Last Updated on May 4, 2026

The Medicare IRMAA brackets are important to know to avoid surcharges, which is an additional fee many people discover as an unpleasant surprise.

They think they will pay a certain amount for Medicare, but because of a higher income, they may be in a higher Medicare IRMAA bracket.

The good news is that the IRMAA Medicare surcharge resets each year, so if you take the time to learn about it and strategies to reduce or avoid it, you may be able to pay less for your Medicare.

Let’s discuss what IRMAA is, the different 2026 brackets, how to pay the IRMAA surcharge, strategies to reduce the surcharge, how to appeal IRMAA, and future tax planning.

What is IRMAA?

IRMAA stands for Income-Related Monthly Adjusted Amount. It’s an additional amount, or surcharge, you pay for Medicare Part B and Part D when your income meets certain thresholds.

Unfortunately, you don’t get better Medicare coverage or anything additional. It’s simply an additional amount you pay for the same coverage if you have higher levels of income, which is why it can catch people off guard.

Income Definition of IRMAA

There are many different definitions of income for different governmental programs. IRMAA is determined based on your Modified Adjusted Gross Income (MAGI) with certain adjustments.

Unfortunately, MAGI is not a line on your tax return, but we can look at the tax return for the AGI, make a few adjustments, and arrive at the MAGI that will determine your IRMAA bracket.

Look at line 11 of your tax return to find your Adjusted Gross Income (AGI). You can see from the image below what will affect your AGI:

- Wages

- Taxable interest

- Dividends

- IRA distributions

- Pension and annuity income

- Social Security

- Capital gains

- Schedule 1 income (examples: alimony, rental real estate, gambling winnings)

From there, you can make the following adjustments by adding back the following:

- Tax-exempt interest (example: municipal bonds) – Line 2a

- Interest from U.S. savings bonds used to pay higher education tuition and fees

- Earned income of U.S. citizens living abroad that was excluded from gross income

- Income from sources within Guam, American Samoa, the Northern Mariana Islands, or Puerto Rico

How to Calculate your MAGI: For many people to calculate their MAGI for IRMAA, they will locate Line 11 (AGI) and add tax-exempt interest (Line 2a).

IRMAA Delay – 2 Years Later

The reason IRMAA can surprise people is that your IRMAA Medicare premium is based on your MAGI from two years ago.

For example, your 2026 Medicare Part B and Part D premium amount is based on your MAGI in 2024.

Your 2027 Medicare Part B and Part D premium will be based on your MAGI in 2025.

In other words, tax planning (or lack of) you do today may influence the amount you pay for Medicare two years from now.

Medicare Advantage vs. Medicare Supplement

As you plan for which IRMAA bracket you may fall into, pay attention to the type of Medicare plan you choose. There are huge differences between Medicare Advantage and a Medicare Supplement. Watch the video below to learn more.

