It’s important to review your tax return.

People rarely review their tax return, and if they do, they often don’t review it properly. They may review it to make sure everything is accurate, but they don’t think about common tax planning mistakes they may be making.

They don’t plan how to reduce their lifetime tax bill, such as with Roth conversions, charitable gifting, or gifting to family members.

Let’s look at how to review your tax return and look for tax planning opportunities.

Please note that I am reviewing tax planning mistakes from the perspective of someone who is retired or soon-to-be retired.

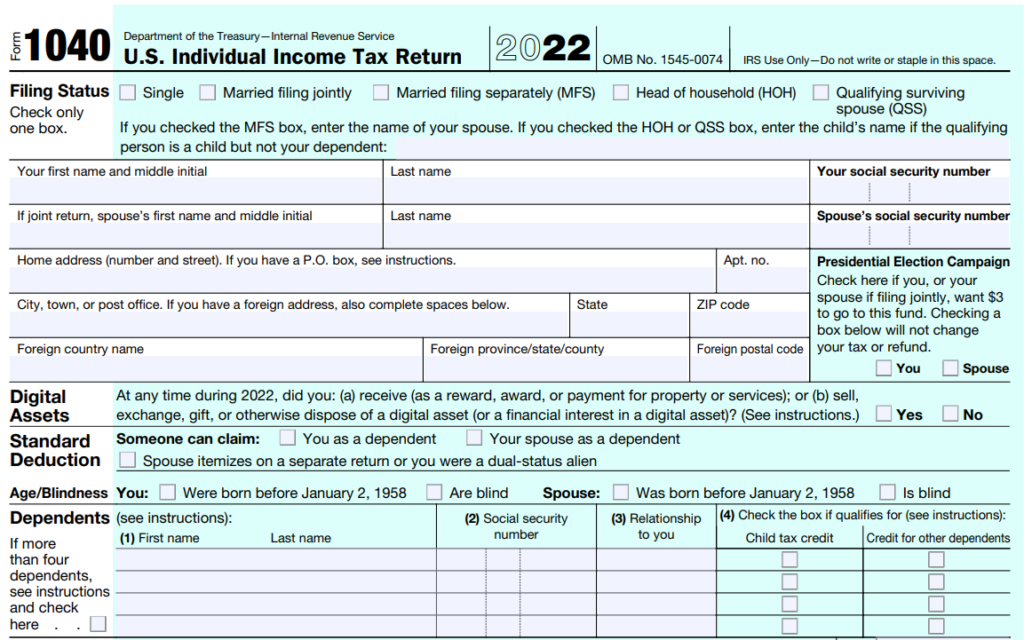

Before Line 1: Filing Status, Name, SSN, Address, Digital Assets, and Dependents

Before line 1 are the easier parts to complete. There are not many tax planning opportunities in this section, but there are many areas to make mistakes.

Filing Status

For married people, filing separately rarely results in lower taxes than filing jointly.

If you are a widow and your spouse died this year, you can still file jointly, though this may be your last year to file jointly.

Only under limited circumstances can a widow file as Qualifying Surviving Spouse (QSS), where she may still use the married filing jointly tax brackets. Qualifying Surviving Spouse status requires the surviving spouse to have a dependent child living with them all year, and paid more than half of the cost to keep up the home. It’s also limited to two years following the year of the spouse’s death if the surviving spouse remains unmarried.

For single people, they normally file as Single.

Head of Household rarely applies unless you provided more than half the support for a child or parent that was living with you for at least half of the year.

Name

Double check that you spelled your name correctly.

Social Security Numbers

A common tax filing mistake is incorrectly entering Social Security numbers. Are yours correct?

Address

Since the IRS will use this address to correspond with you, is it accurate?

If you need to update your address with the IRS, you can update it using Form 8822.

Digital Assets

Answer this question carefully. Given the hype in digital assets the past few years, you may have received a digital asset as a reward or exchanged, gifted, or sold it.

The IRS is increasing scrutiny in this area.

Dependents

Many retirees do not have dependents, but if you do, ensure someone else is not claiming them as a dependent because it can slow down the processing time.

