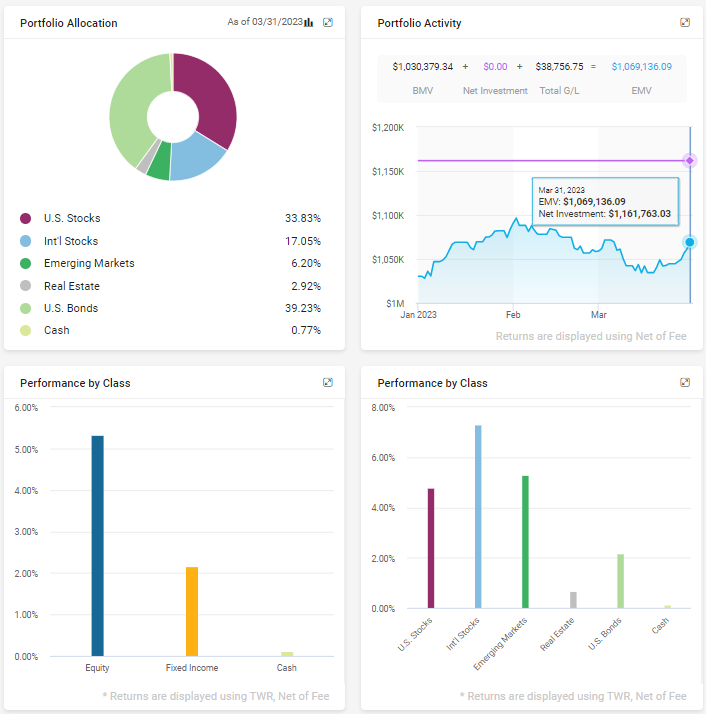

Throughout the process, you’ll always have full control of your financial accounts on Charles Schwab, which is where my clients’ have their assets. I’m simply connected to accounts via a limited power of attorney, which allows me to trade the accounts (to manage within the investment policy statement we build together) and debit my management fees.

After the investments are transitioned, you’ll also be given access to an investment portal, which does a better job of explaining how you are invested (mix of stocks vs. bonds and other asset classes) and performance.

Throughout the onboarding process, I’m available through email, phone calls, or video calls.

Security

The security of your private information is extremely important.

For my financial planning software and vault, you can enable two-factor authentication. The infrastructure is hosted and managed within Amazon’s secure data centers. Your personally identifiable information is encrypted using AES-256.

The financial planning software also gives you the option to link your accounts using Envestnet | Yodlee. The data is “view only” — meaning no money transfers can be initiated from the financial planning software. Envestnet | Yodlee is used by some of the largest U.S. banks and undergoes rigorous examinations and audits.

Since the assets are held at Schwab, you also can learn about Schwab’s Security Guarantee. You can also learn more about how your assets are protected at Schwab, such as FDIC, SIPC, and “excess SIPC” coverage.

Since files are not shared over email, assets are held at Charles Schwab (which has $7.38 trillion client assets as of February 28, 2023), and we are not working together on paper files, your important information is stored in secure areas with two-factor authentication whenever possible.

Meeting Process

After the onboarding phase, we’ll prioritize which financial planning areas we need to tackle first.

For example, if you don’t have an estate plan, I may provide a referral to an attorney to help you create a Will or Trust, Powers of Attorney, and other legal documents.

If there is a need for life insurance, I may provide a referral to an insurance agent who can get to know your health and help you shop around for the right insurance carrier.

We typically meet on a quarterly basis for at least the first two years. This is usually enough time to get through the major financial planning areas, for you to better understand the investments, and build confidence that you are on a good path.

After about two years, meetings tend to naturally go to 1 to 3 times a year, though it depends on what’s happening in your life and what you prefer. We normally have a conversation and set expectations about how often you’d like to meet around the two year mark.

There is no set limit or time table to meetings. As an accountability and thinking partner, there are certain times I’d like to meet, but I’m here for clients as needed.

We may meet 10 times in a month if you are going through a major life transition, such as buying a new home before selling your current one.

My calendar scheduling link is always open to you, I respond to almost every email within 24 hours (usually the same day), and I’m reachable by phone.