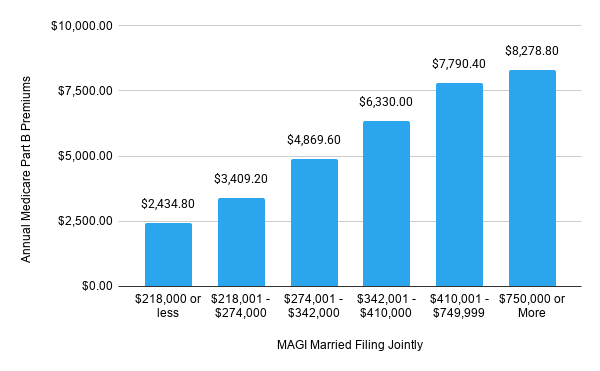

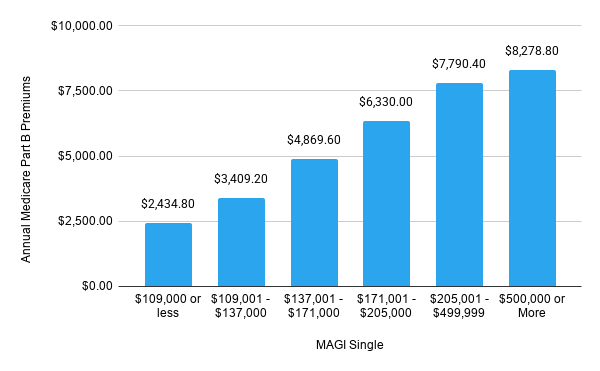

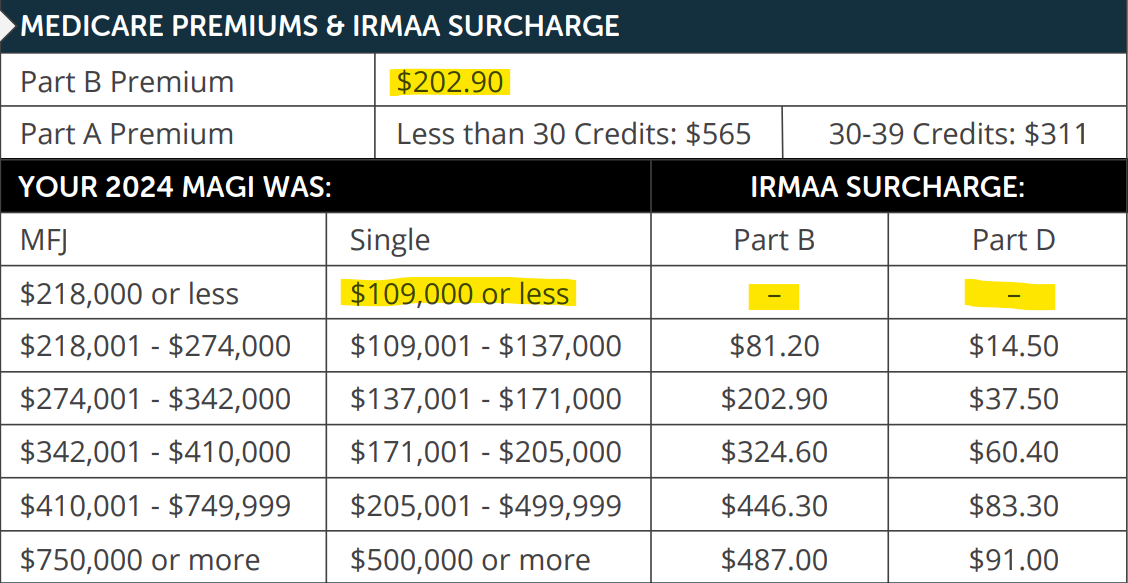

IRMAA Medicare Brackets

There are five IRMAA Medicare tax brackets. If you are curious what past IRMAA brackets looked like, you can find them on the ssa.gov website.

The 2026 IRMAA Medicare Tax Brackets are below. Note that they are based on 2024 MAGI.

2026 Part B Medicare IRMAA Bracket

| 2024 MAGI Single | 2024 MAGI Married Filing Jointly | Part B Premium (Monthly) | Additional Increase from Prior Bracket (Monthly) |

| $109,000 or less | $218,000 or less | $202.90 | |

| $109,001 – $137,000 | $218,001 – $274,000 | $284.10 | $81.20 |

| $137,001 – $171,000 | $274,001 – $342,000 | $405.80 | $121.70 |

| $171,001 – $205,000 | $342,001 – $410,000 | $527.50 | $121.70 |

| $205,001 – $499,999 | $410,001 – $749,999 | $649.20 | $121.70 |

| $500,000 or more | $750,000 or more | $689.90 | $40.70 |

2026 Part D Medicare IRMAA Bracket

| 2024 MAGI Single | 2024 MAGI Married Filing Jointly | Part D Premium (Monthly) | Additional Increase from Prior Bracket (Monthly) |

| $109,000 or less | $218,000 or less | $0 | |

| $109,001 – $137,000 | $218,001 – $274,000 | $14.50 | $14.50 |

| $137,001 – $171,000 | $274,001 – $342,000 | $37.50 | $23.00 |

| $171,001 – $205,000 | $342,001 – $410,000 | $60.40 | $22.90 |

| $205,001 – $499,999 | $410,001 – $749,999 | $83.30 | $22.90 |

| $500,000 or more | $750,000 or more | $91.00 | $7.70 |

Each bracket corresponds to how much someone pays or shares in the program costs. For example, below are the brackets and how much of the program costs they cover:

- Standard Amount: 25%

- 1st Bracket: 35%

- 2nd Bracket: 50%

- 3rd Bracket: 65%

- 4th Bracket: 80%

- 5th Bracket: 85%

For people paying the standard amount, they only cover 25% of Medicare costs. Even people earning the highest amount don’t pay their full share of the Medicare costs. The highest they pay is 85%!

IRMAA MAGI Cliff Warning

It’s important to pay attention to your income because these brackets work as a cliff.