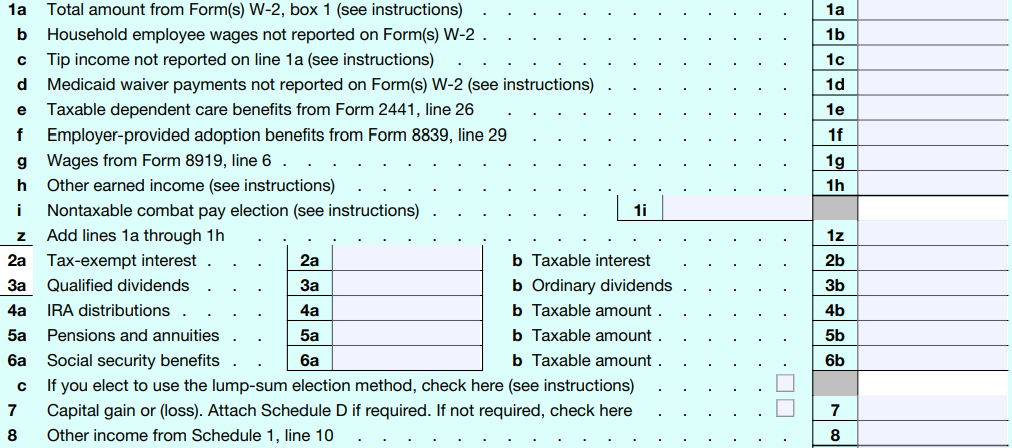

Lines 1 – 8: Income Sources

These are the areas where tax planning opportunities start to exist.

Line 1: Wages

Many retirees don’t have wages, but if you are not retired yet, here are a couple strategies to consider:

- Employer Retirement Plans

- Are you taking full advantage of a match?

- Are you considering your tax bracket today versus in retirement in deciding whether to contribute to the pre-tax or Roth portion of the plan?

- Does your plan allow for after-tax contributions and in-plan Roth conversions? If so, does it make sense to contribute?

- Health Savings Accounts (HSAs): If you have a high-deductible health plan that qualifies for an HSA, are you contributing through work?

Line 2a and 2b: Tax-exempt interest and taxable interest

Line 2a is usually municipal bond interest, which is tax-exempt interest on a federal level.

If the municipal bond was issued by your state of residence, the interest is usually tax-free on your state tax return. For example, if you had a California municipal bond and resided in California, the municipal bond interest may be tax-free on your California state tax return.

Line 2b is taxable interest, which could be interest from bank accounts and corporate bond interest in brokerage accounts.

Planning Tip: Depending on your tax bracket and how much municipal bonds are yielding versus corporate bonds, you may be better off owning municipal bonds over corporate bonds in your brokerage account. For example, if you are in the 32% federal tax bracket and municipal bonds are yielding 4% while corporate bonds are yielding 6%, your tax equivalent yield for the municipal bond is 5.89%. That’s calculated using the following formula: (tax-free municipal bond yield)/(1 – tax rate). In this case, the corporate bonds are still yielding more than the tax equivalent yield, so it may be better to own corporate bonds instead of municipal bonds — though keep in mind the risk levels may be different.

Planning Tip: Schedule B will list where you are receiving interest from. If you have multiple bank accounts and brokerage accounts, you may want to consider simplifying the number of accounts.

Don’t forget to report all interest earned. Although the form 1099-INT is only produced if you earn at least $10 in interest, you still need to report all interest earned, even if it is less than $10 and you did not receive a 1099-INT form.

Lastly, are you holding too much cash? If you have large amounts of interest, that could indicate you have more cash than you need. How much cash you need in retirement is a personal decision.

Line 3a and 3b: Qualified dividends and ordinary dividends

Line 3a shows qualified dividends, which are taxed more favorably than ordinary dividends because they are taxed at long-term capital gains tax rates.

Line 3b shows ordinary dividends, which are taxed as ordinary income, which is less favorable.

Planning Tip: If you have higher ordinary dividends, determine which investment is generating them. You may want to rebalance your portfolio to make it more tax efficient. Bond ETFs generate ordinary dividends. You may want to use asset location and hold them in a tax-preferential account, such as an IRA. That has to be balanced with how much money is needed in the near-term for withdrawals from your brokerage account.

Planning Tip: If you have accounts at multiple custodians, consider consolidating to make it easier to track your asset allocation, reduce the number of tax reporting forms, and make it easier to access your money.

