Last Updated on February 14, 2025

It’s that time of year where you should start to receive your Medicare “Plan Annual Notice of Changes” (ANOC). It usually arrives sometime in September and lists changes in your coverage and costs of your current Medicare plan.

It’s very important to review!

A drug that was covered under the formulary in the prior year may not be covered in the upcoming year. Your providers may not be in network anymore. Your premium, co-pays, deductibles, or co-insurance may have increased.

Like reviewing other types of insurance, not reviewing your Medicare coverage could turn into a very expensive mistake.

Let’s go through in detail why it’s important to review your Medicare plan each year.

Important Dates

First, let’s go through the important dates. You don’t want to miss any of the deadlines.

September and October – Review

September and October are good times to start reviewing your existing plan and new plans. Medicare.gov has a website where you can find health and drug plans. It’s simple to create an account where you can input the doctors you prefer, as well as your prescription drugs.

From there, you can see the yearly premium cost, health deductible, drug deductible, and the maximum out of pocket cost.

October 15 – Open Enrollment Begins

On October 15, you can enroll in a new plan that takes effect on January 1 of the next year. This is the one time of year where anyone can change their coverage without needing to qualify for a Special Enrollment Period.

December 7 – Open Enrollment Ends

Open Enrollment typically ends on December 7. If you want to make changes to your Medicare plan after December 7, you normally need to qualify for a Special Enrollment Period.

January 1 – Coverage Begins

The coverage you selected, whether it is your existing plan or a new plan, normally begins on January 1. This means the new costs, benefits, and coverage start.

January 1 – March 31 – Changes to Medicare Advantage Plan

If you have a Medicare Advantage Plan, you can switch between January 1 and March 31 to another Medicare Advantage Plan or to Original Medicare.

It’s another opportunity to decide your coverage, but you can only switch plans once during this period.

Your Medicare Plan Can Change What it Covers

It’s estimated that 57% of Medicare beneficiaries do not review or compare their coverage options annually, according to the Kaiser Family Foundation.

The problem with this is that your Medicare plan can change what it covers. Below is a list of things that may change:

- Benefits

- Costs (Premium, Deductibles, Copays, Coinsurance)

- Network of Healthcare Providers

- Prescription Drug Coverage and Costs

Benefits

Your Medicare plan may change the benefits and coverage they offer. Medicare Advantage and Supplemental plans are not required to offer the same benefits, which means something that may have been covered last year may not be covered in the upcoming year.

You should review exactly what coverage is available in the upcoming year and decide if that fits within what you wanted. It’s possible another plan offers better coverage for your situation.

For more on the differences between Medicare Advantage and a Medicare Supplemental Plan, watch the video below.

Costs (Premium, Deductibles, Copays, Coinsurance)

Although certain plans may have a $0 deductible, that may not be the best plan for you. It’s important to look at deductibles, copays, and coinsurance to get a feel for how much you may be paying when you visit a physician, have a procedure done, or see another medical provider.

Also, don’t forget to review your maximum out of pocket costs.

Network of Healthcare Providers

There is no guarantee that your Medicare plan will include the same physicians, hospitals, or pharmacies as the prior year.

If you have specific physicians, healthcare clinics, or pharmacies you like, you should make sure that your Medicare plan will cover them.

Prescription Drug Coverage and Costs

Prescription drug coverage is one of the most important elements to review in your Plan Annual Notice of Changes. This is the one that often catches people by surprise.

Each plan has a formulary, which lists prescription drugs that are covered under your plan.

A drug that was on the formulary last year may not be on the formulary this year. They could also move a drug from tier 1 to tier 2, 3, or 4, which may require higher copayments. Given the high cost of many prescription drugs, this could mean paying thousands of dollars or more per year.

You’ll want to put your prescription drugs into Medicare’s plan finder to get an estimate of what you may pay for your drugs; however, prices can change between when you sign up and pay for your prescription under the plan.

Even if you sign up for a plan thinking you will pay one price, “your plan may raise the copayment or coinsurance you pay for a particular drug when the manufacturer raises their price, or when a plan starts to offer a generic form of a drug, but you keep taking the brand name drug.”