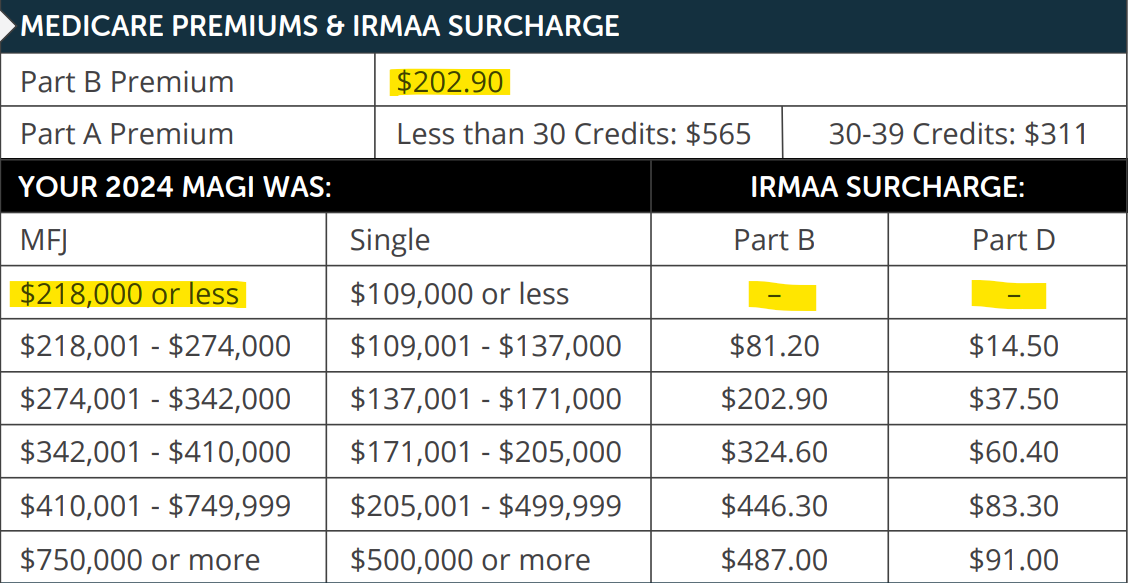

Even if you only go over by $1, you are subject to the next Medicare IRMAA bracket. For example, if you file your tax return as married filing jointly and your MAGI was $218,001 in 2024, your 2026 Medicare Part B premium will be $284.10 and your Medicare Part D premium will be $14.50.

Had you reduced your income by $1 and had a MAGI of $218,000, you would have paid $81.20 less per month for Medicare Part B and $0 per month for Part D.

Over the course of the year, that additional $1 of income caused an additional $974.40 in Part B premiums and $174 in Part D premiums, for a combined total increase of $1,148.40.

Here are two charts you can reference:

Does IRMAA apply to Medicare Advantage Plans?

Some people wonder whether they can switch from Original Medicare to a Medicare Advantage plan to avoid IRMAA.

The answer is no.

IRMAA still applies to Medicare Advantage plans.

You may be able to reduce your cost with a Medicare Advantage plan, but they may come with restrictions, less accessible medical care, and potentially higher costs down the road.

Examples of IRMAA Surcharges

Let’s look at a few examples of IRMAA surcharges to see how they work.

No IRMAA Surcharge

Example 1: Debbie is a widow with a MAGI of $67,000 in 2024. Since she will file as a single individual, the following applies in 2026:

- Medicare Part B Premium: No surcharge, $185.00 per month

- Medicare Part D Premium Surcharge: No surcharge, monthly plan premium only

Example 2: Kate and Mike are married with a MAGI of $190,000 in 2024. Since they will file as married filing jointly, the following applies for 2026:

- Medicare Part B Premium: No surcharge, $185.00 per month per person

- Medicare Part D Premium Surcharge: No surcharge, monthly plan premium only

IRMAA Surcharge – 3rd Medicare IRMAA Bracket

Example 1: Denise is a widow with a MAGI of $145,000 in 2024. Since she will file as a single individual, the following applies for 2025:

- Medicare Part B Premium: $405.80 (normal $202.90 premium + $202.90 IRMAA surcharge)

- Medicare Part D Premium Surcharge: $37.50 (monthly plan premium + $37.50 IRMAA surcharge)