Line 4a and 4b: IRA distributions

Line 4a lists the total IRA distributions. Line 4b lists the taxable amount of those distributions.

If you do a Roth conversion and have after-tax basis in your IRA, the taxable amount on line 4b should be less than line 4a since a portion is not taxable. Form 8606 will report your non-deductible IRA contributions, distributions, and Roth conversions when you have after-tax basis and make the pro rata calculation of how much is taxable.

Planning Tip: If you did a Qualified Charitable Distribution (QCD), you’ll need to account for it on your tax return. The 1099-R you receive will show the total distribution, but won’t separate the amount that went to charity via a QCD. For example, if you took a $20,000 distribution and $5,000 of it was a QCD, line 4a should list $20,000 and line 4b should list $15,000.

Line 5a and 5b: Pensions and annuities

Line 5a shows total income from pensions and annuities while line 5b shows the taxable amount.

If you surrender a non-qualified annuity, not all of it should be taxable. Line 5b should be less than 5a.

Line 6a and 6b: Social Security benefits

Line 6a lists the total Social Security benefits while line 6b lists the taxable amount.

Line 6a is not what is paid to you — it’s the gross, or total, amount before Medicare costs, IRMAA adjustments, or additional tax withholdings.

Not all Social Security benefits are subject to tax. At most, 85% of Social Security benefits are taxable. In some cases, Social Security benefits are not taxable at all. The amount of Social Security benefits that are taxable is based on “Provisional Income.”

Provisional Income = Adjusted Gross Income (AGI) + ½ of your Social Security Benefits + Tax-Exempt Interest

Reducing your income could make less of your Social Security benefits subject to taxation.

Planning Tip: In some cases, it can make sense to undo filing for Social Security benefits or suspending Social Security benefits to allow more room for Roth conversions and benefit from delayed Social Security retirement credits.

Line 7: Capital gain or loss

Line 7 lists your capital gains or losses, which could be from selling assets in a brokerage account, capital gain distributions from mutual funds, a home sale, or other tangible assets.

Planning Tip: If you have large capital gain distributions from tax-inefficient mutual funds, you may want to consider the tax consequences of selling versus the tax consequences of remaining in the fund in future years.

Planning Tip: If you have a $3,000 capital loss carry forward, you may have other losses you can use to offset future capital gains. You could use these losses to sell other assets with capital gains and potentially offset them.

Line 8: Other income

Line 8 lists other income, which could include many different sources, such as:

- Taxable refunds

- Alimony

- Business income

- Rental real estate, royalties, trusts, S corporations

- Gambling income

- Jury duty pay

- Stock options

- Hobby income

Planning Tip: These are areas where you want to be sure you are properly reporting income and taking any appropriate deductions, such as business expenses and rental depreciation. It may make sense to work with an accountant to ensure you are taking the appropriate deductions and reporting income properly.

Lines 9 – 15: Total Income, Adjusted Gross Income, Itemized Deductions/Standard Deduction, Qualified Business Income, and Taxable Income

Now that your income is accounted for, it’s time to total it, take deductions, and determine your taxable income.

Line 9: Total income

Line 9 is adding your total income from lines 1 through 8.

Line 10: Adjustments to income from Schedule 1

Line 10 are adjustments to income from Schedule 1, which includes categories such as:

- Health Savings Account (HSA) contributions

- Deductible part of self-employment tax for self-employed people

- Self-employed qualified plan contributions

- Self-employed health insurance deduction

There are others, and they are less common, but review Schedule 1 to make sure you are accounting for all adjustments.

Planning Tip: If you have access to an HSA, consider investing it for future medical expenses and spend money on current healthcare expenses with cash. Also, if you have an HSA with poor investment options or high expenses, consider moving it to another provider.

Line 11: Adjusted Gross Income (AGI)

Line 11 is your Adjusted Gross Income (AGI), which factors into many other calculations.

AGI can affect your Modified Adjusted Gross Income (MAGI) and eligibility for specific deductions, credits, and other programs, such as:

- Medicare IRMAA surcharges

- ACA health insurance premium tax credits, which can lower the cost of health insurance through a state or federal health insurance marketplace

- Whether you can make contributions to a Roth IRA

- Whether you can deduct IRA contributions

- Net Investment Income Tax (NIIT)

- Child tax credit

- Education credits

Planning Tip: Pay special attention to your AGI and how it may affect what accounts you can contribute to, credits you are eligible for, IRMAA surcharges, and additional taxes. For example, a Roth conversion can affect your AGI and cause an IRMAA surcharge that increases the cost of your Medicare.