New Plans Can Become Available

Another reason to compare your Medicare plan to other plans is that new plans can become available in your area.

It’s estimated that 3,959 plans were available nationwide in 2024, which was 39 fewer plans than 2023. The average Medicare beneficiary had access to 43 Medicare Advantage plans in 2024.

If plans are continually changing and more are becoming available, there is a chance a different plan may be better for you.

Imagine for a second that you had access to 43 Medicare Advantage plans and each one changed their coverage, costs, network of healthcare providers, and prescription drug coverage. If you don’t review the plans each year, you may miss out on opportunities to save money. By not taking 30 minutes to review your coverage, you could end up costing yourself thousands of dollars.

For most people, a quick check is worth potentially saving thousands of dollars.

Is it for you?

Your Health Needs May Change

Another reason to review your Medicare plan is that your health needs may change.

Perhaps last year you were healthy and this year you were diagnosed with an illness that requires expensive, special medication or vice versa.

For some people, an inexpensive plan with a high drug deductible and high maximum out of pocket cost may be okay if they are healthy and rarely use medical services.

For other people, a plan with an expensive monthly premium, low drug deductible, and lower maximum out of pocket cost may end up costing them less over the course of a year.

Someone may not think they need good prescription drug coverage, but if they are diagnosed with cancer and need a chemotherapy drug that costs thousands of dollars each round, their perspective may change.

It’s important to weigh your financial resources against potential out of pocket costs if your health needs change. For example, you may be healthy at the beginning of the year, but as soon as you are out of open enrollment, you could be diagnosed with a serious health issue that requires access to many specialists.

As one gets older, they often require more regular access to healthcare services, which is why it’s important to review Medicare plans annually to make sure they serve you well.

How to Review Your Plan

The do-it-yourself approach to reviewing your plan is using https://www.medicare.gov/plan-compare/ to enter your information.

There are other options if you need more help.

Use a Health Insurance Broker

One option is to use a health insurance brokerage to search for a plan that may be best for you.

There are two brokers I’ve connected with in the past who I found to be knowledgeable and who create great educational and free content:

They both have informational resources and videos online to help explain Medicare and varying support services if you enroll in Medicare through them.

Boomer Benefits even has a question and answer Facebook group to help with your questions.

Health insurance brokers are paid by health insurance companies and typically receive a commission in the first year they enroll someone, as well as a lesser amount in future years.

The maximum commission is set by the Centers for Medicare and Medicaid Services (CMS) for Medicare Advantage Plans. For example, in 2025, the maximum commission is $626 in most states. California is an exception at $780. For Part D plans, the maximum commission is $109 in 2025.

If you renew your plan, the health insurance broker may receive 50% of the first year commission.

For Medigap plans, the agent’s commission is typically a percentage of the annual premium. The average commission might be 20% of the first year annual premium and 10% in renewal years, which means if the average premium in 2025 for Medigap was $1,660, an agent might make $322 the first year and $166 upon renewal.

Generally, a health insurer broker is paid more for Medicare Advantage plans, and while sometimes these plans can make more sense for people, the health insurance brokers I’ve talked with often recommend Medigap plans. What I’ve been told is they often have better coverage than Medicare Advantage plans, but better coverage does often come with a higher price.

Contact a State Health Insurance Assistance Program (SHIP)

Another option is to contact your State Health Insurance Assistance Program (SHIP). Each state is different, but these organizations usually have volunteers to help you navigate the Medicare choices.

For example, in Washington state, there are 250 volunteers across the state with local non-profits who can help assess Medicare coverage needs, provide Medicare enrollment help, and make referrals to other programs.

In Wisconsin, a SHIP counselor is available on the Medigap Helpline and other phone resources, as well as locally at aging units and aging and disability resource centers in every county.

It’s wonderful these resources are available, but one potential downside is that you are working with volunteers, which means the knowledge and helpfulness may depend on the volunteer, their training and experience.