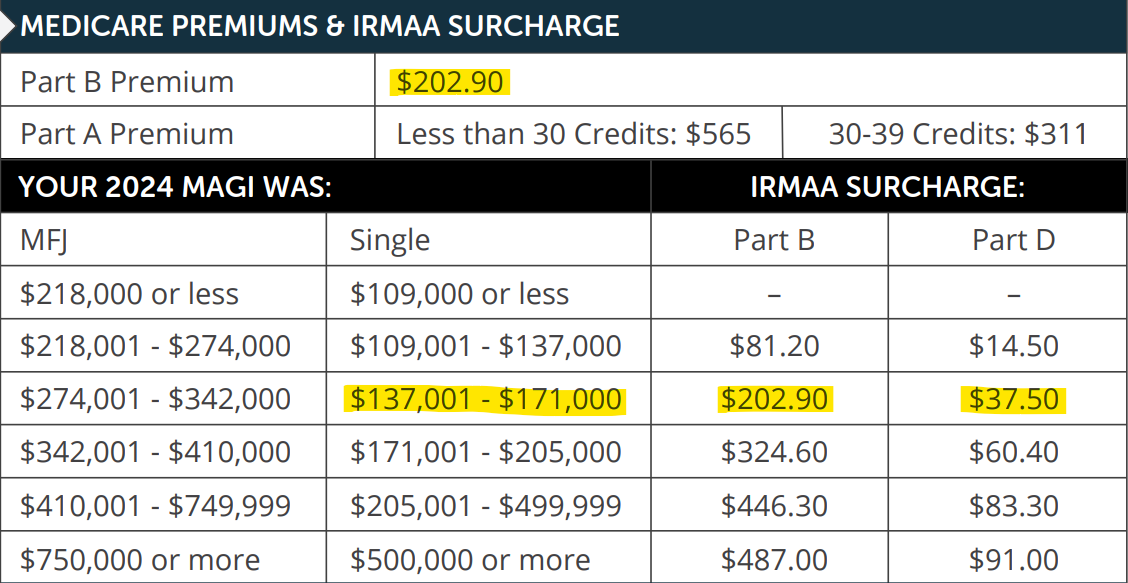

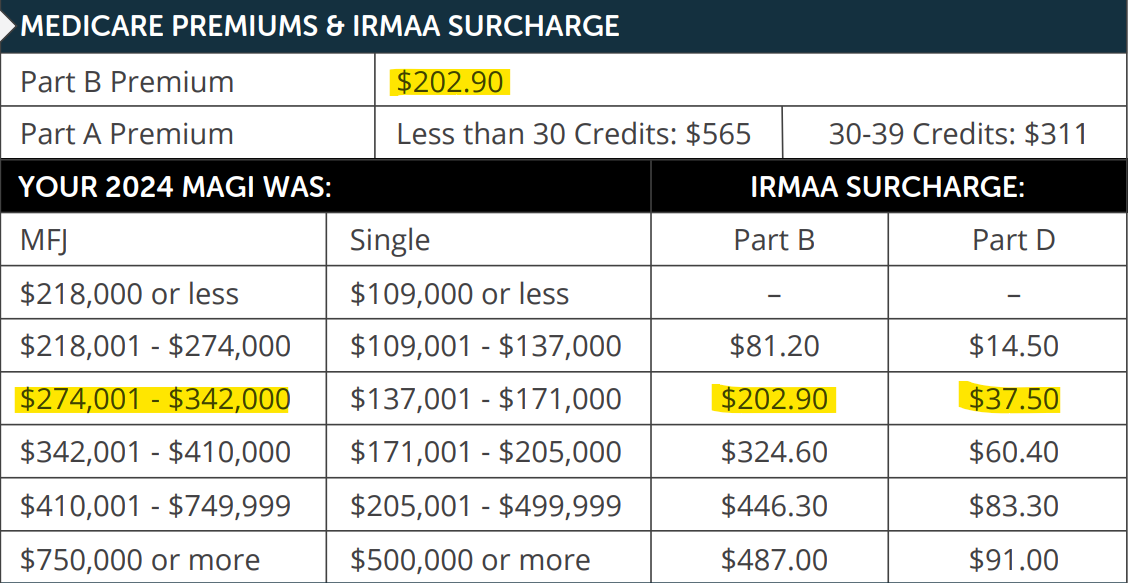

Example 2: Alison and Jeremiah are married with a MAGI of $300,000 in 2024. Since they will file as married filing jointly, the following applies for 2026:

- Medicare Part B Premium: $405.80 per person (normal $202.90 premium + $202.90 IRMAA surcharge)

- Medicare Part D Premium Surcharge: $37.50 per person (monthly plan premium + $37.50 IRMAA surcharge)

How to Pay the Medicare IRMAA Surcharge

If you are already collecting Social Security, paying the Medicare IRMAA surcharge is easy.