Line 12: Standard Deduction or Itemized Deductions

Line 12 is either taking the standard deduction, or if your itemized deductions total more than your standard deduction, taking itemized deductions.

The standard deduction for 2023 is $13,850 for single filers (plus $1,850 if age 65 or older) and $27,700 for married filing jointly (plus $1,500 per person if age 65 or older).

Possible itemized deductions include:

- State and local income or sales taxes

- Real estate taxes

- Personal property taxes

- Mortgage interest (including points on a new mortgage)

- Disaster losses

- Gifts to charity (including unused carryover amounts up to five years)

- Medical and dental expenses

Planning Tip: If you are charitably inclined, you could consider “bunching” a few years’ worth of gifting into a single year to get over the threshold for itemizing deductions. You could even consider using a Donor-Advised Fund to make grants to charities over a longer time frame than one year.

Line 13: Qualified Business Income Deduction

Line 13 is Qualified Business Income Deduction, which allows owners of pass-through business to potentially deduct up to 20% of their qualified business income. There are income limits and other limitations to be aware of. with the QBI deduction.

If you are still working and self-employed, you may qualify for the QBI deduction. If you are retired, you may see small amounts of a QBI deduction due to REIT dividends held in a brokerage account.

Line 15: Taxable Income

Line 15 is taxable income, which helps you determine your federal marginal tax bracket and your total tax.

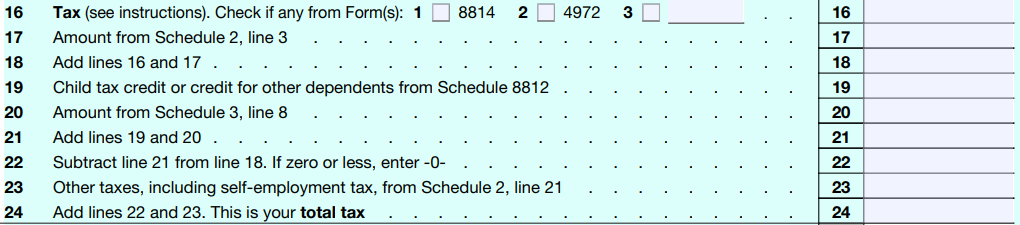

Lines 16 – 24: Tax and Credits

Now that you know your taxable income, let’s look at what you owe.

Line 16: Tax

Line 16 is the total amount of tax you owe before any credits, alternative minimum tax (AMT), repayment of ACA health insurance premium tax credits, and other adjustments.

Line 17: Amount from Schedule 2, Line 3

Line 17 has to do with additional taxes from Schedule 2, which is the alternative minimum tax or repayment of the ACA health insurance premium tax credits.

AMT normally applies when people exercise Incentive Stock Options (ISOs), recognize a very large capital gain, or have a very high household income.

Planning Tip: If you thought you qualified for ACA health insurance premium tax credits and paid less for your health insurance throughout the year, but ended up making more money than you stated, you may need to repay those credits. If you want to be more conservative, you can forgo the tax credits throughout the year and have them paid to you via the tax return when you file (if you qualify).

Line 19: Child tax credit or credit for other dependents

Line 19 is the child tax credit.

Planning Tip: Pay special attention to the situations where a child can be claimed. This is an area many people get wrong. Pay attention to ages and phaseouts of the credit.

Line 20: Amount from Schedule 3, Line 8

Line 20 is the amount from Schedule 3, which includes additional credits and payments, such as:

- Foreign tax credit

- Residential energy credits (such as energy-efficient home improvements)

- Qualified electric vehicle credit

Planning Tip: If you are planning on buying an electric vehicle, see if a credit is available. There are many limitations to who qualifies and which vehicles qualify.

Planning Tip: Foreign stocks often produce foreign dividends, and a portion of it may be withheld in the issuer’s home country for taxes. You can often get that money back, so you are not being taxed on it twice (once in the foreign country and once in the U.S.). If you paid foreign taxes due to investments held in your taxable brokerage account, make sure you account for them on Schedule 3. Your 1099 in your brokerage account should specify your foreign taxes paid, which you can use to determine your foreign tax credit.