You can get financial advice from the comfort of your own home through a video call.

Meeting Follow Up

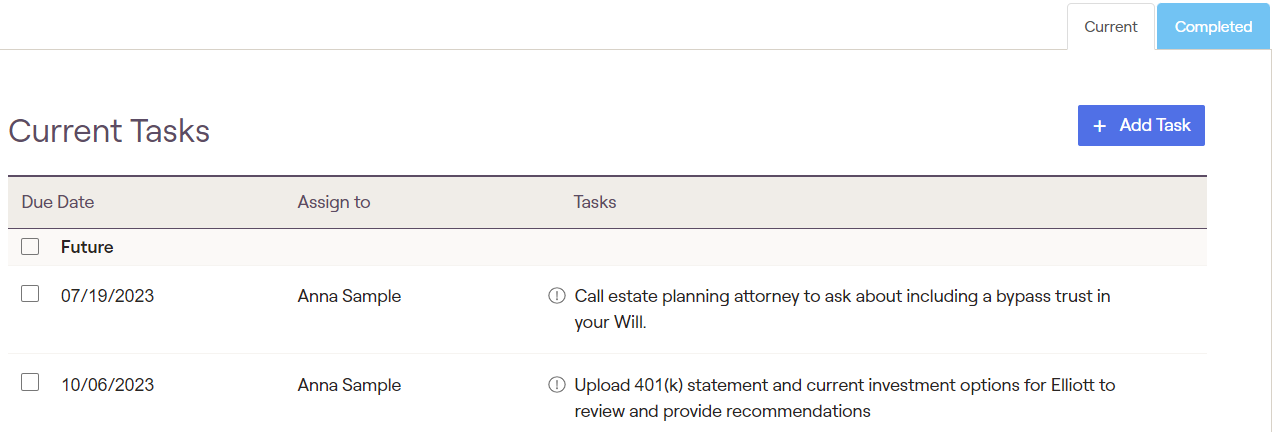

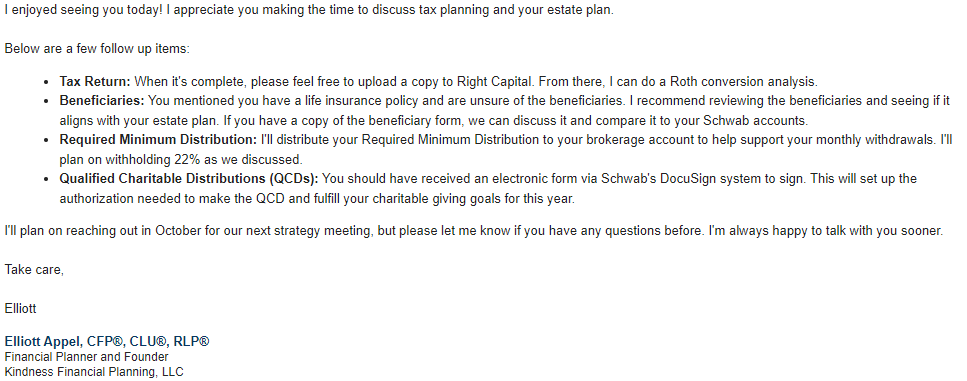

After our meetings, I normally send a follow up email with the next steps you’ll need to take and create a “task” in Right Capital, so you’ll have a reminder of what needs to be done.

I’ve been told the email summary is really helpful. It provides a brief overview of what needs to be done, so you can focus on the most important things and get back to your day.

If we cover a report about how to claim Social Security benefits, how much of a Roth conversion to do, or update the financial independence plan, I may also upload a report in case you ever want to go back and look at what we discussed.

Final Thoughts – My Question for You

Working with a virtual financial planner can be a great way to feel better about your money, learn about financial planning strategies and investments, and have a thinking partner from the comfort of your home, office, or while traveling.

Instead of going into the office, you can meet with a virtual financial planner on your own time — when it works best for you.

For those who are worried about what it means to work together online, hopefully this article showed you how easy and accommodating it can be and the benefits of working with a virtual financial planner who may have more expertise to help you.

I’ll leave you with one question to act on.

What is a financial concern you’ve been wondering about that a virtual financial planner may be able to help with?