It’s automatically deducted from your Social Security!

If you are not collecting Social Security, the government will send you a bill for the amount. The IRMAA surcharge is not paid to your insurance provider. It’s paid to the government and can be seen as an extra tax to help support the Medicare program.

You can pay for the bill 4 ways:

- Pay online through your Medicare account

- Sign up for Medicare Easy Pay

- Use your bank’s online bill payment service

- Mail your payment to Medicare (can pay be check, money order, credit card or debit card – be sure to include your payment coupon)

If you want to understand your bill, Medicare.gov has a great PDF that breaks down understanding your bill.

7 Strategies to Reduce IRMAA Surcharges

Now that you know more about IRMAA, let’s talk about how to reduce or potentially avoid IRMAA surcharges.

Tax Deductible Retirement Contributions

If you are still working and have earned income, you can consider making tax-deductible retirement contributions.

For example, you may be able to make contributions to the following types of accounts:

- Traditional 401(k), 403(b), 457, or deferred compensation plans

- Solo or Individual 401(k)

- SEP or SIMPLE IRA

- Traditional IRA

Since contributions may reduce your taxable wages, they may help reduce your MAGI and subsequent IRMAA bracket two years from now.

Planning Tip: Since the current tax rates are low compared to historical tax rates, pay special attention to whether deferring money at today’s tax rates make sense. Some people may be better off paying the IRMAA surcharge and not deferring at their current tax rate because they may be in a higher tax bracket in the future.

Charitable Giving

Not all forms of charitable giving may help reduce IRMAA surcharges. The method in which you give matters because many charitable donations are below the line deductions – meaning they don’t affect your MAGI!

As you can see above, many charitable contributions, such as cash or appreciated investments will go on line 12 if you itemize. Line 12 is below Line 11, your adjusted gross income, which means the actual donation won’t help your MAGI; however, there are certain methods of charitable giving that can potentially reduce your IRMAA surcharge.

Qualified Charitable Distributions (QCDs): QCDs are donations made directly to charity from your IRA when you are age 70 ½ or older. While distributions from an IRA are normally taxable as ordinary income, QCDs are not taxable.

Since they are not taxable, they don’t show up on line 4b, the taxable amount of IRA distributions.

Since they don’t show up on line 4b as taxable, a QCD may reduce your MAGI and, subsequently, your IRMAA bracket.

Donating Highly Appreciated Assets Held More Than A Year: Donating highly appreciated assets also won’t help lower your MAGI directly because the donation falls on Line 12, which is below the AGI line. But, if you were considering selling an investment and donating the cash (or donating cash and then selling an investment to replenish for your own spending), donating the investment would reduce the capital gains you may recognize, which could lower your MAGI.

One example of this is the following: you had investments you bought for $10,000 five years ago and it’s worth $20,000 now. You plan to sell it to cash to replenish your bank account because of a charitable donation. If you do this, you would recognize $10,000 in long-term capital gains, which would increase your MAGI. This could bump you into a higher IRMAA bracket.

Instead of selling the investment, you could donate it directly to charity, take a $20,000 charitable deduction, and avoid the $10,000 long-term capital gain. While the $20,000 charitable deduction is not reducing your MAGI, avoiding the $10,000 long-term capital gain does.

Capital gains show up on Line 7 of the tax return, which affects your MAGI

Donor-Advised Funds (DAFs): Donor-Advised Funds won’t help lower your MAGI directly for the same reason donating highly appreciated assets held more than a year won’t, but if you donate highly appreciated investments to a donor-advised fund, you may avoid the capital gains on the donated investment, which would avoid capital gains that may raise your MAGI.

The benefit of a DAF is that you can make a donation today, receive a charitable deduction, and give grants from the DAF over time. It’s a way to still have limited control over the money.

Tax-Efficient Investments in Brokerage Accounts

If your investments are tax-inefficient, they may create unnecessary, additional taxes for you.

For example, I’ve seen people use high turnover funds that create large capital gain distributions in December. Those capital gain distributions can increase your MAGI and cause higher Medicare premiums. By using ETFs or mutual funds with low turnover, you may be able to reduce or eliminate capital gain distributions.