Line 23: Other taxes, including self-employment tax

Line 23 includes other taxes from Schedule 2.

Schedule 2 includes the alternative minimum tax (AMT), repayment of the advanced premium health care credit, self employment taxes, net investment income tax, Medicare payroll taxes for those with high incomes, 6% excise tax on excess IRA, Roth IRA, or HSA contributions, and the penalty for missed RMDs.

Planning Tip: The 3.8% net investment income tax can be planned around by managing your MAGI, such as limiting capital gains in a high income year, creating installment sales when selling property, and donating appreciated property instead of selling investments with long-term capital gains.

Line 24: Total Tax

Line 24 is the total tax before taking into account withholdings, estimated tax payments, or refundable credits.

The total tax is a key figure for tax withholdings and estimated tax payments because you can calculate a safe harbor amount to protect yourself from underpayment penalties.

You may face underpayment penalties if you don’t withhold enough taxes or make estimated tax payments that equal:

- 90% of the current year’s total tax (line 24), or

- 100% of the prior year’s total tax if prior year AGI was under $150k or 110% of the prior year’s total tax if prior year AGI was $150k or more, or

- You owe less than $1,000 in tax after subtracting your withholdings and credits.

Planning Tip: Withholding money is generally better than making estimated tax payments because money can be withheld at any point throughout the year. For example, you could make one large withholding in December and still potentially not face underpayment penalties. If you make estimated tax payments, they generally need to be paid in four equal installments. You generally can’t make a large estimated tax payment in December and avoid underpayment penalties.

Planning Tip: When doing Roth conversions, it’s important to plan for your safe harbor amount because it’s generally better to make estimated tax payments if you have cash or brokerage assets than withholding money from the Roth conversion.

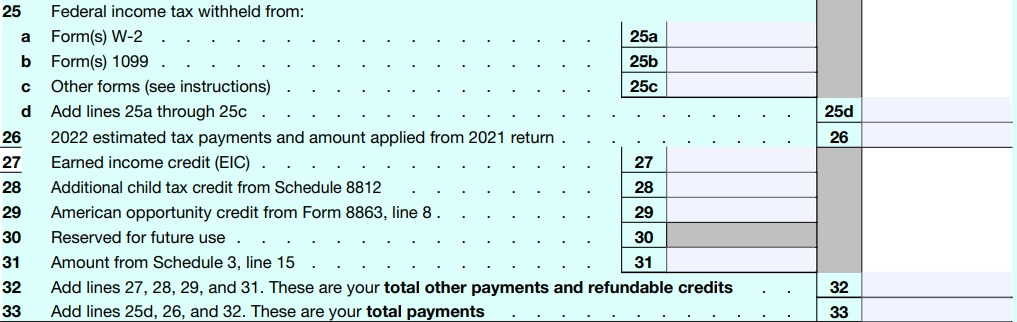

Lines 25 – 33: Payments

Lines 25 through 33 reflect the income tax withheld, estimated tax payments made, and other credits to subtract from your total tax to then determine how much you are overpaid or the amount you owe.

Line 25: Federal income tax withheld

Line 25 captures the federal income tax withheld from W-2 jobs, 1099s and other sources.

Planning Tip: If you are still working, you may want to occasionally add up your estimated withholdings for the year to determine if it will be enough to cover your total tax. If not, you may want to increase your withholdings to avoid a surprise when you file your tax return. On the other hand, if you are withholding too much, you are giving the government an interest free loan and may want to reduce your withholdings.

Line 26: Estimated tax payments and amount applied from prior year return

Line 26 includes the estimated tax payments you made, as well as any overpayment you had applied from your prior year tax return to this year.

Planning Tip: As you make estimated tax payments through EFTPS or Direct Pay, I recommend printing a PDF of each tax payment and putting it into a tax folder on your computer. It makes it easy to remember how much you paid and when as you file your tax return.

Line 31: Amount form Schedule 3, Line 15

Line 31 includes amounts from Schedule 3, which are foreign tax credits, qualified plug-in motor vehicle credit, residential energy credits, additional ACA healthcare exchange premium tax credits if the estimated income was too low, and others.

Planning Tip: If you retire before Medicare and need to buy health insurance off of the healthcare exchange, it’s important to estimate your income, but if you underestimate, you will get those tax credits back when filing your tax return.