Finding Lower Prescription Drug Prices

Given the high cost of prescription drugs, I wanted to provide a few resources to potentially find lower cost prescription drugs.

CostPlus Drug Company

CostPlus Drug Company is Mark Cuban’s startup to disrupt the drug industry and take on the high cost of prescription drugs. The premise is that they will charge their cost plus a 15% mark up, pharmacy fee, and shipping fee.

While I don’t have enough expertise to say whether the study is accurate, one study estimated that Medicare could have saved up to $3.6 billion in 2020 if they bought 77 generic drugs through CostPlus Drug company.

Here is a screenshot of the website of one drug, amlodipine, as an example:

You can see the manufacturing cost, 15% markup, pharmacy labor, and shipping costs. You can also compare it to a typical pharmacy cost.

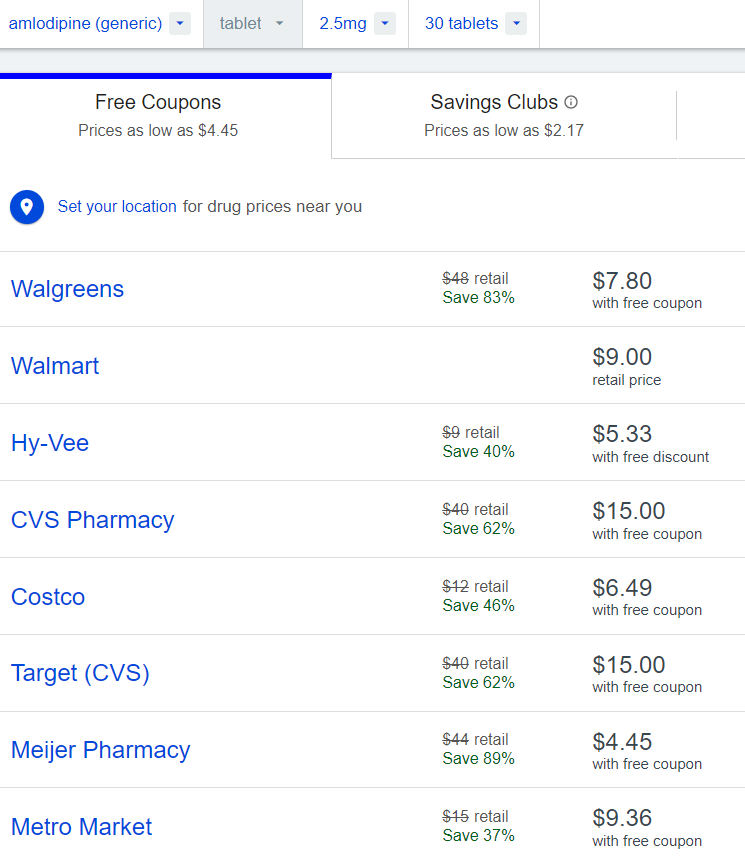

GoodRx

GoodRx is a publicly traded company that offers “coupons” that lower the cost of prescription drugs. You can input your prescription drug, zip code, and then see free coupons, savings clubs, and mail order prices.

Prices vary considerably between pharmacies.

Comparing amlodipine on GoodRx, here is a screenshot below:

As you can see, some prices are higher than CostPlus Drug Company while others are lower when shipping is considered.

It’s worth shopping around to see if a prescription drug is cheaper out of pocket instead of running it through insurance.

Final Thoughts – My Question for You

Although certain Medicare plans are standardized, Medicare Advantage Plans may change each year.

Even if nothing has changed in your life, you should review your Medicare plan to see if it’s coverage, healthcare providers, costs, or prescription drug coverage has changed. Prescription drugs can be moved to a more expensive tier on the formulary or dropped altogether. Coverage can change. Healthcare providers may no longer be in network.

Then, there is the possibility your health has changed or a new plan is a better fit.

Every fall, don’t forget to review your Medicare Plan and compare it to other plans to see which may be a good fit for you. If you need help reviewing it, there are health insurance brokers or free, local volunteer resources in each state.

I’ll leave you with one question to act on.

When will you review your Medicare plan?