Another example of a tax-inefficient strategy is not using asset location. Asset location is a strategy where you put investments in their most tax efficient accounts. For example, instead of putting funds with high income, such as bonds and REITs, inside a brokerage account, you may want to put them in a tax advantaged account, such as an IRA. The income those investments produce could increase your MAGI in the brokerage account, where as in the IRA, they may be sheltered.

Lastly, I know many people like to focus on dividend investing, but there are many problems with dividend investing. One problem with dividend investing inside of a brokerage account is that the higher dividends can cause a higher MAGI, which can cause higher Medicare premiums.

The types of investments you use and which accounts you put the investments into can affect your IRMAA bracket. Pay close attention that your investments are not increasing your IRMAA bracket.

Create a Tax-Efficient Withdrawal Strategy

One of the common issues I see in retirement is not paying attention to the amount of lifetime taxes someone will pay. They simply focus on the current year and try to reduce taxes as much as possible.

The problem with this approach is that it can lead to higher taxes later, potentially pushing people into higher Medicare IRMAA brackets for life.

For example, someone may try to reduce their income for a few years, but in doing so, cause decades of higher taxes.

I see this happen when people retire early, but fail to take advantage of a 0% long-term capital gains bracket or plan for large withdrawals.

There are those who want to move or build a house in a couple of years, and instead of spreading out income over multiple years to stay below higher IRMAA brackets, they recognize the income in one year, which pushes them into a much higher IRMAA bracket.

I’ve also seen people fail to take advantage of a 0% long-term capital gains bracket. Instead of proactively recognizing income and paying zero in federal taxes on it, they let the opportunity slip by. By recognizing the gains, they can raise their cost basis so when they sell in the future, less of it will be taxable. When less of it is taxable, they reduce their MAGI and possibly IRMAA bracket.

Other strategies could include taking money from a Roth IRA, reverse mortgage, or cash value life insurance.

If you are going to go into the next Medicare IRMAA bracket by a few dollars, you may consider taking money out of a Roth IRA or a cash value life insurance if you can do it in a tax-free way.

While reverse mortgages can be expensive and should not be obtained for tax reasons, if you have one, you could use it to help smooth out your income.

The key with any withdrawal strategy is to know how each account is taxed (ordinary income, tax-free, or capital gains) and proactively plan for larger withdrawals to smooth income out over time.

Roth Conversions

Another common strategy to reduce or avoid higher IRMAA brackets is to do Roth conversions, particularly early in retirement.

Some people are focused on deferring taxes as long as possible, but the issue is that future Required Minimum Distributions (RMDs) can be much higher, causing your MAGI to be higher for the rest of your life. RMDs start at either age 73 or 75, depending on your birth year. The IRS forces money out of your IRA, 401(k), 403(b) and other tax-deferred accounts through RMDs, and they are taxed as ordinary income at that time.

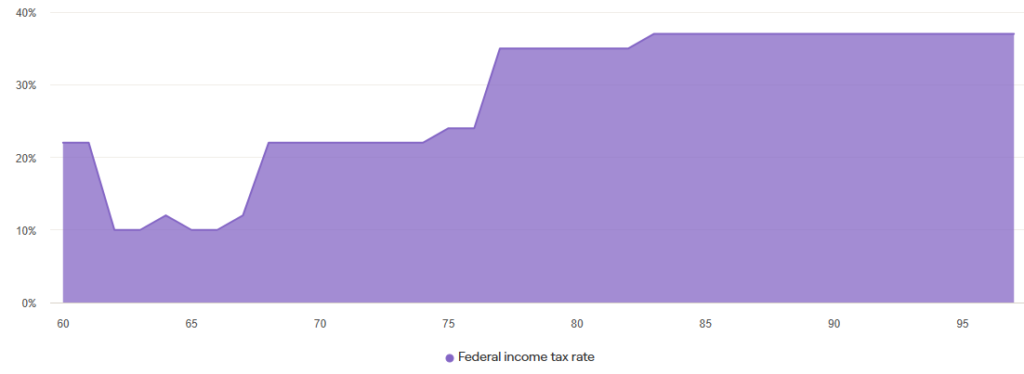

One strategy is to do a few years of larger Roth conversions, potentially pay a higher amount for Medicare for a short period of time, but then reduce the income you must take later for a longer period of time.