Line 33: Total Payments

Line 33 is the total of lines 25d (tax withholdings), 26 (estimated tax payments and overpayments applied to the current year), and 32 (refundable credits).

Lines 34 – 36: Refund

If you paid in more than you owe, you get a refund and can say what you want done with it.

Line 34: Amount you overpaid

If you paid more than your total tax, line 34 is the amount you are overpaid (line 33 minus line 24)

Line 35: Amount you want refunded to you

Line 35 is the amount you had refunded to you.

Planning Tip: The fastest way to get your tax refund is to have it electronically deposited. The IRS issues more than nine out of ten refunds in less than 21 days.

Line 36: Amount of line 34 you want applied to your next year estimated tax

If you decide not to have the full refund deposited to your bank account, line 36 captures how much of your overpayment will be applied to your next year’s estimated tax.

Having your overpayment applied to the next year can be an easy way to potentially avoid needing to make an estimated tax payment.

Lines 37 – 38: Amount You Owe

If you did not pay more than your total tax, this is where you’ll calculate how much you owe and the estimated tax penalty.

Line 37: Amount you owe

Line 37 the amount you still owe (line 24 minus line 33).

Planning Tip: Assuming you follow the safe harbor amount and avoid underpayment penalties, it’s okay if you owe the IRS money when you file. You received an interest-free loan from the government. For example, if you owe $10,000 at tax time, but you met the safe harbor requirements, you had an extra $10,000 over the past year that could have earned interest or been used to enjoy life.

Line 38: Estimated tax penalty

If you didn’t pay enough through withholdings or estimated tax payments, you may owe interest on the shortfall.

The interest is calculated on form 2210.

Planning Tip: If your income fluctuates throughout the year and you face underpayment penalties, you may be able to use the annualized income installment method to reduce penalties.

Planning Tip: You can see the quarterly interest rates charged by the IRS to decide how on top of your estimated taxes you want to be. Interest is compounded daily. Q1 of 2023, interest for underpayment penalties was 7%.

Common Tax Return Questions

Below are a few tax return filing questions people ask.

How long should I keep my tax returns?

The IRS has different suggestions about how long to your tax returns and records depending on different situations; however, a general rule of thumb is for 7 years.

Seven years covers most situations, except if you do not file a return or if you file a fraudulent return.

However, given how cheap cloud storage and backup storage is, why not scan your files and keep them indefinitely?

Planning Tip: Create a folder on your device called “Taxes” and put a sub folder with the tax year (i.e. 2023). As you receive tax documents or have supporting documents (i.e. charitable receipts), download them into that folder or if they come via mail, scan them, and upload them to that folder. Your records won’t take up physical space, and you don’t need to worry about how long to keep them.

Should I take the standard deduction or itemize?

Many people are confused about whether they should take the standard deduction or itemize their deductions.

If your itemized deductions are not greater than the standard deduction, you likely are taking the standard deduction.

Planning Tip: If you do a ballpark estimate of your itemized deductions, and it’s unlikely they are greater than the standard deduction, don’t waste your time adding everything up. You could simply take the standard deduction.

What are common tax filing mistakes?

Many tax filing mistakes are avoidable. It requires time to review the return and catch errors before filing.

Below are some of the tax filing mistakes the IRS mentions on their website.

- Filing too early: if you file before you have your tax reporting documents, you may need to amend your tax return with the complete information

- Inaccurate information: double check the numbers you or your accountant input. It’s common to transpose numbers or type in the wrong numbers.

- Inaccurate or missing Social Security numbers: Don’t forget to put the correct SSN for each individual.

- Misspelled names: The names should match Social Security cards.

- Math errors: Whether you are doing your return by hand (I highly discourage it!) or electronically, make sure you add, subtract, multiple, and divide correctly.

You can see the complete list of tax filing mistakes the IRS mentions to avoid.

Final Thoughts – My Question for You

Many people don’t review their tax returns.

Whether you personally prepare it using software or rely on a CPA, spend 15 to 30 minutes reviewing your tax return and understanding how the numbers flow through your tax return.

Use this article as a guide to understand how your income, tax planning strategies, and investments affect your taxes.

I’ll leave you with one question to act on.

When will you review your tax return?