For example, in the chart below, you can see this person may be in the 35% or 37% tax bracket later. Instead of waiting for those years to occur, they may want to do a Roth conversion and fill up the 12%, 22%, and 24% tax bracket the next few years to smooth out their taxes and pay less later at a higher rate.

Roth conversions are a particularly important tax strategy because tax rates are historically low. Plus, if you can reduce your future RMDs, you may be able to lower your MAGI and subsequently, your Medicare IRMAA bracket later in life.

Additionally, after the death of a spouse, your income is often a similar amount, but tax brackets and Medicare IRMAA brackets are often compressed for surviving spouses. Surviving spouses could find themselves in a higher Medicare IRMAA bracket for life with RMDs, Social Security, and other income.

As you can see in the chart below, by doing Roth conversions today, you may be able to reduce the amount you pay in taxes over your lifetime and reduce your MAGI.

Planning Tip: Many people see the Medicare IRMAA bracket as a significant reduction in cash flow because it often is deducted from Social Security. It can come as a surprise when you get a few hundred dollars less per month. When it comes to Roth conversions, try to see the higher Medicare premium as an additional, temporary tax.

For example, if your increase in federal taxes was $36,004 from a $200,000 Roth conversion and your Medicare Part B premiums went up by $162.40 ($81.20 times two people) and your Part D Premiums went up by $29.00 ($14.50 times two people), that is $1,948.80 more in Part B Premiums and $348 more in part D Premiums. Combined, that is $2,296.80.

If you add $2,296.80 to the original tax amount of $36,004, that is $38,300.80 more in taxes.

If you divide the original tax of $36,004 by the $200,000 of increase in the Roth conversion amount, that is an effective tax rate of approximately 18%.

If you divide the new tax of $38,300.80 by the $200,000 of increase in the Roth conversion amount, that is an effective tax rate of approximately 19.2%.

As you can see, the Roth conversion is still worthwhile because the effective tax rate hasn’t changed much (19.2% vs. 18%) even though on a monthly cash flow basis, the increase in Medicare premium (or drop in Social Security benefits as you may see), feels significant.

Delay Social Security

Another strategy to reduce the IRMAA surcharge is to delay Social Security.

Ultimately, how you decide to claim Social Security benefits should be decided based on how you can optimize benefits over two lives if married, or one life if single or widowed; however, a benefit of delaying Social Security is that you can do more tax planning.

If you claim Social Security early, it will fill up whatever tax bracket you are in and potentially provide fewer opportunities for Roth conversions or the 0% capital gains bracket to help manage or spread out your income over time.

People who delay Social Security can decide when and how much income to recognize whereas those that claim early have a set level of income due to Social Security that they can’t adjust.

For example, if a married couple claims Social Security early and it is $50,000 per year, that is $50,000 that fills up a tax bracket instead of a Roth conversion or recognizing capital gains for withdrawal purposes.

People who claim early may have fewer opportunities for tax planning and managing their income, which may mean higher RMDs or more capital gains later, potentially leading them into a higher IRMAA bracket.

Experience a Life-Changing Event and Appeal

The last strategy to reduce the IRMAA surcharge is to have a life-changing event and successfully appeal the higher Medicare surcharge.

Major life events include:

- Married

- Divorce/Annulment

- Death of your spouse

- Work stoppage

- Work reduction

- Loss of income-producing property

- Loss of pension income

- Employer settlement payment

For most people, divorce, death of a spouse, or work reduction or stoppage could impact their Medicare premium.

For example, if you were working one year and then decide to retire and have lower income, you may be able to appeal the IRMAA surcharge because it was a life-changing event that affected your income.

A common question that comes up is “Does selling a home with a large capital gain qualify as a life-changing event?”

Selling a house with no other major life events referenced above likely does not qualify as a life-changing event. If you sell a home with a large capital gain that causes an IRMAA surcharge, you should be prepared for a higher Medicare premium in two years.

How to Appeal an IRMAA Surcharge

You can appeal an IRMAA surcharge by completing and submitting Form SSA-44.

Another method is to call 800-772-1213 and schedule an interview with your local Social Security office. Depending on your situation, how complicated it is, and how much time you have, going in person may be easier.

If you submit Form SSA-44, you’ll need to attach evidence of the life-changing event and potentially show original documents or certified copies.

It’s important to only choose one life-changing event on the list. If you experienced more than one, you’ll want to call your local Social Security office.

Also, if you think Social Security used outdated or incorrect information, you can also appeal. This may be an issue if you file an amended tax return.

To file an appeal, you must follow the instructions closely:

- File an appeal within 60 days of receipt of an IRMAA determination notice

- Typically, they assume you received the notice 5 days after the date on the notice unless you can show you did not receive it within the 5-day period.

- If you file an appeal outside that timeframe, you must have “good cause.”

“Good cause” is fairly broad and could include scenarios like the following:

- Moving and not receiving the letter

- Seeking evidence to support the claim, but did not finish before the time period expire

- Death or serious illness in the immediate family

- Did not understand the requirement or not able to timely file due to physical, mental, educational, or linguistic limitation

If you are thinking about appealing an IRMAA surcharge, please remember to gather the evidence quickly, complete the form or go in person, and make sure you check the appropriate boxes.

Future IRMAA Planning

Although it’s impossible to know exactly what the 2027 IRMAA brackets will be now, we can estimate them.

IRMAA brackets are adjusted by inflation each year, (except the top bracket, which won’t increase until 2028) which means they can go up or down. In 2026, both the IRMAA brackets and Medicare Part B and Part D premiums increased.

To estimate future IRMAA brackets, you can do the following:

- Estimate the average CPI-U from 9/2025 – 8/2026 (we only have 4 of those figures as of this writing, so I assumed there is no inflation the rest of the year. One of those figures is missing because the government didn’t release a CPI number during the October 2025 shutdown.)

- Subtract 249.28 from step 1

- 249.28 is the average CPI-U from 9/2017 – 8/2018

- Divide the step 2 figure by 249.28

- Increase the 2019 IRMAA brackets by the step 3 figure percentage (except for the last top bracket — that won’t adjust until 2028)

- Round to the nearest 1,000

2019 Medicare IRMAA Brackets

| 2019 MAGI Single | 2019 MAGI Married Filing Jointly |

| $85,000 or less | $170,000 or less |

| $85,001 – $107,000 | $170,001 – $214,000 |

| $107,001 – $133,500 | $214,001 – $267,000 |

| $133,501 – $160,000 | $267,001 – $320,000 |

| $160,001 – $500,000 | $320,001 – $750,000 |

| Above $500,000 | Above $750,000 |

If inflation is 0%, below is an estimate of the 2027 IRMAA brackets, which will be based on your 2025 MAGI.

2027 Estimated Medicare IRMAA Brackets

| 2025 MAGI Single | 2025 MAGI Married Filing Jointly | Part B Premium (Monthly) |

| $111,000 or less | $222,000 or less | Standard |

| $111,001 – $140,000 | $222,001 – $280,000 | Standard * 1.4 |

| $140,001 – $175,000 | $281,001 – $350,000 | Standard * 2.0 |

| $175,001 – $209,000 | $350,001 – $418,000 | Standard * 2.6 |

| $209,001 – $500,000 | $418,001 – $750,000 | Standard * 3.2 |

| Above $500,000 | Above $750,000 | Standard * 3.4 |

Here is how I got the first tier number:

- Get the average CPI-U from 9/2025, 10/2025 (estimate because no data was released), 11/2025, 12/2025, and 1/2026 and assume the same figure through 8/2026 = 326.13725

- Subtract 249.28 from step 1 = 76.86

- 249.28 is the average CPI-U from 9/2017 – 8/2018

- Divide the step 2 figure by 249.28 = 30.83%

- Increase the 2019 IRMAA brackets by the step 3 amount = $111,207

- Except for the last top bracket – that won’t adjust until 2028 (based on 2026 MAGI) and will be based on CPI-U from 9/2025 – 8/2026

- Round to the nearest 1,000 = $111,000

- Double for married filing jointly = $222,000

The Part B Premium calculation for anybody outside of the first bracket is to take the standard Part B monthly premium and multiply it by the corresponding number.

For example, if the standard Part B Premium in 2027 is $205.00 (a random number I chose), the second tier would be $287.00 ($205 x 1.4).

If you want to be more conservative in your estimates and skip this math, you could simply use the current IRMAA brackets instead of an estimated one.

Final Thoughts – My Question for You

IRMAA can catch people off guard.

Paying more for Medicare Part B and Part D without receiving any additional benefits can frustrate people.

For people who are aware of the IRMAA surcharge, they can proactively do tax projections and tax planning to potentially reduce or avoid it.

It’s important to pay special attention to your income each year because even $1 in additional income can put you into another IRMAA bracket in two years.

I’ll leave you with one question to act on.

What proactive tax planning will you do to plan for IRMAA?